You've probably experienced this before: you buy a plain call option expecting a stock to rise, the stock barely moves, and your option expires worthless. We see new traders face this frustration constantly when they rely solely on single-leg options. Buying naked options can drain your account quickly if the market doesn't move exactly as you predict. There's a better approach, and we're going to walk you through it step by step. By the end of this guide, you'll understand how to structure vertical spreads, calculate your exact risk before entering a trade, and apply these strategies to real market scenarios with confidence.

What Is a Vertical Spread and How Does It Work?

Bottom Line: Vertical spreads solve the core problem with single-leg options trading: unlimited downside exposure relative to the premium paid. By combining a long and short option at different strikes, traders lock in a defined risk profile before the trade even opens. The practical takeaway is that managing exit timing, specifically closing 3 to 5 days before expiration, is just as important as the entry structure itself.

A vertical spread is a multi-leg options strategy that limits both your potential gains and potential losses. You create this position by buying one option and selling another option of the exact same class. Both legs must share the same underlying stock and expiration date, differing only by strike price.

This strategy works because the option you sell helps pay for the option you buy. We teach our members that this structure acts like a financial shock absorber. The premium you collect from the short leg reduces the overall cost of the long leg.

If you buy a standalone option, you face a total loss of your premium if the stock moves against you. With a vertical spread, your risk is strictly capped from the moment you enter the trade. These are widely known as defined risk options strategies, making them highly accessible for beginner traders who want to control their downside exposure.

Key Concept: A vertical spread involves buying and selling options of the same type, on the same stock, with the same expiration date, but at different strike prices. Your maximum risk and maximum reward are both known before you place the trade.

What Are the Four Types of Vertical Spreads?

There are four primary ways to build a vertical spread. Your choice depends entirely on whether you expect the stock to go up or down, and whether you want to pay upfront (debit) or collect premium upfront (credit).

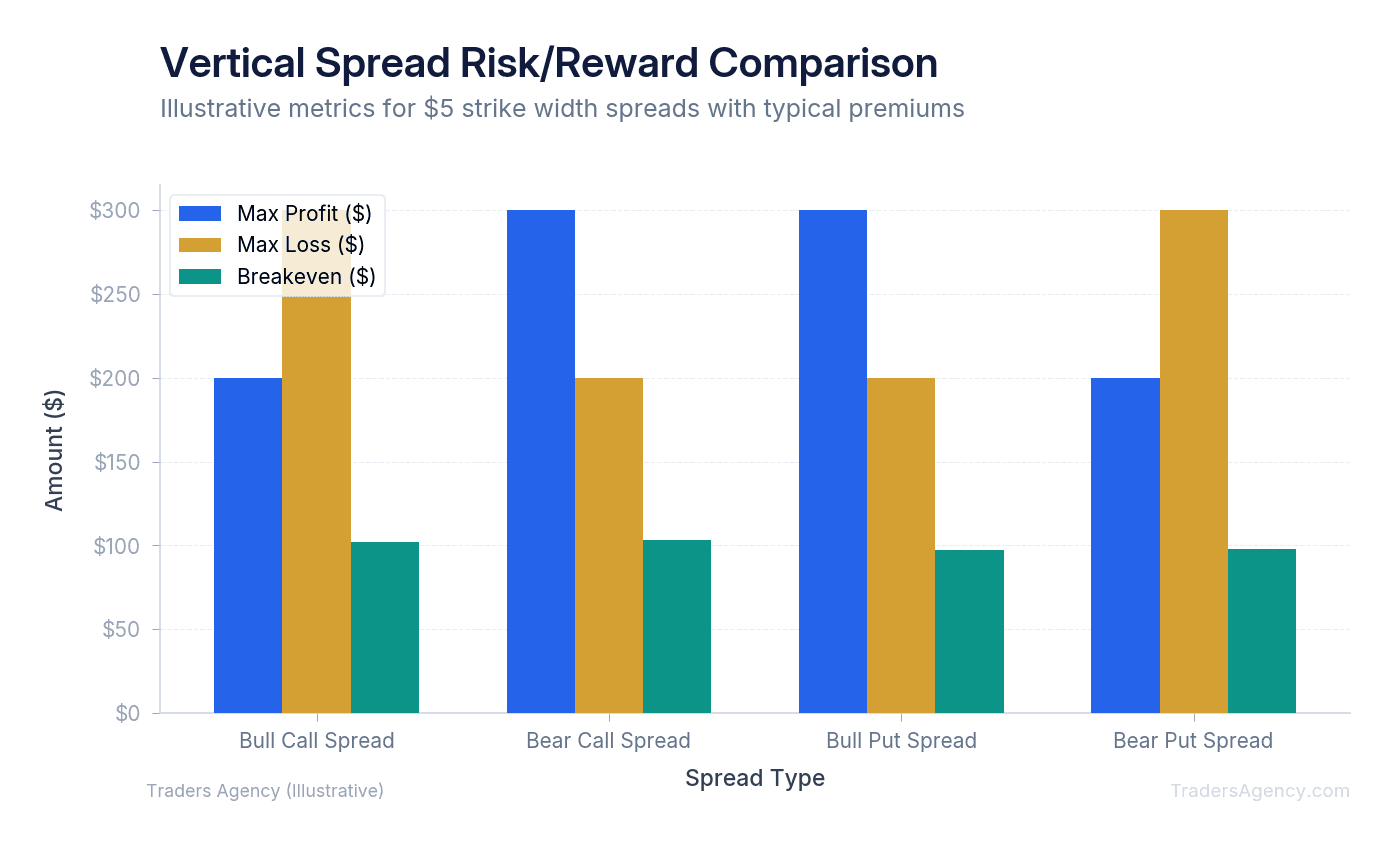

- Bull Call Spread: You buy a call option and sell a higher strike call. You want the stock price to rise.

- Bear Put Spread: You buy a put option and sell a lower strike put. You want the stock price to fall.

- Bull Put Spread: You sell a put option and buy a lower strike put. You want the stock price to stay above your strikes.

- Bear Call Spread: You sell a call option and buy a higher strike call. You want the stock price to stay below your strikes.

Understanding bull put spread mechanics and how a bear call spread works in simple terms will help you generate steady income. These are credit spreads, meaning you get paid upfront to open them. We often use credit spreads when we expect a stock to trade sideways or stay within a specific range.

How Do Debit and Credit Spreads Compare?

Debit spreads require you to pay money upfront to open the trade, meaning your maximum loss is the initial cost. Credit spreads pay you money upfront, meaning your maximum profit is the initial premium collected. Both strategies offer strictly capped risk and reward profiles.

When you trade a bull call spread or a bear put spread, you are using a debit spread. We prefer to use debit spreads when we expect a large, aggressive move in the stock. You're paying for the right to participate in that directional move, but your cost is discounted by the option you sold.

When you trade a bull put spread or bear call spread, you are using a credit spread. You must monitor credit spread risk closely. Your maximum loss on a credit spread is the difference between your strike prices minus the premium you collected. We typically use credit spreads when we want time decay to work in our favor.

| Spread Type | Direction | Debit or Credit | You Want the Stock To... |

|---|---|---|---|

| Bull Call Spread | Bullish | Debit | Rise above the long strike |

| Bear Put Spread | Bearish | Debit | Fall below the long strike |

| Bull Put Spread | Bullish/Neutral | Credit | Stay above the short strike |

| Bear Call Spread | Bearish/Neutral | Credit | Stay below the short strike |

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyStep-by-Step Example: Bull Call Spread

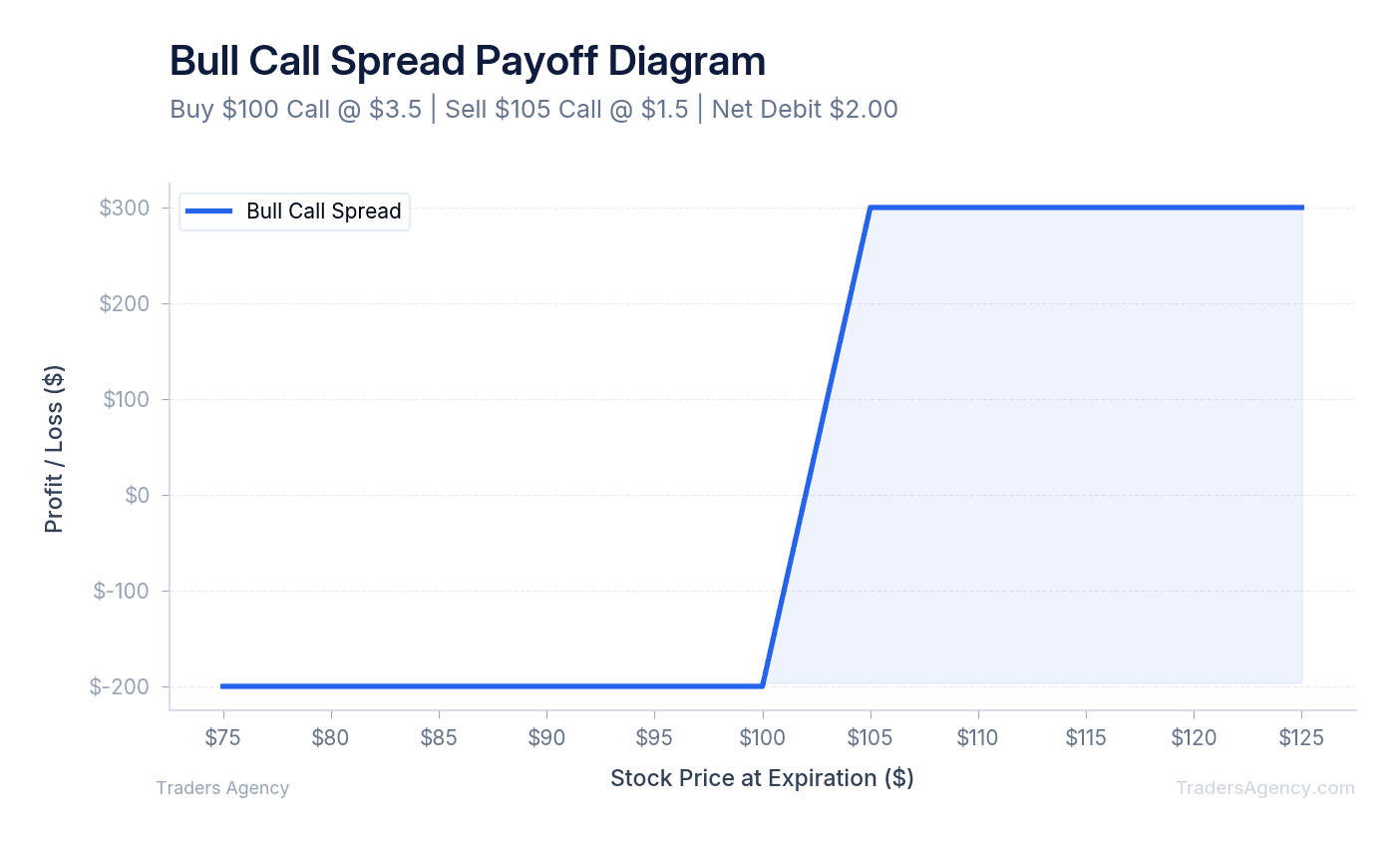

Let's look at a concrete example using a hypothetical stock, XYZ Corp, currently trading at $50 per share. We expect the stock to rise moderately over the next month and want to participate in this upward move without risking too much capital.

- Identify the Setup: We want to limit our upfront cost while capturing upside potential. We decide to use a bull call spread expiring in 30 days. We buy one $50 strike call for $3.00 and sell one $55 strike call for $1.00. Since one standard options contract controls 100 shares, the $50 call costs us $300 and the $55 call pays us $100. This gives us a $5 wide spread.

- Execute the Trade: We execute both trades simultaneously as a single vertical spread order through our broker. Our net cost is the difference between the two premiums. We pay $3.00 and receive $1.00, making our net debit $2.00 per share, or $200 total. This $200 is our absolute maximum loss. We can never lose more than this amount, no matter how far the stock drops below $50.

- Calculate the Outcome: To find our breakeven point, we add our net debit ($2.00) to our long strike ($50). Our breakeven is $52.00. The stock must rise above $52 for us to profit at expiration. Our maximum profit is the distance between the strikes ($5) minus our net debit ($2.00), which equals $3.00 per share, or $300 total.

| Parameter | Value |

|---|---|

| Stock | XYZ Corp at $50 |

| Long Call | $50 strike, $3.00 premium paid |

| Short Call | $55 strike, $1.00 premium received |

| Net Debit (Max Loss) | $200 |

| Breakeven | $52.00 |

| Max Profit | $300 |

| Scenario | Stock Price at Expiration | Profit/Loss |

|---|---|---|

| Best Case | $55 or higher | +$300 |

| Breakeven | $52.00 | $0 |

| Worst Case | $50 or lower | -$200 |

If XYZ Corp closes at $56 at expiration, both options are in the money and we make our maximum profit of $300. If the stock drops to $45, both options expire worthless and we lose our initial $200. Calculating vertical spread profit and loss is always this straightforward.

How Do Greeks Affect Your Vertical Spread?

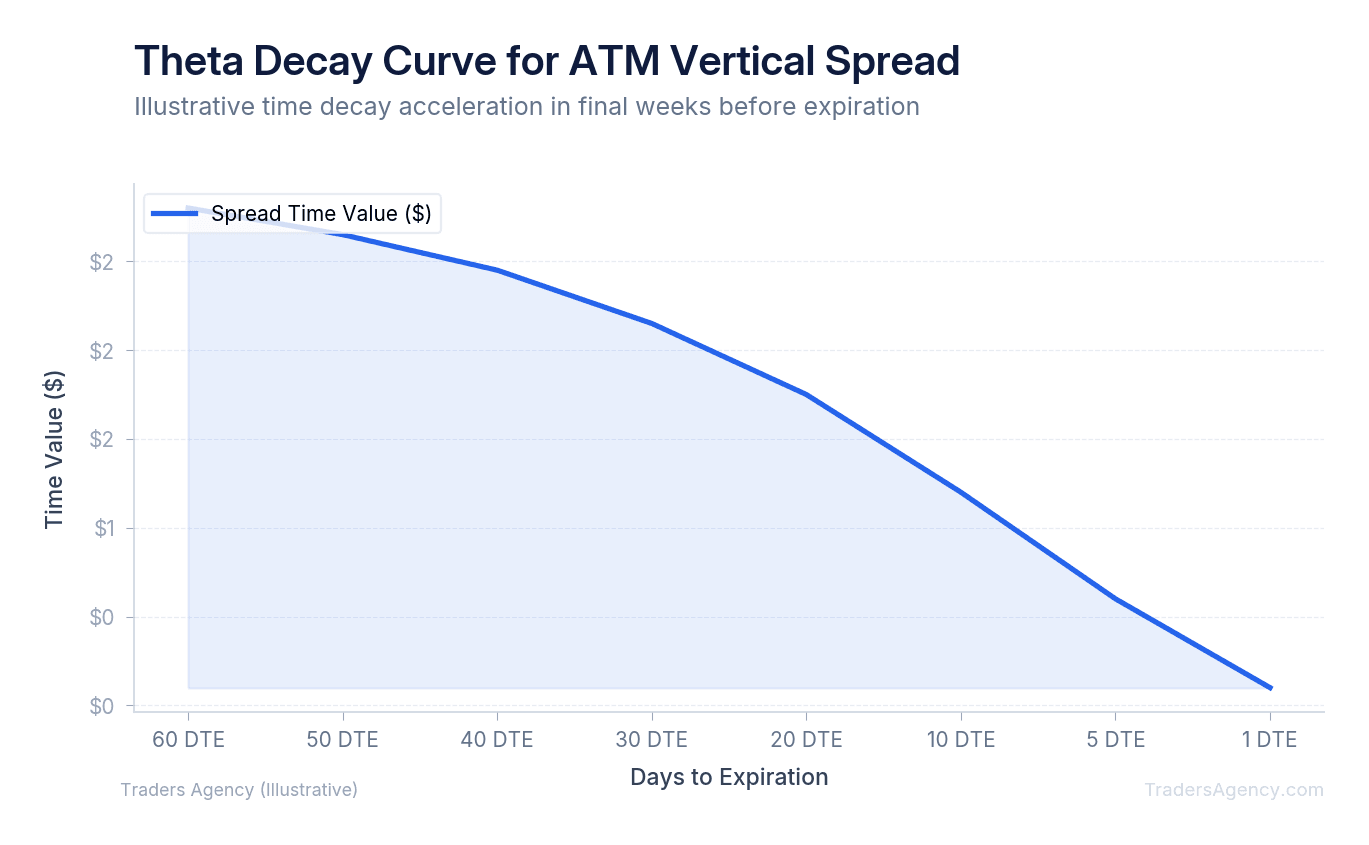

Options Greeks measure how different market forces impact your trade's price. Because a vertical spread involves buying and selling options simultaneously, the Greeks partially cancel each other out. This makes vertical spreads much less sensitive to time decay and volatility changes than single option positions.

Time decay (theta) negatively impacts option buyers. If you buy a standard call, time decay constantly eats away at your position. Every day that passes lowers the value of your option. In a vertical spread, the option you sold also loses value over time. For credit spreads, this works in your favor because you want both options to expire worthless, giving you net positive theta. For debit spreads, the short leg only partially offsets the negative theta from your long leg, so time decay still works against you, just less aggressively than with a single long option.

Volatility (vega) works in a similar way. A sudden drop in market volatility will crush the value of a single long call. In a vertical spread, the short call also loses value. This dual-action partially protects your overall position from severe volatility swings, making the trade easier to manage than a standalone option.

Key Concept: In a vertical spread, the Greeks from your long and short legs partially offset each other. This means your position is naturally more stable against time decay and volatility shifts compared to a single-leg option.

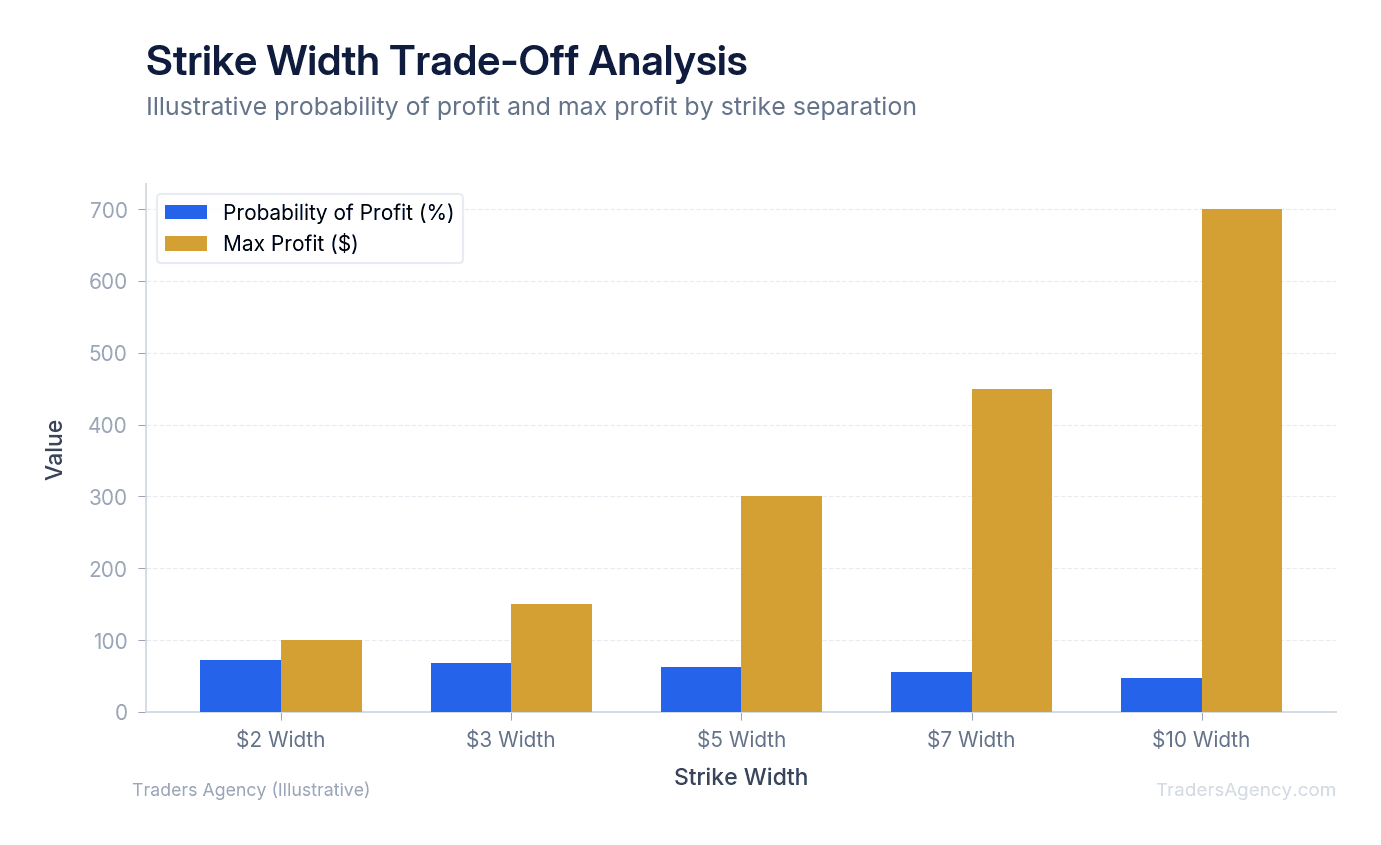

How Do You Choose the Right Strike Width for a Vertical Spread?

The distance between your bought and sold options is called the strike width. Our team recommends keeping strike widths narrow when you first start trading defined risk options. A narrow width keeps your capital requirements low while you learn the mechanics.

If you choose a $5 wide spread, your maximum risk and reward are confined to that $5 window. If you widen the spread to $10, your potential profit increases, but your initial cost and maximum risk also increase proportionally.

Wider spreads behave more like single options. They require a larger move in the underlying stock to reach maximum profit. Narrow spreads cost less upfront, which means you risk less capital per trade. This lower cost basis can make it easier to achieve a favorable risk-to-reward ratio on smaller moves.

| Strike Width | Approximate Cost | Max Profit Potential | Probability of Profit |

|---|---|---|---|

| $2.50 | $100 | $150 | Higher |

| $5.00 | $200 | $300 | Moderate |

| $10.00 | $400 | $600 | Lower |

We suggest starting with $1 to $5 wide spreads until you're completely comfortable with the execution process. As your confidence and account size grow, you can experiment with wider strikes.

Are Vertical Spreads Safe?

Vertical spreads are generally considered safer than naked options or single-leg options because they have a hard cap on potential losses. You know your exact maximum risk before you enter the trade. That said, they still carry the risk of losing your entire initial investment on that position.

We teach our members that safety in trading comes from proper risk management. While these are defined risk trades, you should never allocate your entire account to a single position. A capped loss is still a loss if the trade goes against you.

Our team prefers to risk no more than 2% to 5% of total account capital on any single vertical spread. If you have a $10,000 account, your maximum loss on a single trade should not exceed $200 to $500. This strict position sizing ensures that a string of losing trades won't wipe out your portfolio.

Watch Out: Avoid using vertical spreads in low-liquidity stocks. If the bid-ask spread is too wide, it becomes difficult to enter and exit at fair prices. Stick to highly traded, large-cap stocks or major index ETFs like SPY or QQQ when practicing these setups. High liquidity ensures you can close your position quickly if market conditions change.

You should also be aware of early assignment risk on the short leg of your spread. If the short option goes deep in the money before expiration, the buyer might exercise it early. While your long option protects you from catastrophic losses, early assignment can temporarily tie up your account capital. We recommend closing vertical spreads a few days before expiration to avoid this scenario completely.

Risk Reminder: Always close your vertical spreads 3 to 5 days before expiration to avoid early assignment complications. Even though your risk is defined, managing your exit timing keeps your account capital free and your trading plan on track.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyKey Takeaways

- A vertical spread requires two legs on the same underlying stock and expiration date, differing only by strike price. The premium collected from the short leg directly reduces your cost basis on the long leg.

- Vertical spreads are classified as defined risk options strategies because your maximum loss is locked in at entry. You cannot lose more than the net premium paid, regardless of how far the stock moves against you.

- Early assignment risk is real on the short leg if it goes deep in the money before expiration. Closing the spread 3 to 5 days before expiration eliminates this complication entirely.

- Selling the short leg acts as a financial shock absorber. Unlike buying a naked option where a full premium loss is possible on any adverse move, the spread structure caps your downside from the moment the trade is placed.

- Strike width selection directly controls both your maximum risk and your maximum reward. Wider strikes increase potential profit but also increase the capital you put at risk on each trade.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources