Understanding theta decay options strategies is a foundational skill for consistent trading. Theta decay measures how much an option's price decreases each day due to the passage of time. We're going to walk you through exactly how time value works and how to use it to your advantage.

You've probably seen this frustrating scenario play out in your own account. You buy a call option, the underlying stock goes up, but your position still loses money. This happens because the time value of the contract eroded faster than the stock price increased.

By the end of this guide, you'll know the exact days to expiration (DTE) sweet spots our team targets. We'll also show you how to structure specific trades to profit from the passage of time.

What Is Theta Decay in Options Trading?

Bottom Line: Theta decay is not just a background force to be aware of; it is a tradeable edge when you understand which structures capture it most efficiently and which DTE windows offer the best risk-to-reward. The real skill is pairing a mechanical exit plan with the right trade structure so that a single losing position cannot erase weeks of steady premium collection. Traders who internalize both the opportunity and the risk controls around theta are far better positioned for consistency than those chasing directional plays.

Theta decay in options trading represents the daily reduction in an option's extrinsic value as it moves closer to its expiration date. This metric tells you exactly how much money the option contract will lose each day, assuming the underlying stock price and implied volatility remain completely unchanged.

Think of theta like a melting ice cube sitting on your kitchen counter. The moment you pull that ice cube out of the freezer, it begins to melt. Options contracts operate the exact same way. Every single day that passes chips away at the premium of the contract.

Key Concept: Theta is one of the primary risk metrics (known as "the Greeks") used to evaluate options pricing. It quantifies the daily cost of holding an option position. If you buy an option, you pay that fee every day. If you sell an option, you collect that fee directly into your account.

Our team prefers to view theta as a daily rental fee. Buyers pay rent on their position every single day they hold it. Sellers collect that rent. Once you internalize this concept, your entire approach to options trading shifts.

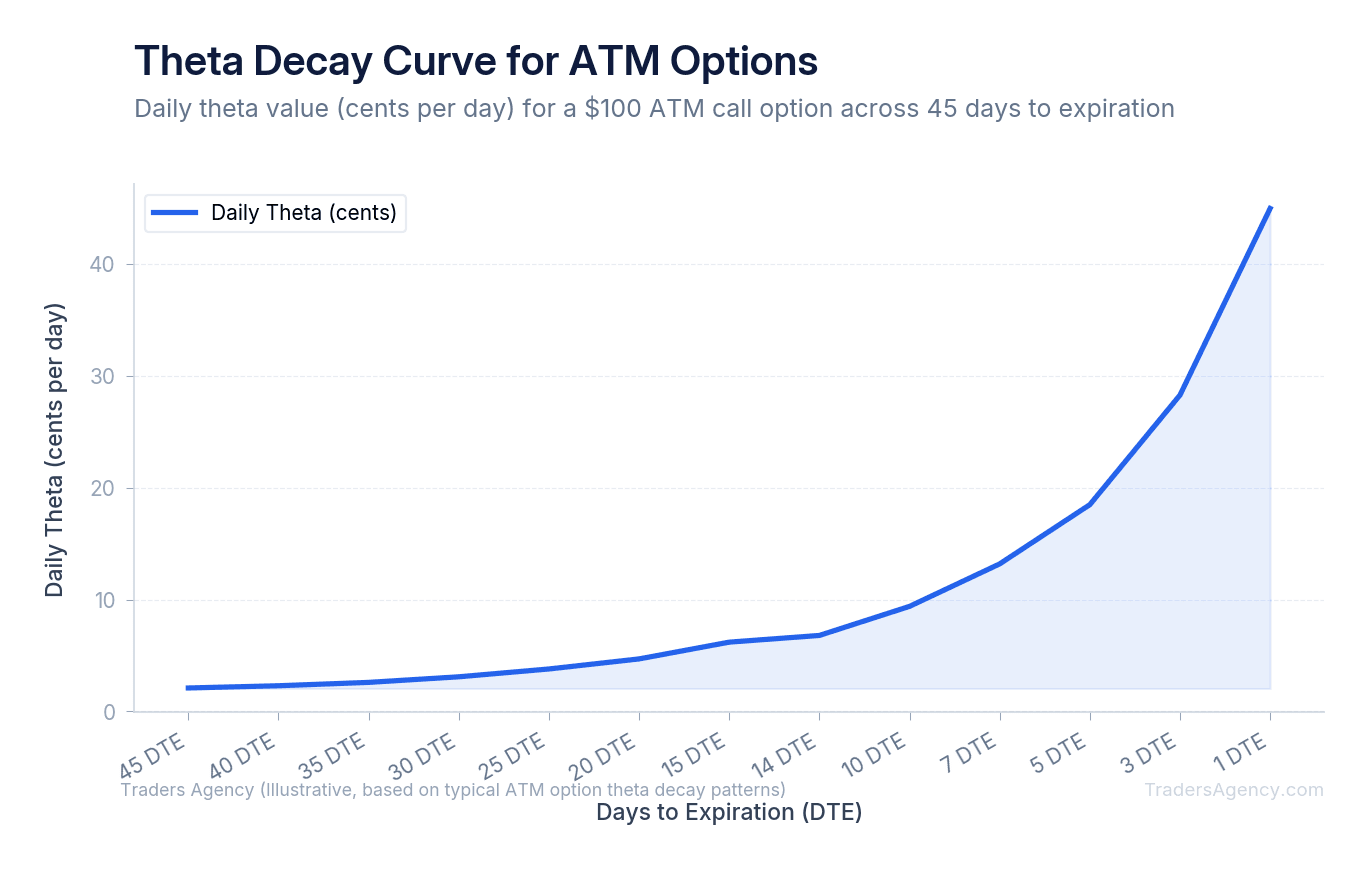

How Does the Theta Decay Curve Accelerate as Expiration Approaches?

The theta decay curve accelerates exponentially rather than linearly as expiration approaches. An option loses a very small amount of value each day when it is months away from expiration. However, as the contract enters the final 30 to 45 days, the daily rate of value loss increases dramatically.

When you buy a contract with 120 DTE, the daily time decay is barely noticeable. The market still prices in plenty of time for the stock to make a significant directional move.

Once that same contract crosses the 45 DTE mark, the melting process speeds up significantly. By the time the contract reaches 14 DTE, the daily loss of extrinsic value becomes highly aggressive.

We teach our members to respect this mathematical curve. Holding long options into the final two weeks of expiration is a common way to drain your trading account. The math simply works against you as the daily decay rate peaks.

If an option has a theta of -0.10, the contract loses $10 of value per day. In the final week before expiration, that number might jump to -0.30 or higher.

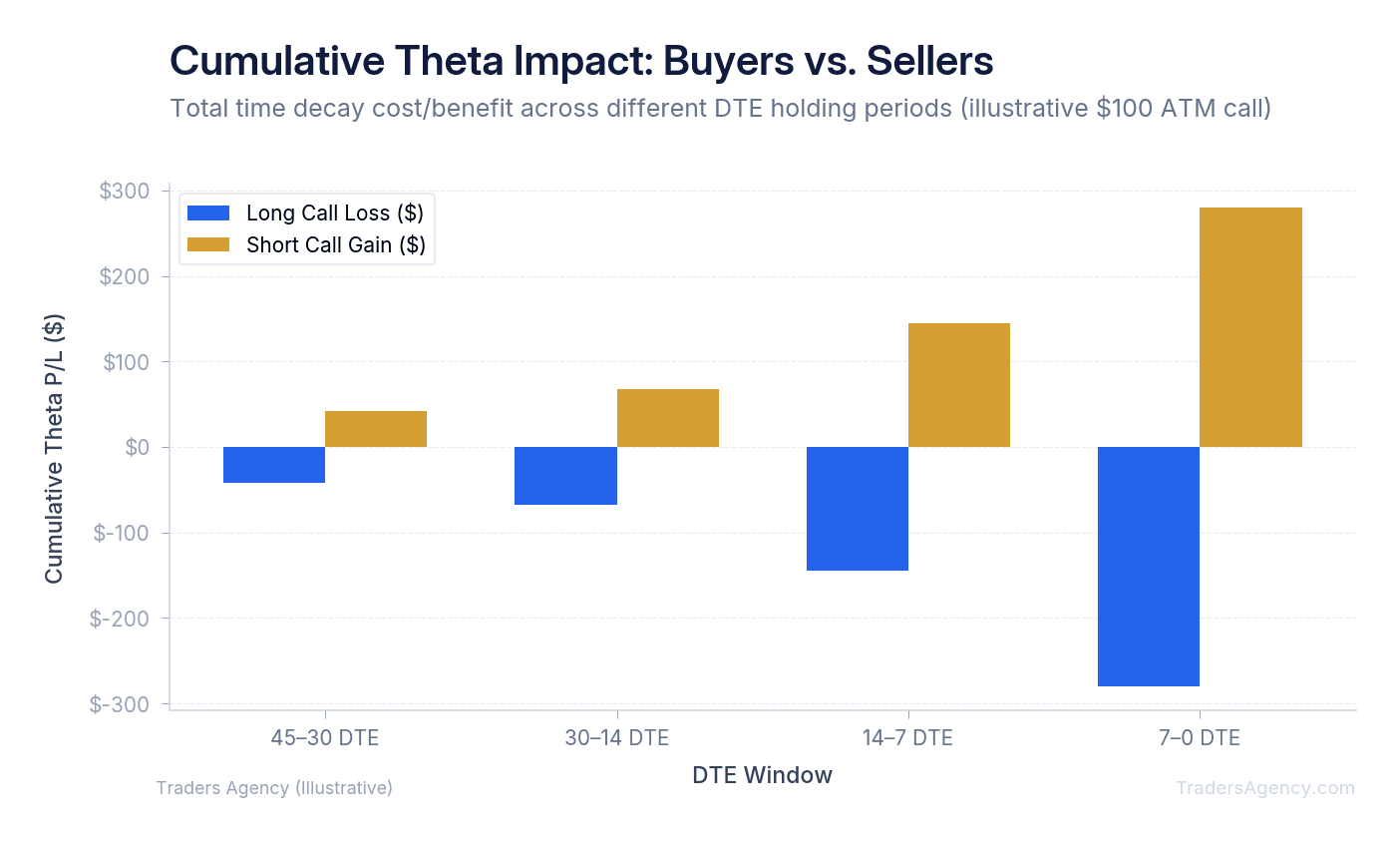

Who Actually Wins Between Options Buyers and Sellers When Theta Is Involved?

Option sellers win the time war because they collect premium upfront and benefit as theta decay erodes the option's value daily. Option buyers constantly fight against time, needing the underlying stock to move far enough and fast enough to overcome the daily loss of extrinsic value.

When you are a net buyer of options, theta is a negative number in your portfolio. You are racing against the clock. The stock must make a directional move just to offset the daily time decay.

When you are a net seller, theta is a positive number. You want the contract to lose value so you can buy it back cheaper or let it expire worthless.

Our education team recommends that intermediate traders learn to operate on the sell side. Selling premium puts the mathematical certainty of time decay in your favor. You don't need the stock to make a massive move to secure a profit.

Instead, you simply need the stock to stay within a specific range. As long as the stock cooperates, time decay does the heavy lifting for your portfolio.

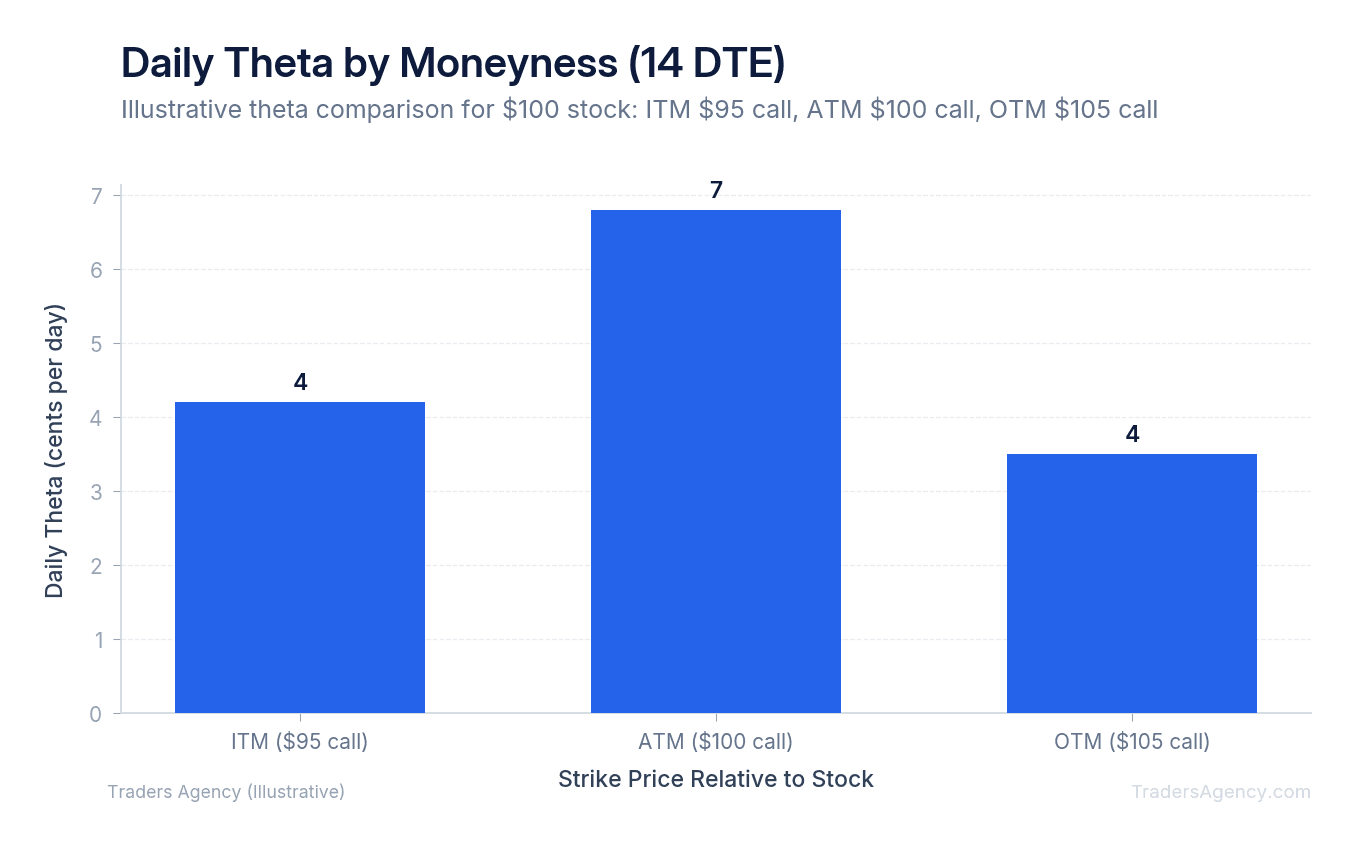

Why Do ATM Options Lose Value Fastest?

At-the-money (ATM) options lose value fastest because they contain the highest amount of extrinsic value. Since the strike price is exactly where the stock is currently trading, the market prices in maximum uncertainty. This high extrinsic value means there is more premium available to decay rapidly.

To understand how strike prices impact time decay, here's how the three main categories of options compare:

- At-the-money (ATM) options sit right at the current stock price. They hold the highest time value and experience the most aggressive daily decay.

- In-the-money (ITM) options consist mostly of intrinsic value. Because intrinsic value does not decay, these options have significantly lower theta.

- Out-of-the-money (OTM) options have only extrinsic value, but they are cheap. The market knows the probability of these options paying out is low, so the absolute theta decay is smaller.

If you want to maximize the premium you collect from time decay, selling ATM or slightly OTM strikes yields the highest daily return.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

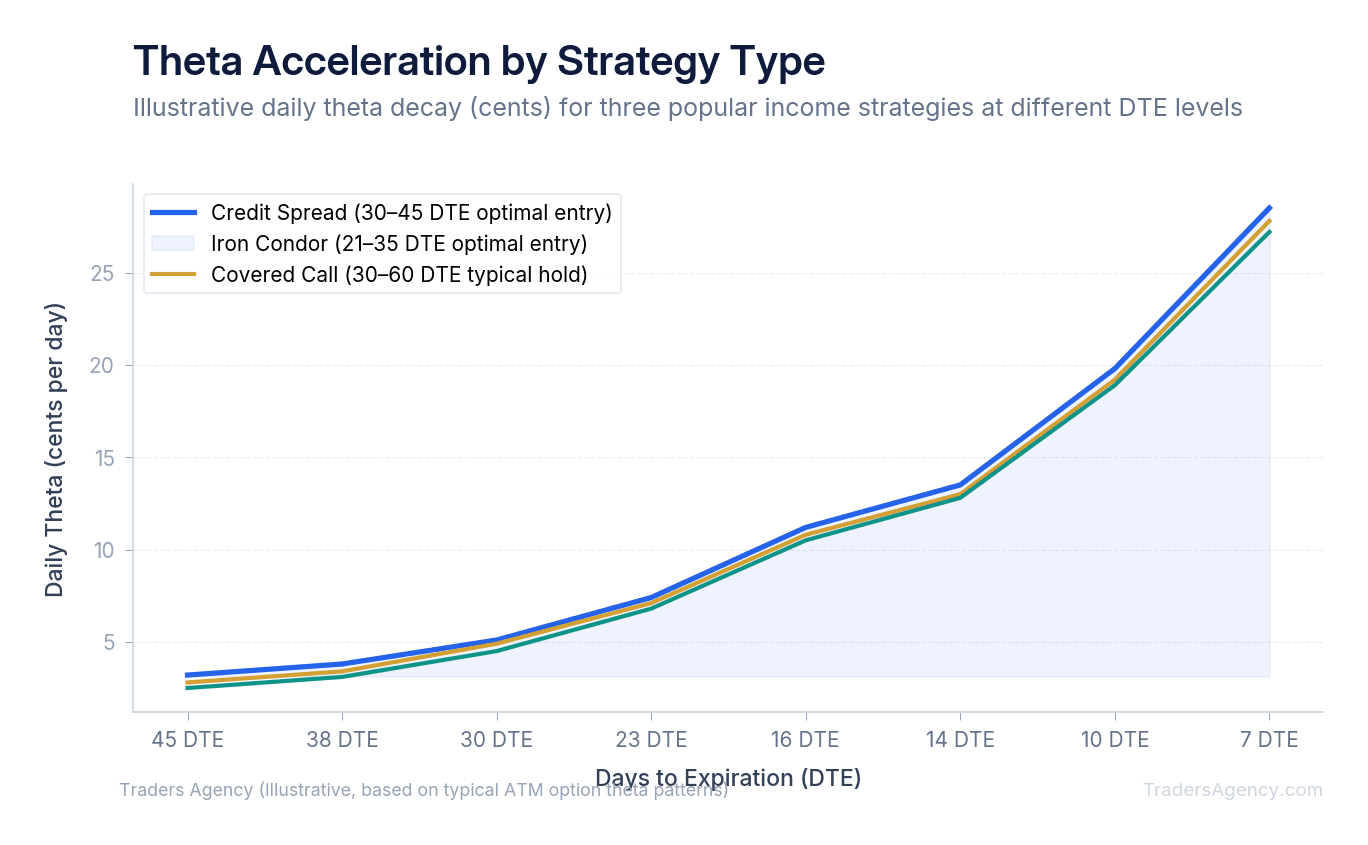

Join Traders AgencyDTE Sweet Spots for Credit Spreads, Iron Condors, and Covered Calls

Our team recommends entering short premium trades between 30 and 45 DTE. This specific window provides the perfect balance between rapid time decay and manageable price risk.

If you sell options with 90 DTE, you tie up your capital for months while waiting for the slow decay to take effect. If you sell options with 7 DTE, you collect very little premium and face massive risk if the stock makes a sudden move.

For credit spreads and iron condors, the 45 DTE entry allows you to capture the steepest part of the decay curve. We prefer to exit these trades around 14 to 21 DTE.

Closing the position early prevents you from holding through the final weeks. Price swings in the final days can easily wipe out your accumulated profits. You do not need to hold a trade to expiration to make money.

For covered calls, we often look at slightly shorter timeframes. Selling covered calls in the 30 DTE window allows you to generate consistent monthly income while taking advantage of the accelerated decay curve.

Key Concept: The 30 to 45 DTE window is our preferred entry zone for premium-selling strategies. It captures the steepest portion of the theta decay curve while giving you enough time to manage the trade if the stock moves against you.

Step-by-Step Example: Selling a Credit Spread to Capture Theta

Here's exactly how to set up a bull put spread to profit from time decay. Assume a major index ETF (ticker: SPY) is currently trading at $500 per share.

You believe SPY will stay above $490 over the next month. You decide to sell a credit spread to capture the theta decay while strictly defining your risk.

- Identify the Setup: Look for an expiration cycle roughly 45 DTE. You'll sell the $490 put option and simultaneously buy the $480 put option in the exact same expiration cycle.

- Execute the Trade: The $490 put pays you $3.50 in premium. The $480 put costs you $1.50 in premium. Your net credit is $2.00 per share, or $200 total per contract. By buying the $480 put, you cap your downside risk. Your broker will require $1,000 in collateral (the $10 difference between strikes multiplied by 100 shares).

- Manage the Position: As each day passes, theta eats away at the value of the $490 put you sold. If the ETF just trades sideways at $500, you'll see your position become profitable simply because time has passed. We recommend targeting an exit when you've captured 50% to 75% of the maximum credit.

| Parameter | Value |

|---|---|

| Underlying | SPY at $500 |

| Put Sold | $490 strike, $3.50 premium received |

| Put Bought | $480 strike, $1.50 premium paid |

| Net Credit | $2.00/share ($200 total) |

| Maximum Gain | $200 (if SPY stays above $490) |

| Maximum Loss | $800 ($1,000 spread width minus $200 credit) |

| Breakeven | $488 at expiration |

| Collateral Required | $1,000 |

How Do You Structure Theta Trades Without Getting Crushed by Vega Risk?

You cannot trade theta decay options without understanding vega. Vega measures how much an option's price changes based on a one-percentage-point shift in implied volatility.

If you sell a credit spread to collect theta, but implied volatility spikes, the options will increase in value. This volatility expansion will temporarily offset your time decay profits, putting your trade in the red.

Our team prefers to sell premium when implied volatility is already elevated. When implied volatility is high, options premiums are heavily inflated. As volatility returns to normal levels, you benefit from volatility crush. The options lose value from both the passage of time (theta) and the drop in volatility (vega). This is a powerful one-two punch that accelerates your profits.

You can check current implied volatility levels using tools available on the Cboe Options Exchange, which publishes the VIX and other volatility metrics in real time.

Watch Out: Never sell options right before a major earnings announcement just to capture theta. The massive volatility crush after earnings is heavily priced in, and the directional risk is entirely too high for a standard time decay strategy. One surprise move can wipe out months of steady premium collection.

What Are the Most Common Theta Trading Mistakes and How Do You Avoid Them?

Many intermediate traders understand the concept of time value but fail in the execution. Here's what we teach our members to avoid when trading theta strategies.

1. Holding Trades Until Expiration

Do not hold short option positions into expiration week. As expiration approaches, gamma risk increases significantly. Gamma measures the rate of change in delta, meaning a tiny move in the stock price can cause massive swings in the option's value. We prefer to close or roll positions at 21 DTE to avoid this late-stage volatility.

2. Ignoring Position Sizing

Selling options requires strict risk management because the maximum loss is often larger than the premium collected. Never allocate more than 2% to 5% of your total account capital to a single credit spread. A string of bad trades can quickly deplete your account if your position sizes are too large. Keeping your trades small ensures you can survive the inevitable losing streaks.

3. Trading Illiquid Options

When searching for the best theta decay options setups, always check the bid-ask spread before placing a trade. High premiums on obscure stocks usually mean high risk and terrible liquidity. If you enter an illiquid options chain, you'll lose a significant portion of your profits just crossing the spread to exit the trade. Stick to highly liquid stocks and major ETFs where you can easily enter and exit positions.

4. Forgetting Stop Losses

Always define your risk before entering the trade. We typically recommend closing a short premium trade if the loss reaches 200% of the premium received. Do not let a single bad trade wipe out a month of steady theta collection. Having a mechanical exit plan removes the emotion from your trading decisions.

Risk Warning: Options trading involves substantial risk and is not appropriate for every investor. The strategies discussed in this guide can result in the loss of your entire invested capital. Always trade with defined risk and never risk more than you can afford to lose.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyKey Takeaways

- Theta decay accelerates as expiration approaches, which is why options sellers target specific DTE windows rather than holding contracts indefinitely.

- Buying a call on a rising stock can still lose money if time value erodes faster than the underlying price increases, a dynamic that catches most new traders off guard.

- The article recommends closing a short premium trade if the loss reaches 200% of the premium received, creating a mechanical exit rule that removes emotion from the decision.

- Vega risk can overwhelm theta gains if implied volatility expands sharply, meaning trade structure must account for both time decay and volatility exposure simultaneously.

- Credit spreads, iron condors, and covered calls each have distinct DTE sweet spots that the team targets to maximize theta collection while managing assignment and directional risk.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources