Most investors have completely written off this company, but this klarna stock analysis shows why they might be wrong. It went public last September at $40 a share, spiked to $57.20 on day one, and then proceeded to collapse. The stock bottomed out at $12.18. That is a 79% decline.

But while the rest of the market has been in freefall over the last 45 days, this stock stopped dropping.

Klarna, ticker K, is quietly building a base. The fundamentals are screaming buy, and the technical setup points to a massive turnaround opportunity. We are looking at a potential 200% to 300% upside. Here is exactly what the data says.

Why Did Klarna Stock Crash 79% After Its IPO?

The crash came from a combination of post-IPO selling pressure, the Iran war breaking out in late February, and a severe pullback across the broader tech and fintech sectors. The stock fell from its all-time high of $57.20 down to a low of $12.18.

The company executed its IPO last September at $40 per share. The market was initially thrilled. The first-day pop pushed the price to $57.20. That day-one peak was, and still is, the all-time high.

Then the selling started. The macro environment shifted aggressively. The Iran war broke out in late February. Markets went risk-off immediately, and fintech got hit especially hard. In the six months since going public, this stock has been absolutely crushed.

You also have to factor in the standard post-IPO mechanics. The lockup period for insider selling typically expires 180 days after an IPO. Six months in, all those insiders, venture capitalists, and early investors can finally dump their shares and cash out. For Klarna, that lockup expiration hit in March.

The insiders who wanted to sell have already sold. That massive supply overhang is mostly cleared out. What is left is a stock sitting around $13, 67% below its IPO price.

More Than Buy Now Pay Later

Most people know Klarna from the checkout screen. You are shopping on Amazon or Target, and you see the option to split your purchase into four interest-free payments. That is the core buy now pay later model. But calling Klarna just a BNPL stock is like saying Amazon is just a bookstore.

The business is actively transforming into a full-service digital bank, expanding into savings accounts, checking accounts, and AI-powered personal finance tools.

Klarna also learned a hard lesson about artificial intelligence recently. They fired their AI customer service system after finding out human agents did the job better. But they did not abandon the technology. They doubled down on AI for the backend, non-customer-facing operations. And it worked.

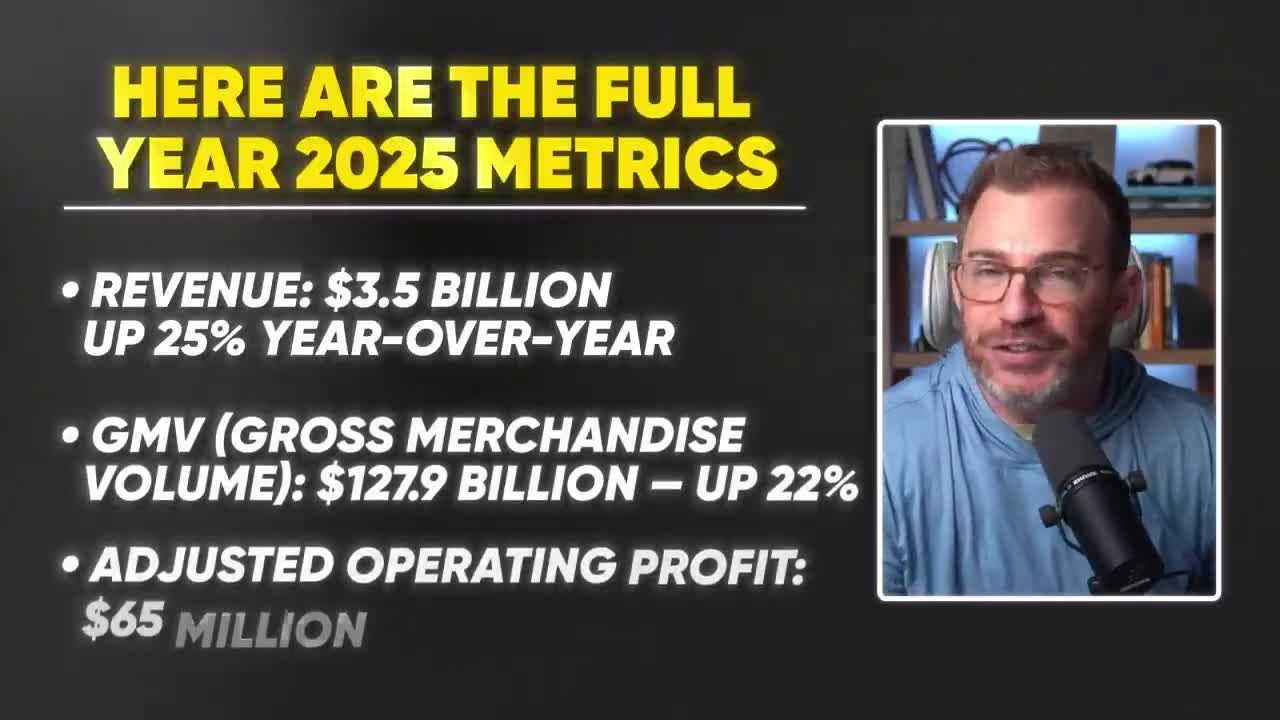

Full Year 2025 Financials

For a company trading at a $5 billion market cap, these metrics are impressive. The data tells a story of a company scaling rapidly despite its depressed share price.

- Revenue: $3.5 billion (up 25% year-over-year)

- Gross Merchandise Volume: $127 billion (up 22% year-over-year)

- Adjusted Operating Profit: $65 million

The most recent quarter is even better. Revenue hit $1.08 billion. Their first-ever billion-dollar quarter. That translates to 38% year-over-year growth. They also beat guidance on both revenue and GMV.

You might look at the GAAP accounting and notice the company is still losing money. Earnings per share were negative $0.79 for the full year 2025. But you have to look under the hood. These losses were largely tied to the IPO itself.

When a company goes public, they face massive one-time cash payments: legal fees, banker fees, compliance buildout, settlement of pre-IPO employee equity. All of these expenses run through cash flow from operations and investing. Klarna also executed a large lease restructure to cut down on office space. They burned significant cash upfront to save money over the long term.

The actual business is generating real cash. The reported losses are mostly accounting items like amortization from acquisitions and stock-based compensation. It is not cash going out the door.

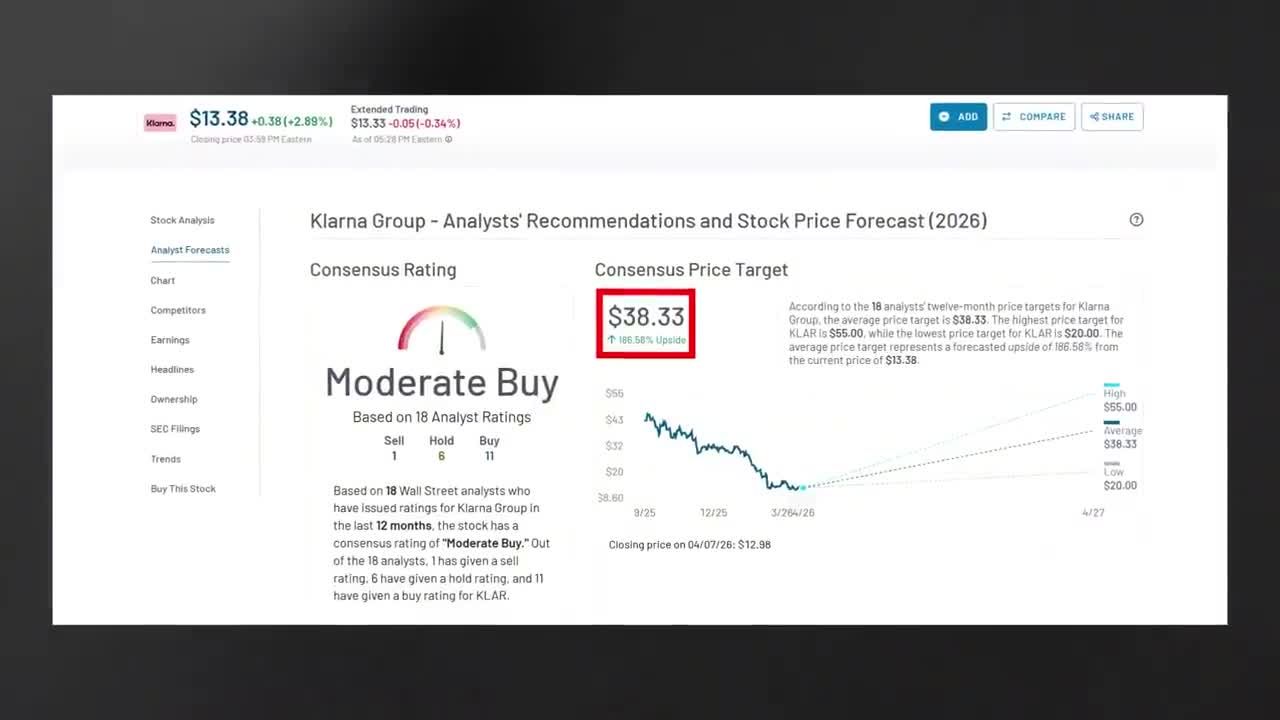

What Are Wall Street Analysts Saying About Klarna Stock?

Wall Street knows the accounting losses are not the full story. The consensus 12-month price target from analysts is $38 to $39 per share.

And this industry has plenty of room to support that kind of valuation. The US buy now pay later market was worth $107 billion in 2025. By 2031, projections show it hitting $258 billion. That is a 2.4x expansion in just six years.

Even more interesting is the physical retail space. In-store BNPL usage is growing at a 19% annual rate. That is actually faster than it is growing online. This physical retail expansion is exactly why their next major partnership matters so much.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWhat Is Klarna's Walmart Partnership and Why Does It Matter?

Last year, Klarna formalized a partnership with Walmart's One Pay, giving them access to Walmart's 240 million weekly customers. The Klarna CEO called it a "game-changer."

Walmart had previously partnered with Affirm. They switched to Klarna, and as of 2026, the deal is fully exclusive. The largest retail audience in the world is now being pushed directly to Klarna's service.

Even with the Walmart deal, competition is fierce. Affirm, Afterpay, PayPal, and the emerging Apple Pay integration are all in the mix. The buy now pay later space has become commoditized. Every checkout has four or five different payment options. Merchants have pricing power, and consumer loyalty is pretty much non-existent.

But Klarna does not need to win the pure BNPL game. I do not think they are even trying to. They are using buy now pay later as a customer acquisition channel, then taking those customers to build banking relationships.

The Real Competitive Moat

Think about traditional banking. A traditional bank spends $300 to $400 to acquire a single customer. That is their cost per acquisition. Klarna acquires a customer every time someone uses their pay-in-four option at checkout.

Once they have that customer, they have incredibly valuable data. The customer is already engaged with their spending. Klarna knows their purchase history. They know their creditworthiness in real time. That is an extraordinarily valuable data set.

The real threat is not Affirm or PayPal. The only real threat is Apple. Apple Pay is integrating both Klarna and Affirm as payment options at checkout, which means Apple once again controls the distribution layer. If Apple decides to build their own BNPL product at scale, that is a risk.

But they are not going to. Apple already tried this with Apple Pay Later. It let users split purchases up to $1,000 into four payments over six weeks. They shut it down in 2024. It was not worth the headache, so they are partnering with Klarna instead.

The Technical Setup

Klarna IPO'd at $40 in September 2025. First-day pop ran to $57.20. That is the all-time high. Then it fell hard. The Iran war broke out in late February. Markets went risk-off and fintech got hit especially bad.

But look at what has happened since then. The stock has been grinding along, holding in that $12 to $14 range. Six weeks of tight consolidation while the NASDAQ has continued selling off.

That is relative strength. The sellers have run out of steam. The people who panic sold at 20 and 15 and 12 are gone. The lockup expiration cleared the insider overhang. What remains is a stock at $13, 67% below the IPO price, with a business growing 38% per quarter and analyst price targets of $39.

Does Klarna Survive? A Klarna Stock Analysis

That is the real question. And I believe they do.

The company has $1.3 billion in cash on the balance sheet. Revenue is $3.5 billion annually and growing. They are profitable on an adjusted operating basis. They have 93 million active customers. This is not a startup burning cash with no revenue. This is not a speculative story. This is a mature, scaled financial services company with a real business.

The risk of bankruptcy or going-concern failure is minimal in my view.

The Risks

Yes, of course there are risks.

First, the company is not yet GAAP profitable. Net losses are real, even if operating cash flow is improving. Second is regulatory risk. The Consumer Financial Protection Bureau has been looking at the BNPL space, and new legislation targeting these companies is always a possibility.

A recession would also hurt Klarna. The risk there is not in less sales volume. It is in a rise in customer default rates. When you are lending out $127 billion a year, it stings when people stop paying you back.

There is real risk here. But there is also substantial upside.

The Bottom Line on This Klarna Stock Analysis

What you have to decide is this. One: do I believe this business will continue to operate and grow over the next two to five years? And two: is a 200% to 300% upside worth the default risk?

If the answer to both is yes, it is a buy at this price. If not, you should probably pass.

Klarna went public and the market got scared. The stock collapsed, peak to trough 79%. But the business kept growing. Revenue hit a billion dollars in a single quarter. Analyst consensus says the stock is worth three times what it trades for today. And technically, while everything else is falling, the stock is holding its ground.

A company with $3.5 billion in revenue, 93 million customers, and a Walmart partnership trading at a $5 billion valuation. Do with that what you will.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- Klarna (ticker: K) IPO'd at $40 in September, peaked at $57.20 on day one, then collapsed 79% to a low of $12.18 — but stopped falling while the broader market continued selling off.

- Revenue hit $1 billion in a single quarter, with full-year 2025 revenue at $3.5 billion and 93 million active customers.

- Wall Street analyst consensus pegs the stock at roughly 3x its current trading price, implying 200–300% upside from the $12–$14 range.

- Klarna's current market cap is approximately $5 billion — a steep discount for a company with $3.5B in revenue and a major Walmart distribution partnership.

- The presenter's thesis hinges on a technical base-building pattern: the stock holding ground while peers fall is treated as a bullish divergence signal.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources