You've probably seen this play out in real time. The Consumer Price Index prints a hot number, and immediately, financial commentators start yelling about buying gold. But does the precious metals inflation hedge actually work? We'll walk you through the real mechanics of trading metals during inflationary environments, show you why gold sometimes fails to protect your portfolio, teach you how to track real interest rates, and demonstrate exactly how to size these positions like a professional trader.

What Is a Precious Metals Inflation Hedge?

Bottom Line: The precious metals inflation hedge is real, but it is conditional. Gold performs when real interest rates are negative and monetary policy is loose, not simply whenever CPI runs hot. Traders who understand this distinction, size positions carefully, and track real rates will use gold far more effectively than those who treat it as a reflexive inflation buy.

A precious metals inflation hedge operates on a straightforward premise. Fiat currency loses value over time as governments print more money. Hard assets like gold and silver require physical labor and capital to extract from the earth, so their price naturally adjusts upward to reflect the declining purchasing power of the dollar.

Think of this strategy like a financial shock absorber. Gold and silver don't generate quarterly dividends or earnings reports. They simply absorb the impact of a devaluing currency.

Key Concept: Our team teaches traders to view precious metals not as growth assets, but as alternate currencies. When the primary currency system experiences rapid inflation, capital naturally flows into these alternate, finite currencies.

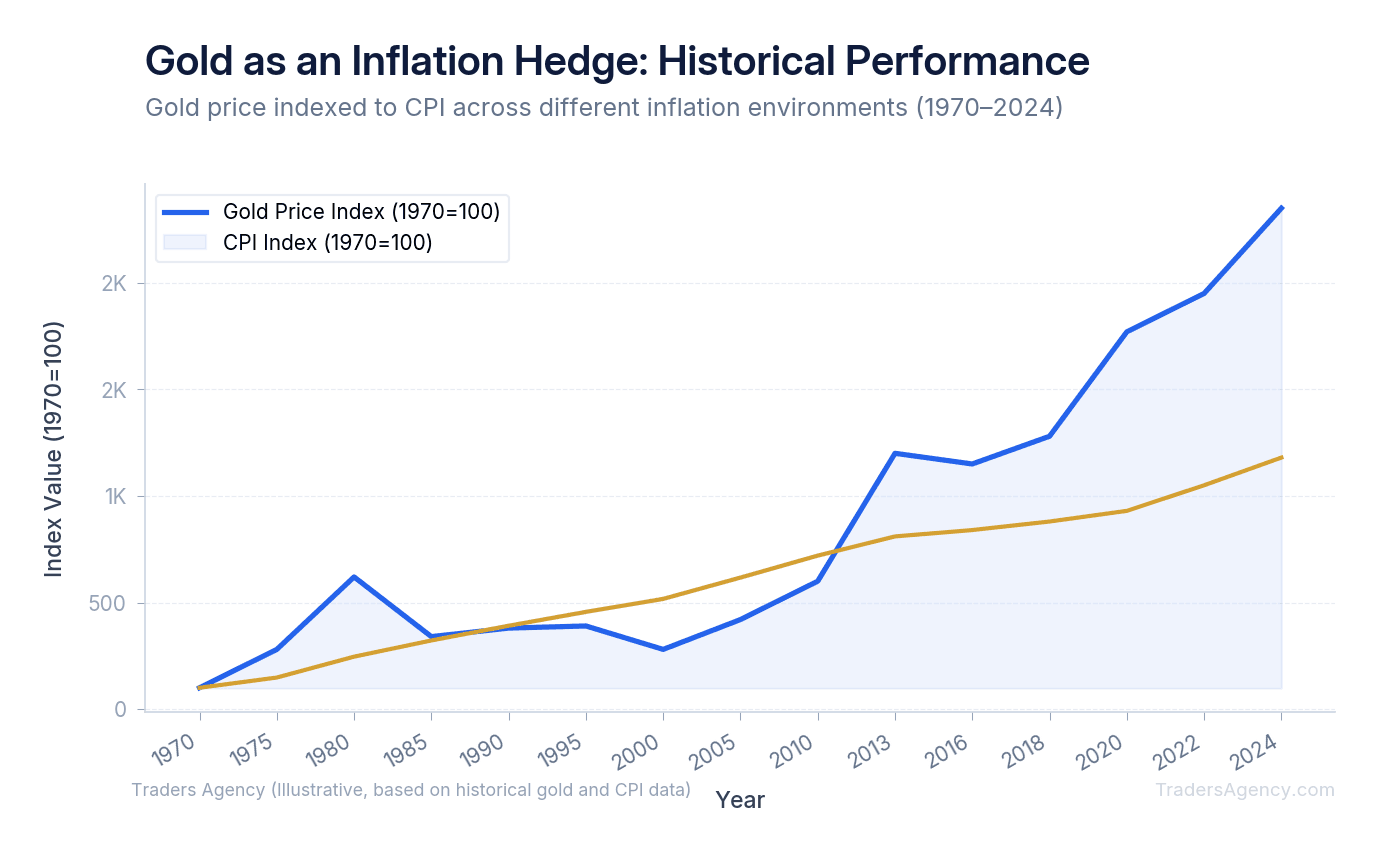

How Has Gold Actually Performed During High Inflation Periods?

Gold has historically performed exceptionally well during sustained high inflation periods like the 1970s and early 2020s, but it can underperform when inflation is moderate or falling. The effectiveness of gold as an inflation hedge depends heavily on whether central banks raise interest rates faster than consumer prices rise.

During the 1970s, inflation ran out of control. Gold responded by rocketing from $35 per ounce to over $800 per ounce by 1980. This is the textbook example that most financial advisors cite.

However, the relationship is not always perfect. Between 2013 and 2018, gold experienced a prolonged bear market. Inflation remained relatively low, and the Federal Reserve began tapering its quantitative easing programs. During this window, holding gold actually resulted in negative real returns for investors.

The early 2020s brought a return to the classic model. As inflation spiked to 9.1% in 2022, gold eventually broke out to new all-time highs above $2,000 per ounce.

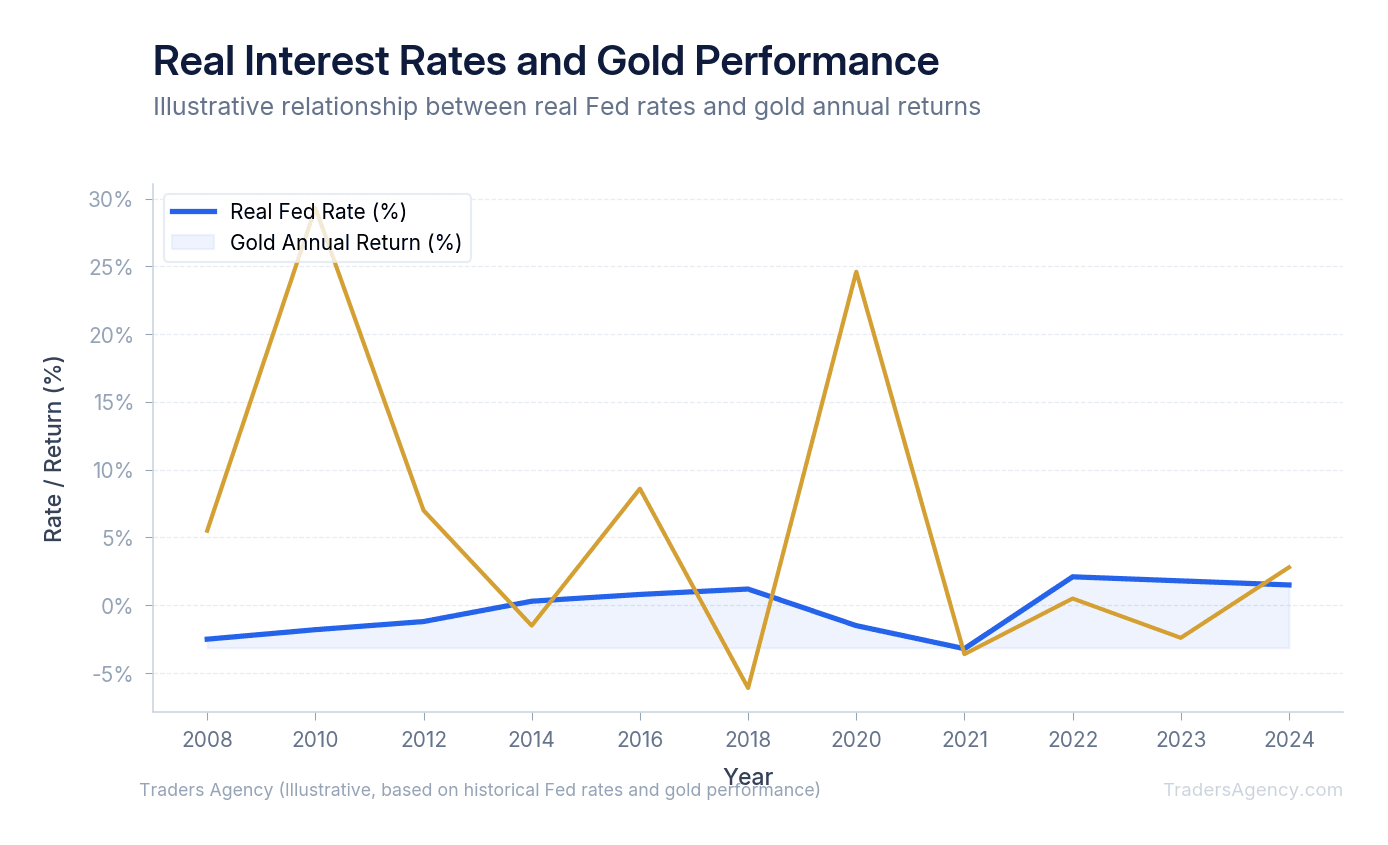

Why Do Real Interest Rates Matter More Than Inflation for Gold?

Real interest rates drive gold prices much more reliably than headline inflation alone. A real interest rate is the nominal yield on a bond minus the current inflation rate. When real rates turn negative, gold becomes highly attractive because holding cash or bonds guarantees a loss of purchasing power.

Here's the exact math our team uses. If a 10-year Treasury yields 4% and the inflation rate is 6%, your real interest rate is negative 2%.

In a negative real rate environment, investors lose money by holding safe government bonds. Gold pays zero percent interest, but zero is mathematically better than negative two. This dynamic forces institutional capital out of bonds and into precious metals.

Conversely, if the 10-year Treasury yields 5% and inflation drops to 2%, the real rate is positive 3%. In this scenario, gold usually sells off because investors can earn a guaranteed positive return in bonds.

Key Concept: The formula is simple: Real Interest Rate = Bond Yield minus Inflation Rate. When this number is negative, gold rallies. When it's positive, gold struggles. Track this number before every precious metals trade.

When Does the Gold-Inflation Relationship Break Down?

The gold-inflation relationship breaks down when central banks aggressively hike interest rates to fight rising prices. If the Federal Reserve raises rates to 5% while inflation is at 4%, the real interest rate becomes positive 1%. This positive yield draws capital away from non-yielding precious metals and into bonds.

We see traders make this mistake constantly. They see a high Consumer Price Index (CPI) print and immediately buy gold. They ignore what the Federal Reserve is doing in response.

In 1980, Federal Reserve Chairman Paul Volcker raised the federal funds rate to 20% to crush inflation. Gold crashed shortly after. The inflation was still high, but the interest rates were even higher.

Watch Out: A hot inflation print alone is NOT a buy signal for gold. You must track the bond market. If bond yields are rising faster than inflation, gold will struggle to gain traction regardless of how high CPI prints.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

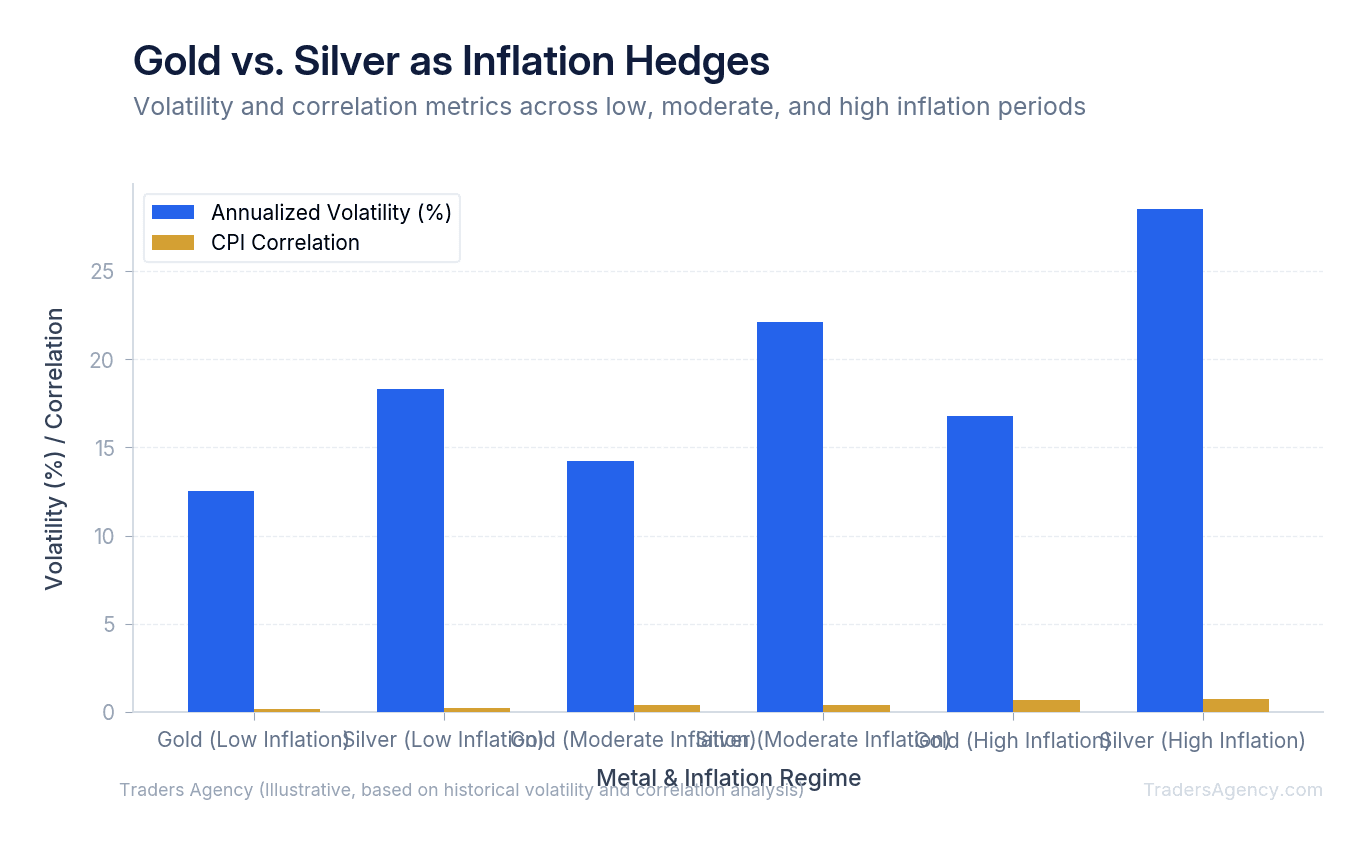

Join Traders AgencySilver vs. Gold: Which Precious Metal Hedges Better?

Silver acts as a higher-beta version of gold during inflationary periods, meaning it moves faster in both directions. While gold is a pure monetary asset, silver has heavy industrial demand that makes it more sensitive to economic growth. Silver often outperforms gold late in an inflationary cycle.

Our team prefers to trade gold for stability and silver for aggressive upside. Because the silver market is much smaller than the gold market, it takes less capital to move the price.

| Characteristic | Gold | Silver |

|---|---|---|

| Primary Role | Monetary asset, store of value | Industrial + monetary hybrid |

| Volatility | Lower | Higher (1.5x to 2x gold) |

| Best Phase | Early inflation cycle | Late inflation cycle |

| Preferred ETF | GLD or IAU | SLV |

| Stop Loss Width | Standard | Wider (to survive volatility) |

When inflation fears peak, silver can easily double the percentage returns of gold. However, when the inflation trade unwinds, silver will crash much harder. If you trade SLV (iShares Silver Trust), you must use wider stop losses to survive the natural volatility.

Are TIPS a Better Inflation Hedge Than Precious Metals?

Treasury Inflation-Protected Securities (TIPS) offer a mathematically guaranteed inflation hedge, whereas precious metals rely on market sentiment and supply dynamics. TIPS directly adjust their principal value based on the Consumer Price Index, making them a more predictable, lower-risk tool for protecting purchasing power compared to volatile commodity markets.

The principal value of TIPS rises with inflation and drops with deflation. When the bond matures, you receive either the adjusted principal or the original principal, whichever is greater.

We view TIPS and gold as complementary tools rather than direct competitors. TIPS are for capital preservation. Precious metals are for capital appreciation during periods of monetary instability.

Should You Use ETFs or Physical Gold for Inflation Exposure?

Exchange-traded funds provide the most efficient way for active traders to gain precious metals exposure, offering high liquidity and tight bid-ask spreads. Physical gold offers protection against systemic financial risks but carries high dealer markups, storage costs, and insurance fees that drag down your overall investment returns.

For active trading, we strictly use ETFs. The SPDR Gold Shares (GLD) and the iShares Gold Trust (IAU) are our preferred vehicles. They allow you to enter and exit positions instantly during normal market hours.

Physical gold coins (like American Eagles) often carry premiums of 5% to 10% over the spot price of gold. If you buy at a 10% premium and sell back near spot, the price must rise by at least that amount just for you to break even. Keep physical metals for long-term emergency holding, not for active inflation trading.

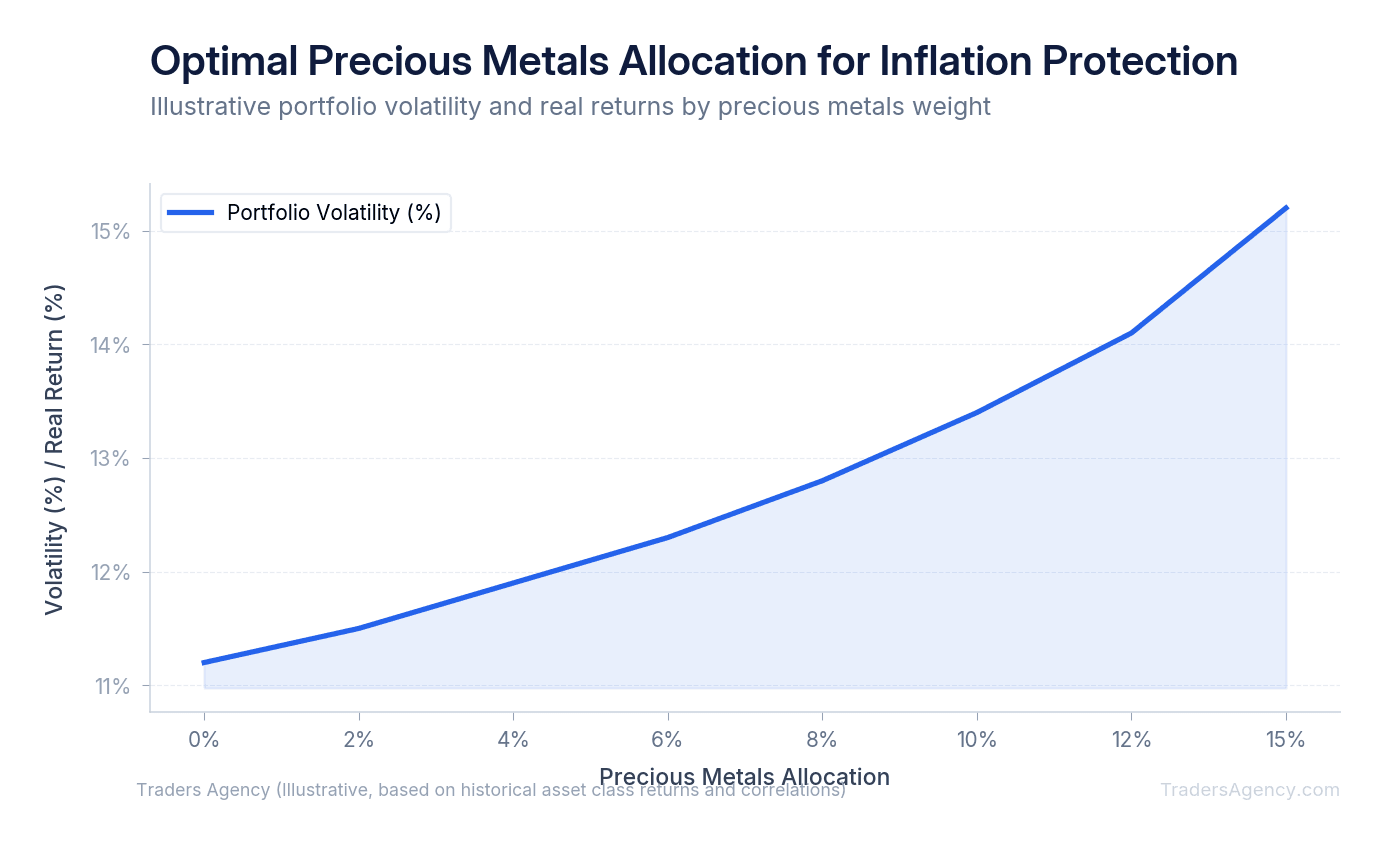

How Much Precious Metals Should You Hold in an Inflation-Protected Portfolio?

Our team recommends allocating between 5% and 10% of your total portfolio to precious metals for effective inflation protection. Allocating less than 5% provides insufficient hedging benefits, while allocating more than 15% introduces excessive volatility and creates a drag on long-term portfolio growth due to the lack of yield.

Here's how we structure this allocation:

- Assess your core portfolio: Calculate your total exposure to standard stocks and bonds.

- Target a 5% to 10% allocation: Move capital from your bond allocation into liquid gold ETFs like GLD or IAU.

- Rebalance annually: When inflation spikes and gold rallies, your allocation might grow to 12% or 15%. Sell the excess metals to lock in profits and buy back into your stock positions.

Step-by-Step: Setting Up Your Precious Metals Inflation Hedge Trade

Let's walk through a concrete trading scenario so you can see exactly how to execute a precious metals inflation hedge in a live account.

- Identify the Setup: Check the latest inflation data and confirm CPI is rising at 5% year-over-year. Next, check the 10-year Treasury yield and note it sitting at 3%. Subtract the inflation rate from the bond yield (3% minus 5%). The real interest rate is negative 2%. This negative real yield is your green light. The macroeconomic conditions are perfectly aligned for gold to rally.

- Execute the Trade: Initiate a position using the GLD ETF at a market price of $190 per share. Purchase 100 shares, deploying $19,000 in total capital. Place a hard stop loss at $175. This means you're risking exactly $1,500 on the trade (100 shares multiplied by the $15 difference between your entry and your stop).

- Manage the Position: Monitor real interest rates weekly. If the Fed signals aggressive hikes, tighten your stop. If real rates continue falling, hold your position and let the trade work toward your profit target of $220.

| Parameter | Value |

|---|---|

| Instrument | GLD ETF |

| Entry Price | $190 per share |

| Position Size | 100 shares ($19,000) |

| Stop Loss | $175 |

| Risk Per Trade | $1,500 |

| Profit Target | $220 |

| Potential Reward | $3,000 |

Trade Outcome Scenarios

| Scenario | What Happens | GLD Price | Result |

|---|---|---|---|

| Best Case | Inflation stays stubborn, Fed holds rates. Real rates plunge further negative. | $220 | +$3,000 profit |

| Most Likely | Inflation persists longer than expected. GLD grinds higher over six months. | $205 | +$1,500 profit |

| Worst Case | Fed surprises with massive rate hike. Bond yields spike, real rates turn positive. | $175 | -$1,500 loss (controlled) |

Risk Warning: Trading precious metals requires patience and strict adherence to the data. Watch the real interest rates, manage your position sizes, and always respect your stop losses. A single unexpected Fed decision can reverse the entire inflation trade within days.

The key takeaway here: gold is not a "buy and forget" inflation hedge. It's a conditional trade that works best when real interest rates are negative and the Fed is behind the curve. Understanding how to properly implement a precious metals inflation hedge means tracking the data, sizing your positions conservatively, and letting the macroeconomic environment do the heavy lifting for you.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyKey Takeaways

- Gold works best as an inflation hedge when real interest rates are negative, meaning the Fed is effectively behind the curve on inflation. When real rates turn positive, the trade often breaks down.

- Gold is not a passive 'buy and hold' inflation hedge. It is a conditional, macro-driven trade that requires active monitoring of CPI prints, Fed policy signals, and real rate movements.

- The 1970s and early 2020s are the clearest historical examples of gold outperforming during sustained high inflation, but performance is inconsistent outside those specific macro conditions.

- Professional traders size precious metals positions conservatively and use stop losses because a single unexpected Fed decision can reverse the entire inflation trade within days.

- Gold and silver should be treated as alternate currencies, not growth assets. Their value proposition is absorbing the impact of a devaluing fiat currency, not generating yield or earnings.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources