OpenAI is set to go public later this year at a valuation north of $800 billion. The insiders will cash out and become famously rich. But beneath the surface, this company is a ticking time bomb, and the OpenAI IPO overvalued narrative is gaining serious traction among informed investors.

The math is not working. The leadership has a documented history of deception. And the upcoming stock offering looks like a classic setup to transfer retail money to insiders before the wheels come off.

In my 20 years as a stock trader, I have watched a lot of IPOs come and go. Most were legitimate businesses going public at reasonable valuations. Others were hype machines designed to transfer retail money to insiders before the wheels came off. I will let you decide which category this one falls into after you see the data.

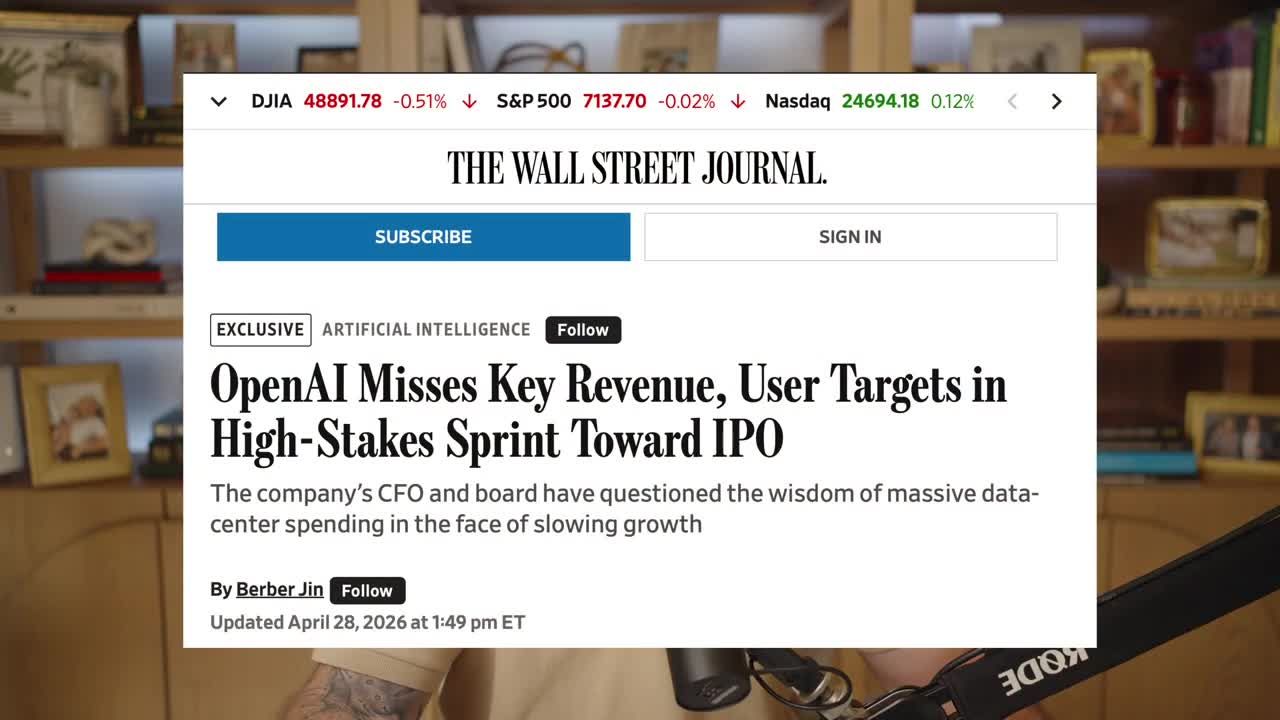

The Wall Street Journal just published an article exposing the problems at OpenAI. The Reddit boards are lighting up. A post on the WallStreetBets sub forum quickly shot to number one, and the comments are brutal. The investment banks are not telling you the full story about Sam Altman and this IPO.

Is the OpenAI IPO Overvalued at an $800 Billion Valuation?

Bottom Line: OpenAI is asking the public to pay up to $1 trillion for a company that is not profitable, is missing its own internal targets, and is led by someone with a documented history of removal for deception. The numbers alone make the OpenAI IPO overvalued case compelling, but the leadership track record makes it significantly harder to justify the risk premium retail investors would be taking on.

Wall Street is asking retail investors to value OpenAI between $800 billion and $1 trillion. That is a staggering number for a business that will not be profitable for at least four more years.

The company is pricing this stock for absolute perfection. The reality behind closed doors is far from perfect.

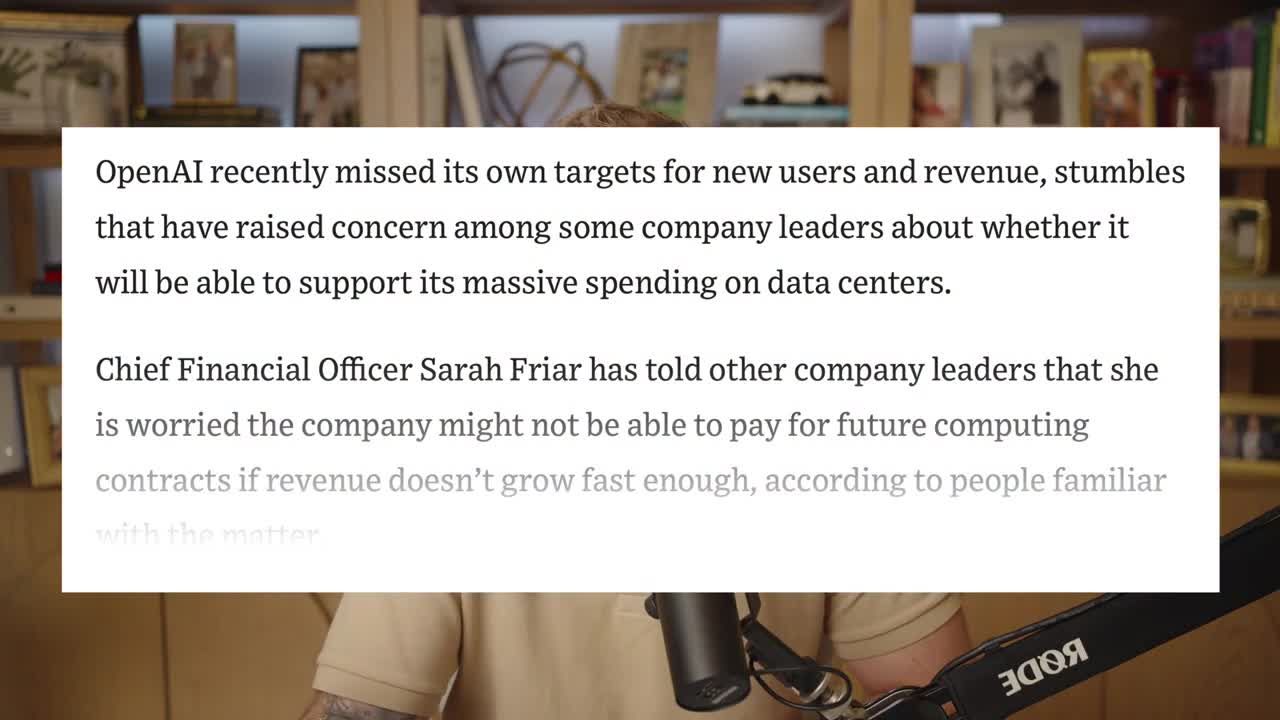

The Wall Street Journal reported on Monday that OpenAI missed multiple internal revenue targets earlier this year. They also missed their goal of reaching 1 billion weekly active users for ChatGPT by the end of 2025.

This is exactly what we saw during the dot-com era. Wall Street asked retail investors to buy into companies burning billions a year, trading at 43 times sales on the promise of profitability years into the future. We know exactly how that ended. The math is simply not mathing.

Can OpenAI Pay Its Own Bills?

Yes, this is a real concern coming directly from the company accountant. The chief financial officer, Sarah Friar, has reportedly expressed concerns to company leadership that OpenAI might not be able to pay for its own future computing contracts if revenue does not grow fast enough.

When the story broke, Altman and Friar put out a joint statement calling the report "ridiculous." That is the exact same word the board used to describe Altman's explanations in November 2023.

The collateral damage in the market could be massive. Consider Oracle, ticker OCL. Oracle signed what was described as the largest cloud computing deal in history with OpenAI, $300 billion. Oracle is building out $135 billion in AI hardware infrastructure to support it.

For Oracle stock, the entire bull case right now is predicated on that deal converting into real money. Yesterday, Oracle stock dropped 7% pre-market on this OpenAI news. The logic is simple: if OpenAI cannot pay its bills, Oracle turns into a collections agency trying to scoop up $300 billion. Oracle shareholders understandably got spooked.

The Sam Altman Pattern

Sam Altman has a documented history of being fired for deception. He has been pushed out of two other companies for the exact same reason before the OpenAI board fired him in 2023.

The investment banks want you to focus on the shiny AI products. You need to look at the man running the company.

Strike One: Loopt

Altman's first company was a location-sharing app called Loopt. He ran it for seven years. The board tried to remove him as CEO twice. The company never gained meaningful traction. In 2012, it was sold for peanuts, and nearly every early investor lost money.

Strike Two: Y Combinator

Altman became president of that famous startup accelerator. In 2019, he was again pushed out. Partners alleged he constantly lied. One investor who spoke to the New Yorker stated clearly that it is a "policy of Sam first."

Strike Three: OpenAI

In November 2023, the OpenAI board of directors fired Altman. They did not lay him off. He did not quietly resign. They point-blank fired the man. The official statement said he was "not consistently candid with the board." In other words, he was lying.

The board also revealed that they learned about the launch of ChatGPT on Twitter. Altman had even hidden his ownership of the OpenAI startup fund from the board entirely. Yet somehow, this Machiavellian trickster managed to get himself reinstated within five days. He even had the board members who fired him removed.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubIs OpenAI Actually Hitting Its Revenue Targets?

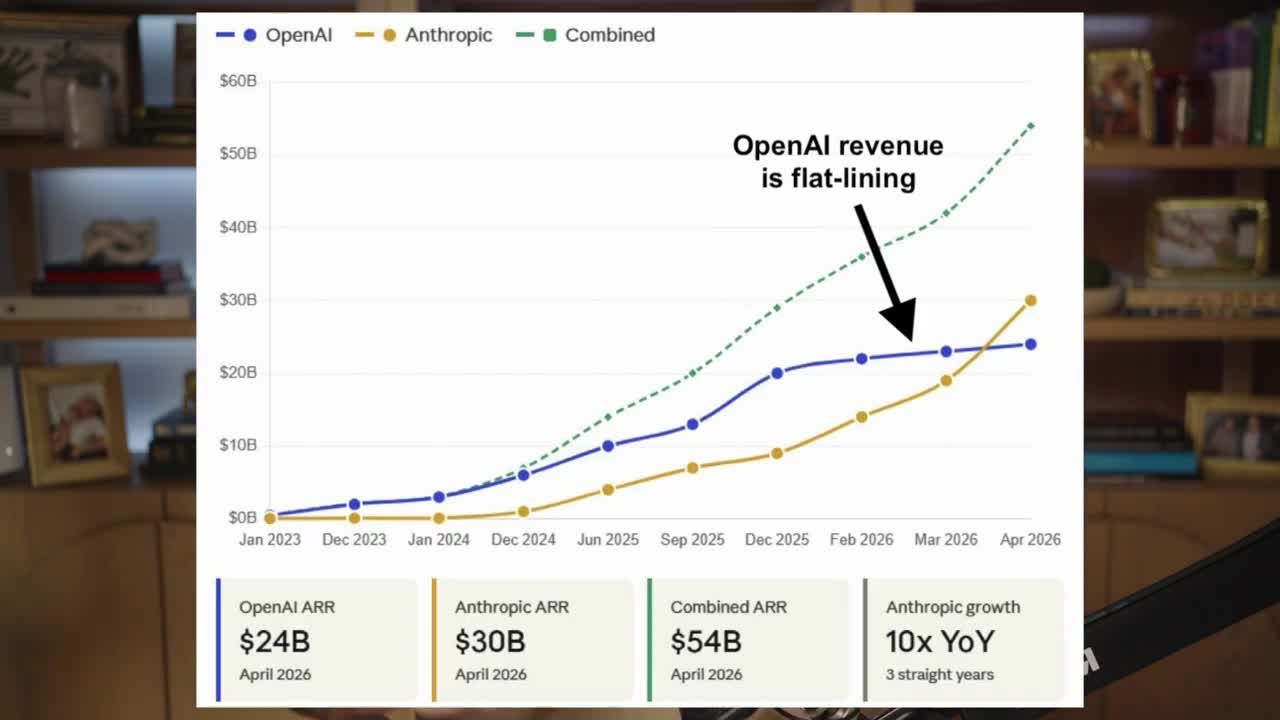

The revenue numbers look impressive on the surface. The internal targets tell a completely different story, and they reinforce why many believe the OpenAI IPO overvalued thesis is correct.

The CFO announced in January that annualized revenue crossed $20 billion in 2025. The historical growth is undeniable: $2 billion in 2023, $6 billion in 2024, $20 billion in 2025. That is triple-digit growth. $20 billion is a lot of money.

But what the CFO did not say in that press release was that they are already missing their 2026 targets.

The internal goal for this year, 2026, was $30 billion. That represents a fraction of the growth they have seen in previous years. And they are not even hitting that. The Wall Street Journal reported this week that they have missed multiple monthly revenue targets this year.

Competitors like Anthropic and Google are gobbling up market share. ChatGPT is genuinely the fastest adopted consumer technology in history. The product is very much real. But so was the BlackBerry. That did not stop competitors like Apple and Samsung from making superior products. We are seeing exactly that happen today with Claude, Gemini, Perplexity, and many others.

The Musk Lawsuit

Opening arguments are underway this week in Oakland federal court in Musk v. Altman. Elon Musk is suing Sam Altman, accusing him of running a "long con" and seeking $150 billion in damages. He wants the court to consider unwinding OpenAI's entire restructuring.

The lawsuit accuses Altman of assiduously manipulating Musk into co-founding OpenAI with promises that it would be safer and more open than profit-driven tech giants. Altman promised OpenAI would remain a nonprofit dedicated to safety. Then he converted it to a for-profit structure. Musk's lawsuit describes this as a long con restructuring that made Altman personally worth billions.

A 2017 diary entry from co-founder Greg Brockman has already surfaced in court. It reportedly describes the nonprofit commitment as a "lie."

Even if Musk loses this suit, which is entirely possible, every single day of this trial is a day of testimony about internal OpenAI documents. It exposes Sam Altman's private communications and the gap between what was promised and what has actually happened. This is not good timing for an IPO roadshow.

The Safety Team Implosion

While Altman was restructuring the company for profit, his own safety team was hollowed out. In May 2024, Ilya Sutskever, the co-founder and chief scientist who built the core technology, resigned. Days later, the head of AI alignment quit publicly. He wrote that at OpenAI, "Safety culture and processes have taken a backseat to shiny products."

The company then dissolved the entire super alignment safety team. The man who told the world OpenAI existed to make artificial intelligence safe fired the people making it safe.

Could OpenAI Run Out of Money Before Turning a Profit?

Altman is spending money like a drunken sailor, and the cash burn is reaching catastrophic levels.

This spending does not even include the compute commitments they have already signed. OpenAI has committed to $1.4 trillion in computing costs over the next several years, including the $300 billion Oracle deal. Where is this money coming from? No wonder the CFO is expressing concerns about whether they can pay their bills.

According to OpenAI's own internal projections, the company will not turn a profit until 2030. Deutsche Bank released an analysis projecting that OpenAI will burn through $143 billion in cumulative negative cash flow between now and 2029 before it finally turns the corner.

In plain English: the company needs to raise hundreds of billions of dollars in additional capital just to stay on its current trajectory. This company has massive insolvency risk. They are pricing this stock for perfection, but the fundamentals point to a financial disaster.

How to Position Yourself: Why the OpenAI IPO Overvalued Case Matters

This environment requires strict discipline. You cannot let the hype machine dictate your portfolio decisions.

1. Avoid the IPO Entirely

My read on the OpenAI IPO is simple. Avoid it like the plague. I would never buy this stock. The insiders will cash out and become famously rich. The retail investors will be left holding the bag if these wildly optimistic projections do not materialize.

2. Monitor the Infrastructure Collateral Damage

The real trades are in the ripple effects. Watch the companies tied to OpenAI's massive spending commitments. Oracle is a prime example. If OpenAI defaults on its $300 billion cloud deal, the entire bull case for Oracle stock takes a massive hit. The 7% pre-market drop is just a preview of what happens if these compute bills go unpaid.

3. Demand Executive Integrity

Do not invest in known charlatans who are famously loose with the truth. Altman told developers in January 2024 to build for AGI, claiming it was coming in 2025. 2025 came and went. No AGI. He spent the last year promising things that never happened. When the math does not work, this specific kind of Silicon Valley executive is very skilled at making sure the consequences land on someone else.

A Retail Investor Trap

The board that fired Altman got fired. The safety team that raised concerns got dissolved. The co-founder who compiled evidence of deception was pushed out. Now the CFO who is privately worried about the bills is being publicly called "ridiculous" for saying it out loud.

Warren Buffett famously said that in looking for people to hire, you look for three qualities: integrity, intelligence, and energy. And if they do not have the first one, the other two will kill you.

OpenAI has genuinely important technology. ChatGPT changed the world. There is no question they built a great product. But when someone has been fired for deception, pushed out of two other organizations for the same thing, and is currently sitting on trial for essentially fraud, maybe do not give him a trillion dollars. The OpenAI IPO overvalued argument is not just about the numbers. It is about the person asking you to trust him with your money.

Do your own homework. This stock is a time bomb.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- OpenAI is targeting an IPO valuation between $800 billion and $1 trillion despite not being profitable, making it one of the most aggressively priced tech offerings in recent memory.

- The Wall Street Journal reported that OpenAI is missing key internal revenue and user targets ahead of its IPO, with internal concerns flagged over data-center spending amid slowing growth.

- Sam Altman was previously removed from OpenAI's board over documented concerns about deception, and is currently named in litigation that critics describe as essentially a fraud case.

- The OpenAI IPO structure raises classic insider-exit red flags: insiders stand to cash out at peak valuation while retail investors absorb the downside if growth targets continue to slip.

- The overvaluation argument is not purely financial. It combines deteriorating revenue fundamentals with serious governance and leadership credibility concerns at the top of the organization.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources