Everyone's favorite meme stock is back in the headlines. The GameStop eBay takeover bid is officially on the table: a $56 billion offer for eBay. One glaring problem: they don't have the money.

This is not a legitimate business strategy. It is a calculated move by CEO Ryan Cohen to unlock a $35 billion payday for himself at the direct expense of GME shareholders. Buried inside one document that almost nobody seems to have read lies the exact blueprint for this wealth transfer.

If this deal goes through, it puts GameStop on the fast track to bankruptcy and completely wipes out current investors. The math makes zero financial sense. The dilution will be catastrophic.

Here is exactly how this scheme is designed to play out step by step, and the one signal that tells you whether to get out or profit from the fallout.

Why Doesn't GameStop's $56 Billion Bid for eBay Add Up?

Bottom Line: The GameStop eBay takeover bid is not a growth strategy. It is a compensation-driven maneuver where the CEO's contract creates a $35 billion personal incentive to force through a deal that the underlying math cannot support. Investors should read the executive pay package in GameStop's SEC filings before making any decision, because that document, not the press release, reveals whose interests this deal actually serves.

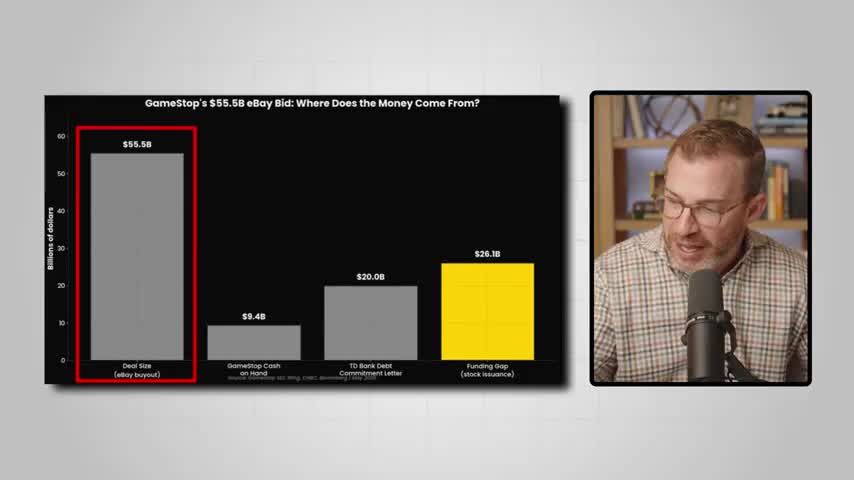

GameStop's offer is officially priced at $55.5 billion. Half cash, half stock. That equates to a buyout at $125 per share, a 20% premium over last week's close.

Initially, the retail crowd fired up. GameStop stock jumped on the news, and eBay jumped even harder. But the math falls apart the moment you look at actual valuations.

GameStop is worth about $10 billion. eBay is worth about $48 billion. You are looking at a company trying to swallow a target almost five times its size. The financial mechanics required to make this happen simply do not exist in reality.

Where Does the Money Come From?

The balance sheet does not support a $56 billion acquisition. Here is the exact breakdown of available capital:

That phrase matters: a "highly confident letter." Not a binding commitment. A letter stating the bank thinks it could provide up to $20 billion in debt financing if pressed.

Even if TD Bank delivers the full amount, add it up. Roughly $29 billion available. The deal requires $56 billion. Where does the missing $26 billion magically come from?

Cohen stated that half the deal is in the form of stock. But if he handed over all the GameStop stock in existence, every single share owned by every investor, the entire company is only worth $10 billion. That still leaves a massive $16 billion hole.

Cohen Can't Explain His Own Deal

When pressed on live television about this funding gap, the CEO could not explain it.

During a CNBC interview, Cohen was asked point blank how the math works. The hosts walked him through the exact numbers: an $11 billion market cap, $9 billion in cash, and a $20 billion non-binding letter from TD Bank. They pointed out the $16 billion shortfall. They noted the TD Bank letter is not locked financing.

His response? "We'll see what happens."

Since the CEO cannot explain his own financing, here is what he is going to do. He is going to issue stock. He will print enough new shares to dilute the absolute life out of every current shareholder.

The stock market quickly came to the exact same conclusion. After that interview aired, GameStop fell 11% in the first couple of hours of trading on Monday. Situations like this, where the headlines don't match the reality, are where a lot of money can be made by understanding what is actually happening underneath the surface.

How Does Ryan Cohen Make $35 Billion From the eBay Deal?

The real reason this deal exists: executive compensation bonuses.

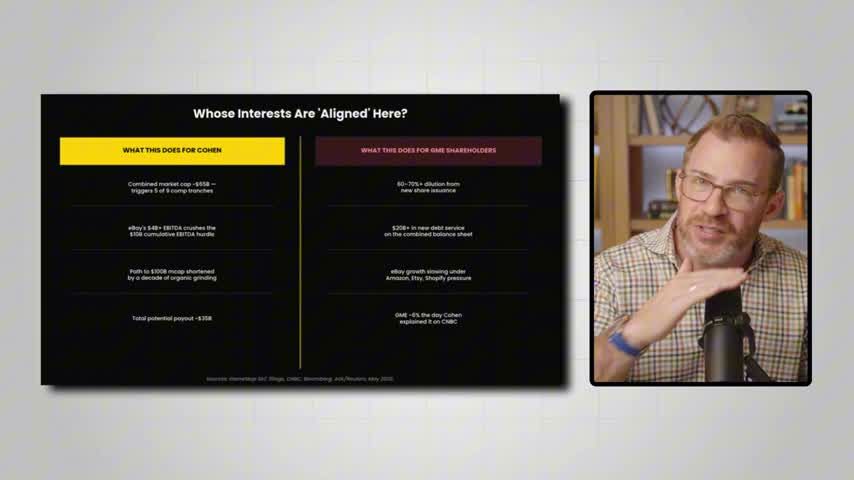

Back in January, GameStop's board awarded Ryan Cohen a Musk-style performance pay package. His entire compensation is at risk. No salary, no cash bonuses, no stock that just vests over time. He gets paid one way only: by hitting specific performance hurdles.

The award consists of 171.5 million stock options with a strike price of $20.66. This package is divided into nine separate tranches. Each tranche has two specific locks that must be opened.

- Lock 1, Market Capitalization: Tranche one vests when GameStop hits a $20 billion market cap. Tranche two requires $30 billion, then $40 billion, all the way up to $100 billion for the final tranche.

- Lock 2, Cumulative EBITDA: Earnings before interest, taxes, depreciation, and amortization. Tranche one requires $2 billion. The final tranche requires $10 billion.

Hit both locks, you unlock the tranche. Hit all nine for full vesting at a $100 billion market cap and $10 billion in cumulative EBITDA, and Cohen walks away with roughly $35 billion. That is billion with a B.

During the CNBC interview, Cohen stated his motivation clearly: "If I don't hit the thresholds, then I don't get anything."

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubThe Shortcut: Stapling eBay Onto GameStop

Stack the pieces and look at reality. GameStop today has a $9 billion market cap. To hit tranche one, Cohen needs $20 billion. He is nowhere close.

GameStop's EBITDA is somewhere around $100 to $120 million. He needs $2 billion just to hit the first tranche. At an organic pace, grinding through as a dying mall store business, that takes a decade. Maybe more. Maybe never.

This is where eBay comes in.

eBay has a market cap around $48 to $50 billion. Their annual EBITDA is north of $4 billion. A real platform business with real cash flow and real margins.

Bolt the two companies together, and the combined entity walks in with a $60 to $65 billion market cap on day one. That does not just unlock the first tranche. That puts tranches one, two, three, four, and maybe five all in play immediately.

The $2 billion EBITDA hurdle for tranche one? eBay clears that in six months by itself.

The pay package was designed and approved for one specific company at one specific size. By changing the size of the company through an acquisition, he changes the path to the payout. How the lawyers did not see this coming, I have no idea.

What Happens to GameStop Shareholders If This Deal Goes Through?

Assume the GameStop board allows him to follow through with this deal. What does that do to the people who own GameStop today? Three massive problems, and none of them are good.

1. Dilution of Biblical Proportions

GameStop currently trades at around $25 a share. To raise another $28 billion in stock at that price, the company would need to print over one billion brand new shares.

These new shares come on top of the 446 million shares that exist right now. We are talking about more than tripling the total share count. And that assumes the stock holds at $25. If it falls to $12 or $13, better make that two billion new shares.

Existing shareholders go from owning whatever percentage they hold today to roughly a third of that. Your slice of the pie shrinks by 60 to 70 percent. Same business, fewer claims per share.

2. A $20 Billion Debt Burden

If the $20 billion TD Bank financing materializes, it adds enormous interest expense to the combined company. eBay already carries debt of its own. GameStop is stacking $20 billion more on top.

That interest gets paid out of operating cash flow before any earnings reach shareholders. Notice how Cohen's compensation package is based on EBITDA, not actual profits. It was specifically designed to factor in company earnings before the interest is paid. He benefits while shareholders do not.

3. Extreme Execution Risk

eBay's growth is slowing. The platform is getting squeezed by Amazon, Etsy, Shopify, Temu, and Mercari.

Cohen has promised $2 billion in annual cost savings within 12 months of closing. He is drunk. This is a CEO who has never run an e-commerce platform business. There is absolutely zero chance he pulls that off.

Best case: the deal closes, synergies hit, the company runs efficiently, Cohen wins big, and shareholders maybe break even on a per share basis after the massive dilution.

Worst case: eBay's growth keeps slowing, synergies miss, and debt service eats the margins. The diluted share count means even decent profits show up as tiny earnings per share. And the stock price continues to climb as shareholders value the debt-ridden dinosaur for what it really is.

Financial Engineering on Steroids

This is the exploitation of shareholders for the benefit of one man. It is the exact opposite of what a CEO is supposed to do, which is to create value for shareholders.

If Cohen's interests were truly aligned with shareholders, he would offer all cash, borrow more, or sell GameStop assets to do this without the dilution. He won't do it. Why? Because his contract pays him to hit total market cap thresholds, not to deliver returns to existing shareholders.

His compensation comes directly from your pocket. Your shares become worth less to create his. Read the contract. Don't take my word for it. The contract tells you exactly what the executive is going to optimize for.

This is one of the most lopsided compensation packages I have ever seen. It will be studied in business school for years to come as a case study of what not to do.

What Happens Next: Will the GameStop eBay Takeover Bid Succeed?

This deal is simply too aggressive to close as proposed. The dilution is too steep. The financing is too thin. Cohen has not made a credible or legible case for it to anyone outside of his company. eBay's board will almost certainly negotiate, slow walk, or reject this entirely.

But Cohen has tipped his hand. The next move from him will not be smaller. He will take another swing at a target big enough to fast-track his $100 billion market cap goal.

If the GameStop eBay takeover bid fails, he will look elsewhere. Maybe Etsy. Maybe Wayfair. Maybe Carvana. Maybe a pre-IPO company. I doubt he even cares which one it is. He is going to move fast because after this week, he knows his time as CEO is limited unless he pulls off a miracle.

This is a massive wake-up call for investors. Take your time and read the CEO's pay package. That contract tells you exactly what the executive is going to do. It tells you whether their interests are truly in line with shareholders.

You can find GameStop's SEC filings, including executive compensation disclosures, through the SEC's EDGAR database.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- GameStop's $55.5 billion bid for eBay is structured as half cash, half stock at $125 per share, a 20% premium over eBay's last close, but GameStop itself is only worth roughly $10 billion, making the target nearly five times the size of the acquirer.

- Ryan Cohen's compensation contract contains a bonus tranche tied to deal execution that could deliver a $35 billion personal payday, creating a direct conflict of interest with GME shareholders who would absorb the dilution and debt.

- The stock component of the deal requires massive share issuance, which means catastrophic dilution for current GameStop investors regardless of whether the acquisition ultimately succeeds or fails.

- Cohen cannot clearly explain the operational or financial rationale for combining a brick-and-mortar gaming retailer with a global e-commerce marketplace, which is itself a red flag about the deal's legitimacy as a business strategy.

- The one protective clause for shareholders: if Cohen is removed before hitting his bonus tranche, he collects nothing, meaning board pressure or shareholder activism could neutralize the payout before it triggers.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources