Hey, Ross here:

Ackman just signaled that two specific stocks could multiply your money by ten times. The billionaire hedge fund manager posted his thesis Sunday night, and the market responded immediately. Both stocks surged 50% on Monday. If you're looking at any Fannie Mae stock forecast right now, the fundamental math behind this setup is hard to ignore.

In all likelihood, this initial surge is just the beginning.

The two companies: Fannie Mae (FNMA) and Freddie Mac (FMCC). Ackman runs one of the largest and most successful hedge funds on Wall Street. When he speaks, the smart money listens. Some of his big ideas have successfully 10Xed in the past. Right now, his Fannie Mae thesis is pretty compelling, and the fundamental math backs up every single claim he is making.

I'm putting $10,000 into each of these stocks at the open. The two opportunities in front of us are clear.

Why Does Ackman Think Fannie Mae Stock Could 10X?

Bottom Line: Ackman's thesis rests on a straightforward valuation mismatch, two companies earning $25 billion annually priced at less than half their yearly profit, with a privatization catalyst that could force institutional buying at scale. The 10X target assumes a successful exit from government conservatorship and relisting, which remains a political and regulatory risk, not a certainty. Investors evaluating any Fannie Mae stock forecast should weigh the asymmetric upside against the real possibility that conservatorship drags on indefinitely.

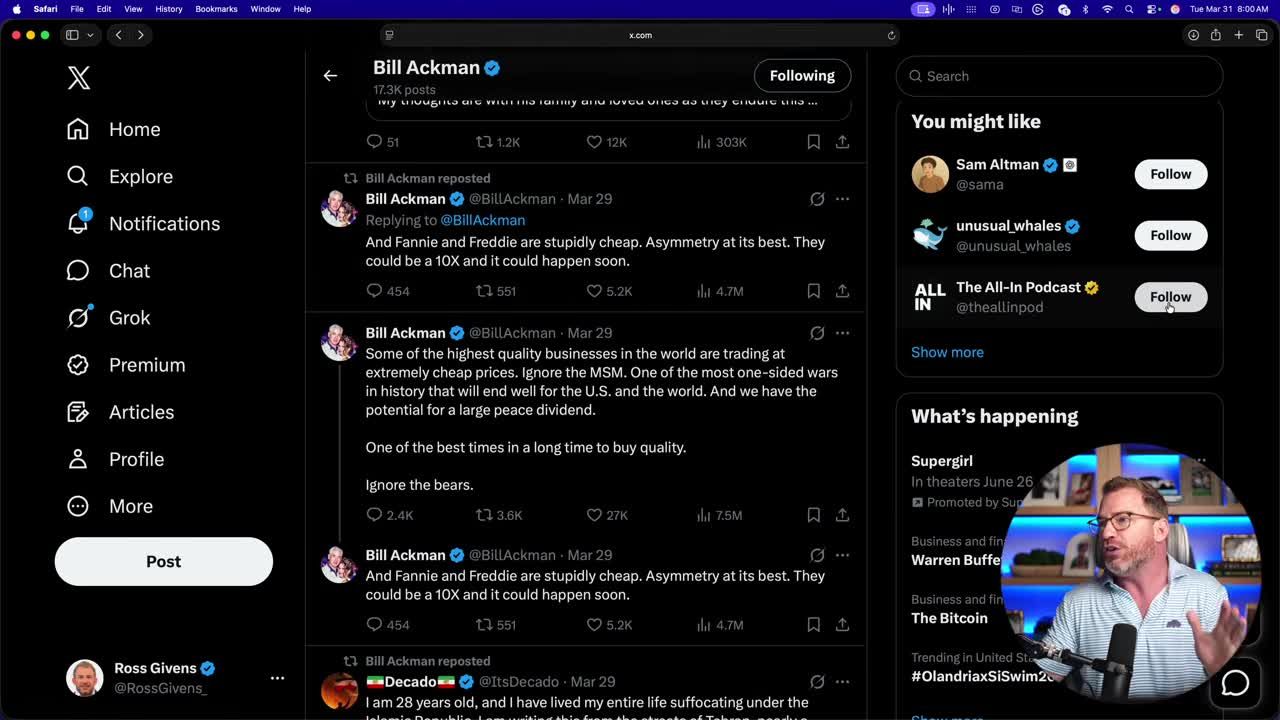

Ackman believes Fannie Mae and Freddie Mac are "stupidly cheap" and represent asymmetry at its best. He explicitly stated these stocks could be a 10X opportunity, and that the move could happen soon.

Ackman pointed out that some of the highest-quality businesses in the world are trading at extremely cheap prices. His advice: ignore the mainstream media and ignore the bears. This is one of the best times in a long time to buy quality.

This is not a small, speculative bet for Ackman. This is one of the largest positions in his very concentrated portfolio. The broader market clearly agrees with his assessment, given the 50% single-day price jump we just witnessed.

The Peace Dividend

A major component of Ackman's thesis revolves around a coming "peace dividend."

Right now, the market is pricing in the unknown regarding the ongoing situation with Iran. Ackman describes this as one of the most one-sided wars in history that will end well for the US and the world.

Once the Iran situation comes to some sort of resolution, the market is going to soar on that news. The removal of that unknown will act as a release valve. When that uncertainty vanishes, quality stocks are going to make almost instant big moves higher. Fannie Mae and Freddie Mac are perfectly positioned to ride that exact wave.

What Are They Actually Worth?

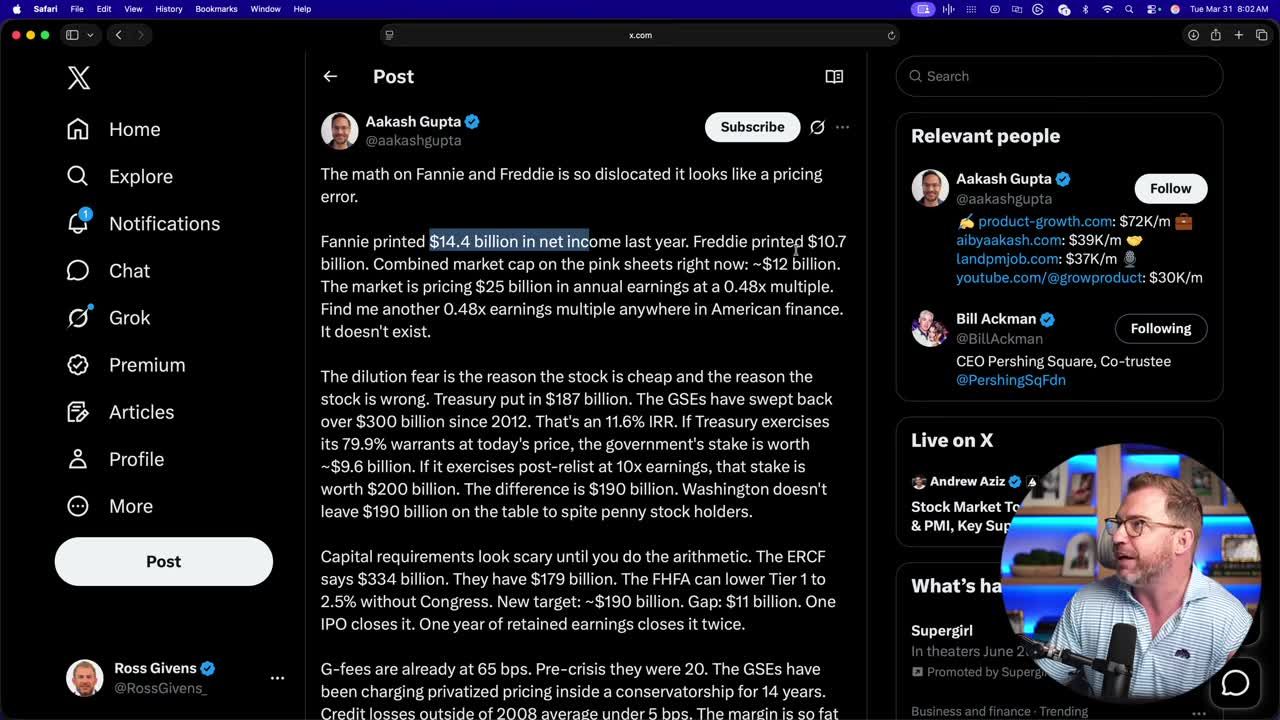

To understand the real Fannie Mae stock forecast, you have to look at what you're actually getting for your money. Value investor Akash Gupta laid out the investment case for these two stocks in detail.

The net income numbers are staggering:

Despite generating $25 billion in net income, the combined market cap to buy both companies outright is just $12 billion.

You are literally buying these companies for half of one year's earnings. That is a 0.48x multiple.

To put that into perspective, the average stock in the market usually trades at 15 to 20 times earnings. Quality companies routinely trade at 25, 30, or even 40 times earnings. You are buying Fannie and Freddie for half of one times earnings. The valuation mismatch is almost unbelievable.

What Happens to Fannie Mae Stock If It Gets Relisted?

If the 10X thesis plays out, the stocks must move off the pink sheets.

Currently, FNMA and FMCC trade over-the-counter. They are not publicly traded on the New York Stock Exchange. This OTC status is a big reason for the current discount. Institutional money simply cannot touch them right now.

That changes the moment privatization and relisting occur. If these entities get listed on the major exchanges, they instantly become investment-grade securities.

Here is exactly what happens next:

1. Index Fund Inclusion

Once they hit the NYSE, they will be added to major market indexes.

2. Mandatory Institutional Buying

Every single index fund and pension fund with a financial sector mandate will have to buy them. They will have to gobble up shares of the two most profitable companies in America.

3. Valuation Surge

That wall of forced institutional buying will cause the valuation to surge. They are currently sitting on the pink sheets waiting for one signature.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWill Government Dilution Kill the Fannie Mae Trade?

Why the market is pricing these stocks so cheaply

The market rarely gets things this wrong without a reason. The primary risk keeping prices suppressed is the fear of shareholder dilution.

These used to be government entities. The Treasury put money into them to keep them afloat. Since then, the government has swept back around $300 billion on that investment.

However, the Treasury still holds warrants. These warrants are basically call options that allow the government to accumulate shares at dirt-cheap prices. They hold an 80% stake in the companies.

The Trump administration has shown they have no problems playing the equity market. Just in the last 12 months, they have taken large stakes in multiple companies, primarily in the rare earth metals space. They see the exact same math we do. They are going to play along.

Dilution Math Still Works

Even if the absolute worst-case dilution scenario plays out, the Fannie Mae stock forecast remains bullish.

The exact math on the government exercising its 80% stake: taking the 80% would dilute current shareholders by 80%. This would effectively multiply the current market cap by five. Multiplying the $12 billion market cap by five brings the total post-dilution valuation to $60 billion.

Even at a $60 billion valuation, these companies are still making $25 billion in pure profit every single year.

Either way, it is an absolute steal compared to the 15 to 20 times earnings average of the broader market.

FNMA vs. FMCC

Both of these stocks offer the exact same fundamental setup, but the price action and net income differ slightly between the two.

Fannie Mae (FNMA): The larger earner, pulling in $14.4 billion in net income last year. The stock surged about 51% on Monday. It gapped up in the morning and ran higher all day long into the close, moving from around $5 up to about $7 a share. Pre-market indications showed it set to open about 70 cents higher.

Freddie Mac (FMCC): Pulled in $10.7 billion in net income last year. Currently trading around $7 a share. Back in September, Freddie Mac was at almost $15. Even with the 50% bump on Monday, the stock is still 50% off its highs. Pre-market indications showed it set to open about 50 cents higher.

Nothing about the fundamental story has changed since Freddie Mac was trading at $15. The discount is entirely sentiment-driven.

The Ultimate Low-Risk Spread

The underlying business model of Fannie and Freddie is arguably the best in the entire financial sector.

They collect guarantee fees, known as G-fees, at 65 basis points. Meanwhile, historical losses on these American mortgages sit under five basis points. That is 0.05%, or five one-hundredths of one percent.

You are buying a royalty on the American mortgage system. It is one of the most predictable spreads in all of finance. This spread is backstopped by a guarantee that both parties have publicly committed to preserving. The federal government will not let these loans fail.

Compare this setup to a traditional bank like JP Morgan. JP Morgan trades at 13 times earnings and takes real risk. Fannie and Freddie take virtually zero risk, have a government backstop, and trade at 2.5 times earnings fully diluted.

My Trading Strategy

I'm putting $10,000 into Fannie Mae and $10,000 into Freddie Mac right at the open.

The price action on Monday tells you everything you need to know about institutional interest. While the overall market index sold off all day long, Fannie Mae jumped up and ran steadily into the close. That is clear, undeniable outperformance. A textbook outlier stock.

These stocks are serious movers. The Average Daily Range (ADR) on Fannie Mae is about 12%. That means intraday volatility is high, and the stock can cover a lot of ground quickly.

Do not let the pink sheet status scare you away. This is a clear long-term play backed by one of the best investors of all time.

The Greatest Valuation Mismatch

The Fannie Mae stock forecast comes down to simple, undeniable math. You have two companies generating $25 billion in combined profit, trading at a $12 billion market cap.

Ackman sees the asymmetry. The smart money is already positioning for the relisting. When the index funds are finally forced to buy, you will want to already own your shares.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- Bill Ackman publicly called Fannie Mae (FNMA) and Freddie Mac (FMCC) 'stupidly cheap' and a potential 10X opportunity, triggering a ~51% single-day surge in FNMA on Monday.

- The core valuation argument: Fannie and Freddie generate $25 billion in combined annual profit but trade at a combined $12 billion market cap, roughly 0.5x earnings.

- Even in a worst-case dilution scenario where the government extracts a $200 billion payday, the presenter argues you're still buying a government-backed monopoly at just 2.5x earnings.

- FNMA trades on the OTC pink sheets with average daily volatility around 12%, meaning position sizing and entry price matter significantly more than with exchange-listed stocks.

- The bull case hinges on privatization and relisting: if Fannie and Freddie are returned to private ownership, index funds would be forced to buy, creating a structural demand surge for current shareholders.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources