The iran war bond market fallout is something almost nobody is prepared for, and the financial system is sitting on a time bomb.

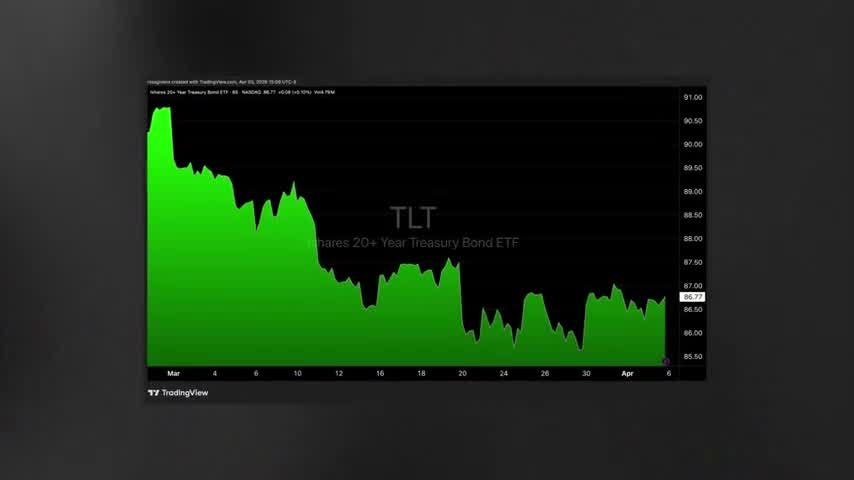

Since the conflict began, the bond market reaction has been severe and immediate. US bond prices have already fallen by around 5%. That might not sound like a massive drop to the average stock trader. In the fixed-income world, that means $1.5 trillion in value has been wiped off the bond market.

You need to understand exactly how this mechanism works to protect your capital and position yourself for the rotation that is already underway.

How Did the Iran War Wipe .5 Trillion From the Bond Market?

Bottom Line: The presenter's core argument is that the Iran war is acting as an accelerant on two slow-burning crises — a fragile Treasury market and sticky inflation — that were already threatening financial stability. The bond market, not stocks, is where the real damage is showing up first, and investors who ignore it are misreading where systemic risk actually sits. The actionable conclusion: rotate away from rate-sensitive assets and toward hard commodities, energy, and infrastructure before the bond panic forces everyone else to do the same.

Bottom Line: The presenter's core argument is that the Iran war is acting as an accelerant on two slow-burning crises — a fragile Treasury market and sticky inflation — that were already threatening financial stability. The bond market, not stocks, is where the real damage is showing up first, and investors who ignore it are misreading where systemic risk actually sits. The actionable conclusion: rotate away from rate-sensitive assets and toward hard commodities, energy, and infrastructure before the bond panic forces everyone else to do the same.

A 5% drop in bond prices translates to $1.5 trillion in value wiped off the bond market. Treasury bonds are at a critical juncture. Further weakness from this war could quickly turn into a bond market panic.

As bond prices fall, bond yields go up. The yield on a 30-year Treasury note is once again attempting to move above 5%. Historically, bonds are boring. Most people don't pay much attention to them. That needs to change right now, because the war in Iran is directly impacting the US Treasury market and could be about to put huge pressure on the financial system.

Bond yields could spike much more than they already have if this continues.

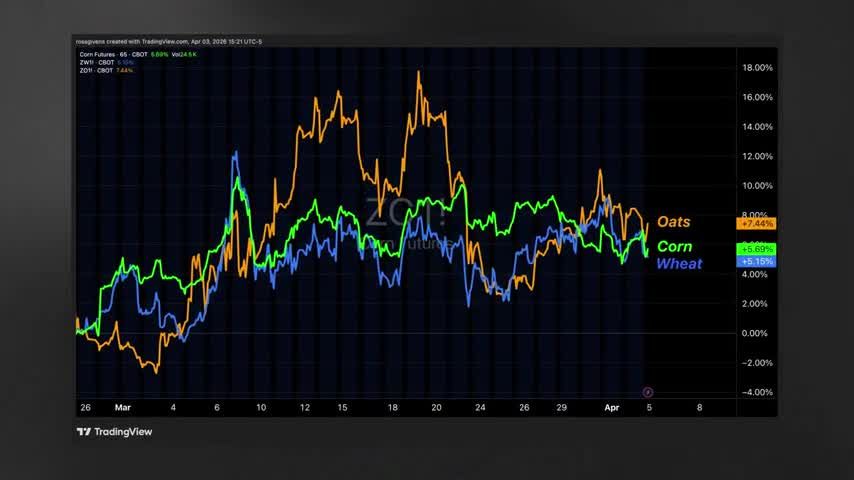

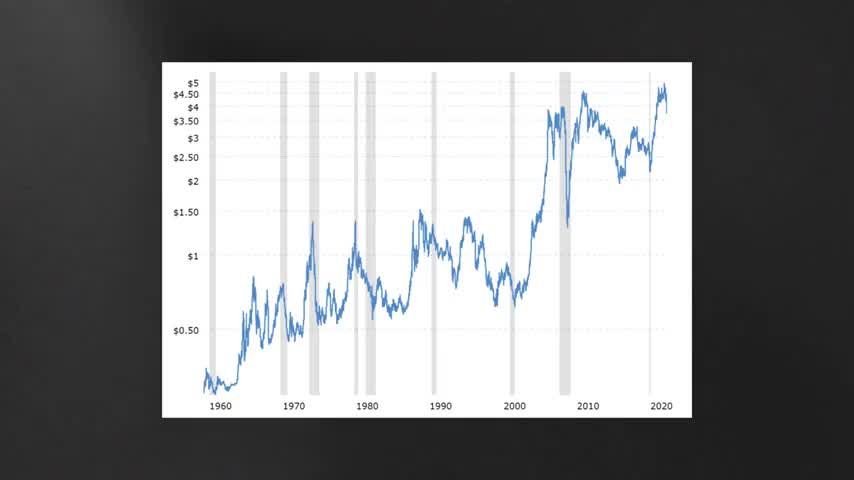

Oil Is Feeding Directly Into Inflation

Oil prices hit $113 a barrel last week. That is 80% higher than they were just a month ago.

That reality is already filtering into the prices of the rest of the economy. The price of corn, oats, and wheat are all up since the war started. The transmission channel is fertilizers. These rely heavily on oil and natural gas for their production, so higher energy prices directly filter into the price of food.

Although the moves in crop prices are small compared to what we have seen on oil, they are enough to make a considerable impact on overall inflation. Here is how this hits the consumer price index:

Those two components also have a significant indirect impact on the rest of the components, like the cost of services. The economy needs people in order to exist, and people require food and energy. Just this dynamic alone can already put a significant amount of pressure on Treasuries, since investors will ask for higher bond yields in order to compensate for that inflation.

But this is just the tip of the iceberg. There are significant forces working beneath the surface that have the potential to completely break the bond market and squeeze the financial system.

The Fed's Forced 180

What is happening in Iran is forcing the Federal Reserve to do a complete 180 on its monetary policy.

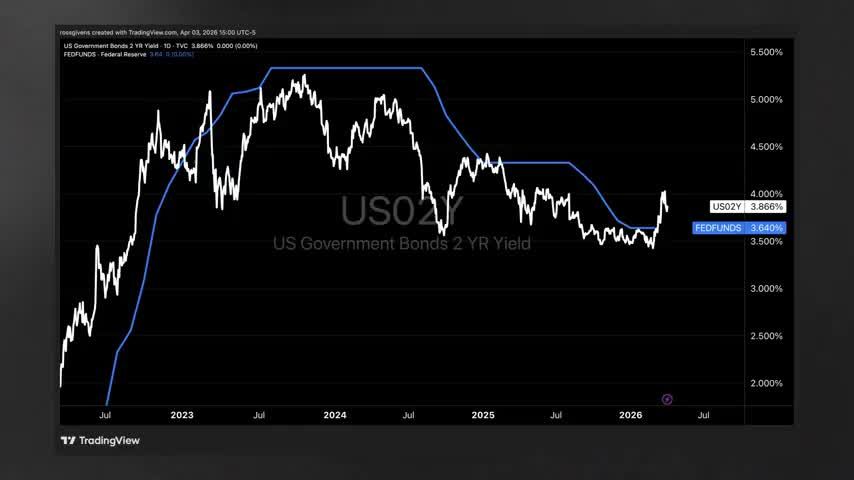

Since 2023, the Federal Reserve has been reducing interest rates, which has actually been stabilizing the bond market. This is something they have been able to do thanks to cooling inflation. The energy shock we are going through right now is completely flipping that around.

The 2-year Treasury yield is generally viewed as the expectation of future Fed policy. Since 2023, the big theme has been that the market has consistently expected the Federal Reserve to lower its interest rates. We can see that from the 2-year yield being below the Fed funds rate.

Now consider what happened in the five weeks since the war started. The 2-year yield has jumped back above the federal funds rate.

The last time the Federal Reserve was hawkish and the 2-year yield was above the Fed funds rate was in 2022. Interest rates jumped from 1% to 5% in a year. That put a lot of pressure on the financial system. It is not a coincidence that bond yields are breaking out right now as the Federal Reserve is about to become hawkish once again.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWhat Bond Market Warning Signal Is the Iran War Sending?

How bad can this actually get? How much damage can the war do to the bond market, and what consequences will that have?

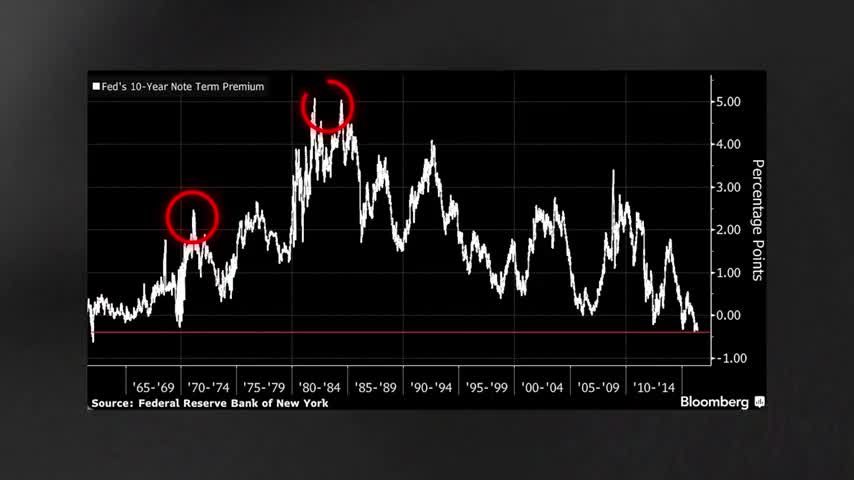

There are three forces that actually drive bond yields. Inflation is the biggest one, the one primarily taken into account by investors. Second is the federal funds rate, set by the Federal Reserve, which takes into account inflation but also the health of the labor market. And finally, there is something called the term premium, which is essentially the confidence that private investors have in US debt.

Although you might not have heard of it, the term premium is what could do real damage to the bond market today. It tells us how much extra compensation bond investors are asking on top of the other two factors at any point in time.

Think of it as the added bonus interest that investors ask for depending on whether they believe the bond market is risky or not. If investors have confidence in the stability of the Treasury market, the term premium is going to be low. In 2019, it was actually negative. Confidence in US bonds at that time was unbelievably high. If investor confidence is low, however, the term premium rises. Historically, it has gone as high as 5% in the US, and this typically happens during times of war or heightened geopolitical uncertainty.

Today, the term premium is hovering just under 1%. Which reflects, frankly, a lot more optimism than I have in the US Treasury market.

The spikes in 1973, 1979, and 1990 matter because those were the last three major oil shocks the global economy has been through. In each and every one, the term premium was above 2%.

This is potentially a major tail risk to the bond market today. If this is not over quickly, it could cause term premiums to start rising quickly back up to 2%, even 3%. The iran war bond market disruption could push yields to levels not seen in decades.

What Happens When Yields Hit 6-7%?

The 30-year Treasury yield is currently sitting at 5%. A 1% to 2% jump in the term premium would mean 30-year bond yields reach 6% or 7%, levels we have not seen in over 30 years.

A spike in bond yields like that would almost certainly bring mortgage rates up along with it. It would also raise borrowing costs for businesses. Treasury bond yields are the risk-free rate, the floor for all other kinds of interest rates across the economy. When these rise, the cost of capital rises everywhere else too, and it tightens the economy considerably.

This is why rising government bond yields often trigger economic recessions in the US, just like they did in the 1970s, 80s, and early 2000s.

We are not there yet. The bond market is not fully broken. But every week the oil shock persists or gets worse, the risk of the bond market actually breaking rises. The iran war bond market stress is something every investor should be watching closely.

Where Is Money Rotating During the Iran War Selloff?

No need to panic. The play is to position in areas that do well under exactly these conditions.

As money flees from the bond market, bond prices fall, causing bond yields to spike. That is what damages the economy. But that money is not going into checking accounts. It is actually rotating to other parts of the economy. This is where I am shifting my attention, where I believe some of the most attractive investment opportunities exist today.

The Case for Copper

I have been extremely bullish on copper for almost a year now. I own 25 tons of it.

In the 1960s and 70s, copper tripled in price. This happened alongside oil shocks, a bond market collapse, and recessions. The reason is simple: investors were panicking out of financial assets into real, tangible things, things that were needed in the real economy. The companies mining and producing that copper saw their stock prices skyrocket as a result.

I expect to see the same in the second half of this decade. We know that there is going to be a shortage of copper in the coming years thanks to underinvestment in the space combined with a massive jump in demand from data centers and electrification.

To fully take advantage of this, you want to own companies whose profit margins expand as a result of the rise in copper prices. That means the miners. If copper does what I think it will, these companies have the potential to 5x or 10x in price. Here are three of my favorites:

Freeport-McMoRan (FCX) is the largest US copper producer. They work a massive Moreny mine in Arizona. They are the industry leader.

Southern Copper Corporation (SCCO) is number two, headquartered in Phoenix. This company has significant revenue and several new projects in the pipeline.

TCO Mines (TGB) is a higher-risk, higher-reward type bet. This is a $2 billion Canadian operator whose stock is up big with no signs of slowing down. The company's Florence copper project in Arizona is nearing full operation with some of the lowest cost metrics in the industry. Almost 100% of TCO's output is copper, making it one of the purest plays in the space.

For diversification, the Sprat Copper Miners ETF (COP) does the job. It holds all three of these stocks along with 58 others.

I have 60% of my retirement account allocated to metals, energy, and infrastructure. Even the 40% equity bucket is weighted heavily to emerging markets with commodity-rich economies. Even after the selloff we went through in March, I am still beating the market by over 10% this year.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- A 5% drop in US bond prices since the Iran conflict began has erased roughly $1.5 trillion in Treasury market value — a move most equity investors are ignoring.

- TLT (20+ Year Treasury Bond ETF) sold off from ~$91 to ~$86.77, and the 30-year Treasury yield is pushing back above 5% — a level that has historically triggered broader financial stress.

- Oil hitting $113 a barrel — up 80% from recent levels — is feeding directly into inflation expectations, which puts upward pressure on yields and makes the Fed's position increasingly untenable.

- The presenter has rotated 60% of his retirement portfolio into metals, energy, and infrastructure, with the remaining 40% equity allocation weighted toward commodity-rich emerging markets — a positioning he says is beating the market by over 10% year-to-date.

- Three unnamed defense/commodity-related stocks are flagged as buy opportunities at 20–25% off their highs, with the Sprott Copper Miners ETF cited as a diversified entry point holding all three plus 58 additional names.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources