The Department of Labor just proposed a new rule, and you need to understand exactly what it means for your retirement. The proposal would open 401k private equity, cryptocurrency, and real estate investments to everyday retirement savers, and the risks are bigger than most people realize.

For decades, your 401(k) has been straightforward. Stocks, bonds, mutual funds. Liquid, regulated assets. Things you could actually sell and get your money out of when you needed it.

That is about to change.

The Trump administration just proposed opening retirement plans to a whole new world of alternative investments. Major financial firms have been eyeing the $7 trillion sitting in 401(k) accounts for a long time. The timing of this move is completely insane, and almost nobody is paying attention to the massive risks hiding just beneath the surface.

What Is the New 401k Private Equity Rule?

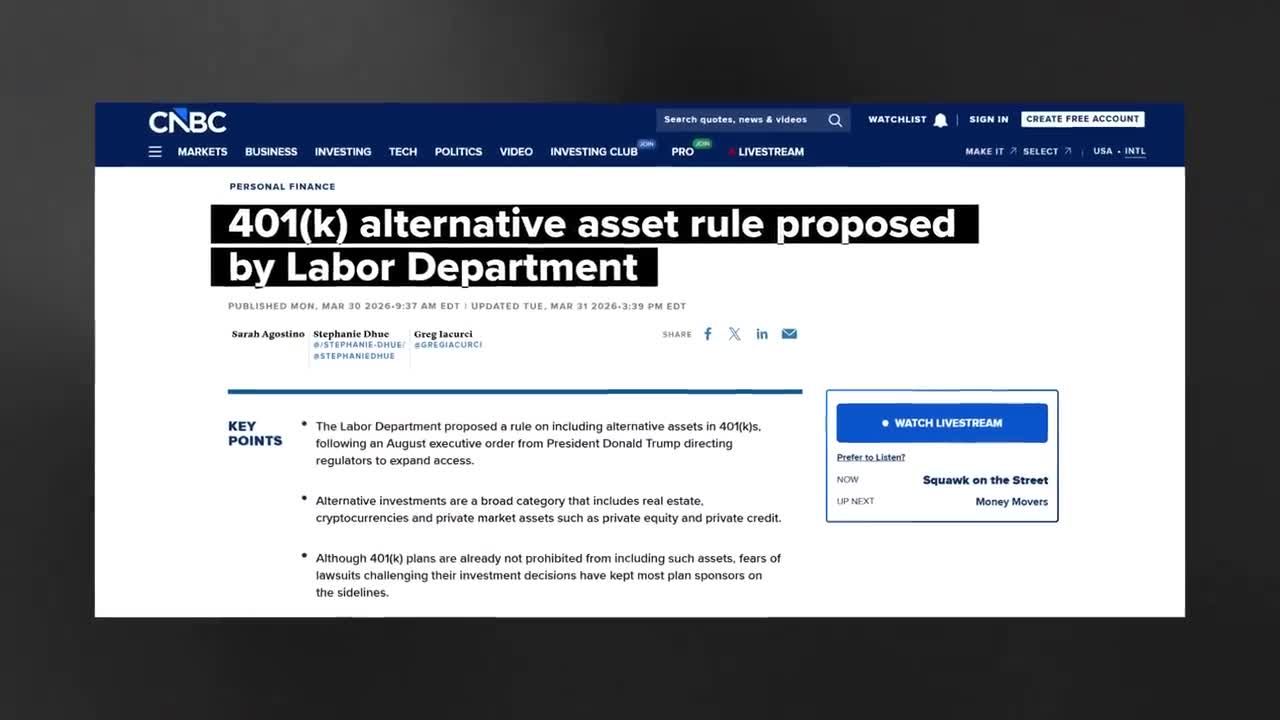

The Department of Labor proposal opens retirement plans to alternative investments. Private equity, cryptocurrencies, real estate, all buyable directly inside your standard 401(k).

The rule dropped on March 30th. They are selling this as freedom, and I actually agree with that. People should have more options. More diversification. The chance at better returns. I am a libertarian who believes in blanket freedom. We are all grown-ups who should be free to make our own decisions, even if they turn out to be bad ones.

But you need to look at who is actually pushing this rule.

The people behind it are not doing this for your benefit. Major financial firms have been pushing for this exact access for years. Blackstone, KKR, and Apollo Global have been eyeing that $7 trillion sitting in your 401(k) accounts for a very long time. They want that capital, and this new proposal would change everything.

Why Private Equity, Why Now?

Private equity is not like buying a stock. When you own stocks in your 401(k) and the market crashes, you can sell. You can move to cash. You can get out at any time, instantly.

Private equity does not work that way. These are illiquid investments. You cannot just sell whenever you want. You cannot just exit when things go wrong.

And right now, things are starting to go wrong.

The KKR Downgrade Nobody Covered

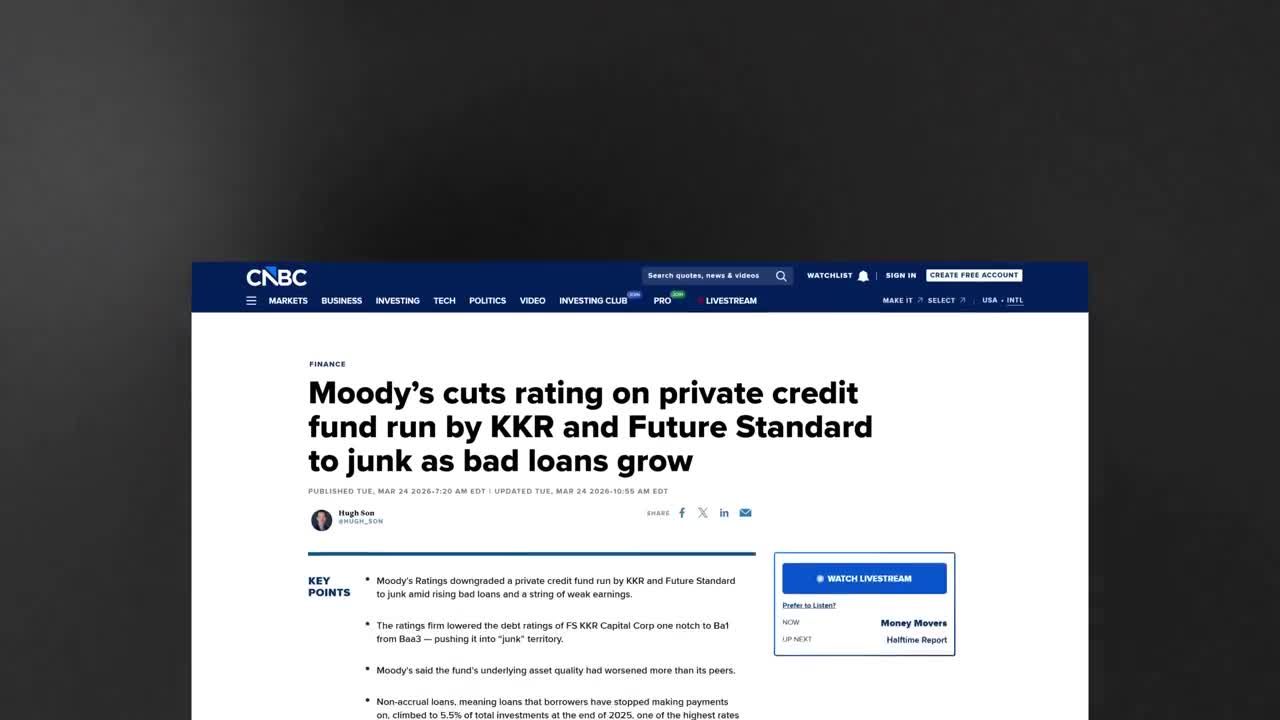

One week before this Department of Labor rule dropped, Moody's made a move that almost nobody covered.

Moody's downgraded a private credit fund run by KKR to junk. KKR is one of the largest private equity firms in the entire world. Their private credit fund is now sitting at junk status.

Why did this happen? Nonaccrual loans. That is the fancy financial term for loans where the borrowers have simply stopped making their payments.

This is happening inside a private credit market currently worth $1.8 trillion. The bad loans are piling up fast.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWhat Is the Illiquidity Trap in 401k Private Equity Investing?

Once your money is in private equity, it is locked up. This is the exact danger for the average, non-sophisticated investor.

When you own stocks and the market crashes, you sell. You move to cash. You protect yourself. Private equity strips that power away. You cannot exit when bad loans start piling up. You cannot sell when the fund gets downgraded to junk.

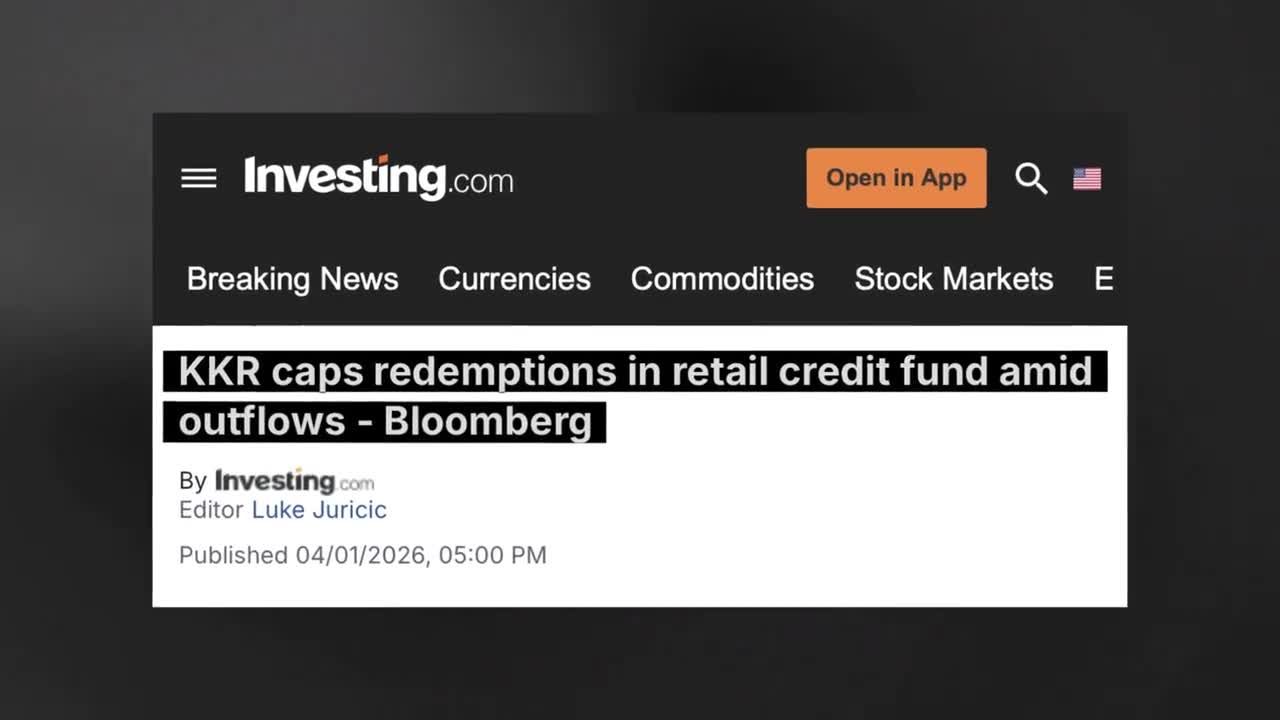

We are already seeing this play out in real time.

This is what happens when you buy illiquid, overly complex assets that even I do not fully understand. You lose the ability to protect yourself when the market turns against you.

The Suspicious Timeline

The timeline of these events should make every single investor pause.

A private credit fund run by one of the biggest private equity firms in the world gets downgraded to junk because borrowers are defaulting on their loans. Six days later, the government proposes a rule that will funnel billions of dollars from everyday retirement accounts directly into these exact types of private credit and equity markets.

That timeline tells me a lot. There is $7 trillion sitting in retirement accounts that these firms have not been able to get their hands on. This proposal would change that.

How Can You Protect Your 401k from Private Equity Risk?

The rule is still a proposal. It has not been finalized. Maybe it gets watered down, maybe it doesn't. But the direction is clear. If this becomes reality, you will have the power to get yourself into a lot of trouble. None of these alternative assets will show up in your account automatically. You will have to choose them.

Here is exactly what you need to do.

1. Know What Is in Your Plan

Pay attention to your account. If you start seeing 401k private equity or crypto options appearing in your menu, read the prospectus. Or at least feed it into ChatGPT and let a computer explain it to you in plain English. You must understand the liquidity terms. Know exactly when you can and cannot get your money out.

2. Question the Upside

Be very, very skeptical of anyone selling you on the upside without explaining the downside. Every investment has risk. If a fund manager or a brochure is only showing you massive potential returns without clearly defining the lock-up periods and default risks, walk away.

The Bottom Line

In all likelihood, the finance space will be a very different place five or ten years from now. We are moving toward a world of 24-hour stock trading, heavy crypto integration, and expanded private credit and equity markets. Personally, I am all for it.

But with every major financial shift comes a fresh batch of charlatans trying to separate you from your money.

This is not about whether you can handle the risk. This is about whether you actually know the risk you are taking. Private equity can be a great asset class. It has made more billionaires than almost anything else. It is a fantastic opportunity for the right investor.

But by stuffing these assets into retirement plans with mandatory holding periods and often no exit mechanism, people are going to get hurt. Some people are going to get themselves in deep trouble, just like they did with meme stocks, little crypto coins, NFTs, digital real estate, and the now non-existent metaverse.

Others will become very, very rich.

Be careful, and never invest in something you do not understand.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- The Department of Labor proposed a rule on March 30th that would open standard 401(k) plans to private equity, cryptocurrency, and real estate investments for everyday retirement savers.

- Roughly $7 trillion sits in 401(k) accounts, and major financial firms have been positioning to access that capital through expanded alternative investment rules.

- The core danger is illiquidity: private equity and real estate inside retirement plans often come with mandatory holding periods and no exit mechanism, meaning savers cannot get their money out when they need it.

- The rule is framed as expanding investor freedom, but the same behavioral patterns that burned retail investors in meme stocks, NFTs, and the metaverse are likely to repeat in an unguarded alternative-asset environment.

- Private equity has created more billionaires than almost any other asset class, making it genuinely valuable for the right investor, but that investor needs to fully understand the structure before committing retirement savings.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources