IV crush after earnings is the rapid decline in an option's implied volatility immediately following a corporate earnings announcement. You've probably seen this happen in your own account. You buy a call option right before a highly anticipated earnings report. The company beats estimates, the stock jumps 5%, but when the market opens, your call option is somehow down 40%. We're going to walk you through exactly why this frustrating phenomenon happens and, more importantly, show you how professional traders use it to their advantage.

Many retail traders treat earnings season like a casino, hoping for a massive directional move. Our team prefers a more calculated approach based on market mechanics. By the end of this guide, you'll understand the math behind implied volatility around binary events, learn specific options selling strategies to protect your capital, and see exactly how we set up, execute, and manage these trades to capitalize on collapsing premiums.

What Is IV Crush and Why Does It Happen After Earnings?

Bottom Line: IV crush after earnings is not a bug in the system, it is a predictable, repeatable mechanic that favors options sellers over options buyers. Traders who understand this shift from trying to guess the directional move to collecting inflated premiums before the event resolves. The edge comes from putting probability on your side, not from being right about where the stock goes.

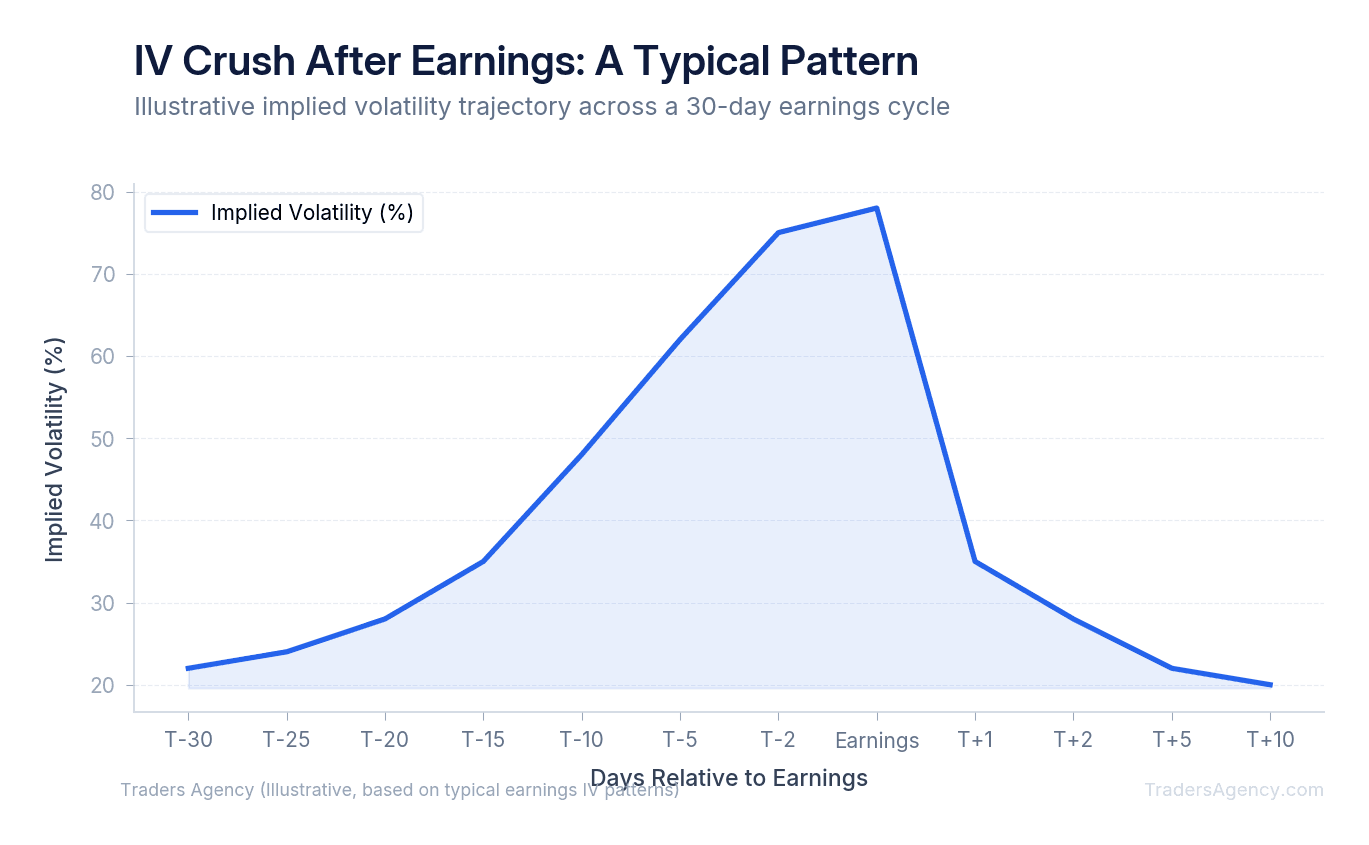

An IV crush is the sudden, sharp drop in an option's extrinsic value that happens when the uncertainty of an earnings event is resolved. Options premiums become inflated before the announcement to account for unknown price risks, then that pricing premium is removed almost instantly once the data becomes public.

To understand this mechanic, we need to look at how options are priced. Implied volatility measures the market's expectation of future price movement. Before an earnings report, no one knows exactly what the revenue, profit, or forward guidance numbers will be. That uncertainty creates massive risk for anyone selling options. The increased demand for options and the elevated risk drive premiums higher on both call options and put options.

Key Concept: Think of it like buying hurricane insurance. The day before the storm hits, insurance premiums are incredibly expensive because the risk of damage is high. Once the storm passes and the actual damage is known, the uncertainty vanishes and the cost of new insurance plummets immediately. The earnings report is the hurricane. Once the numbers are released, the market instantly reprices options to reflect a normal, lower-volatility environment.

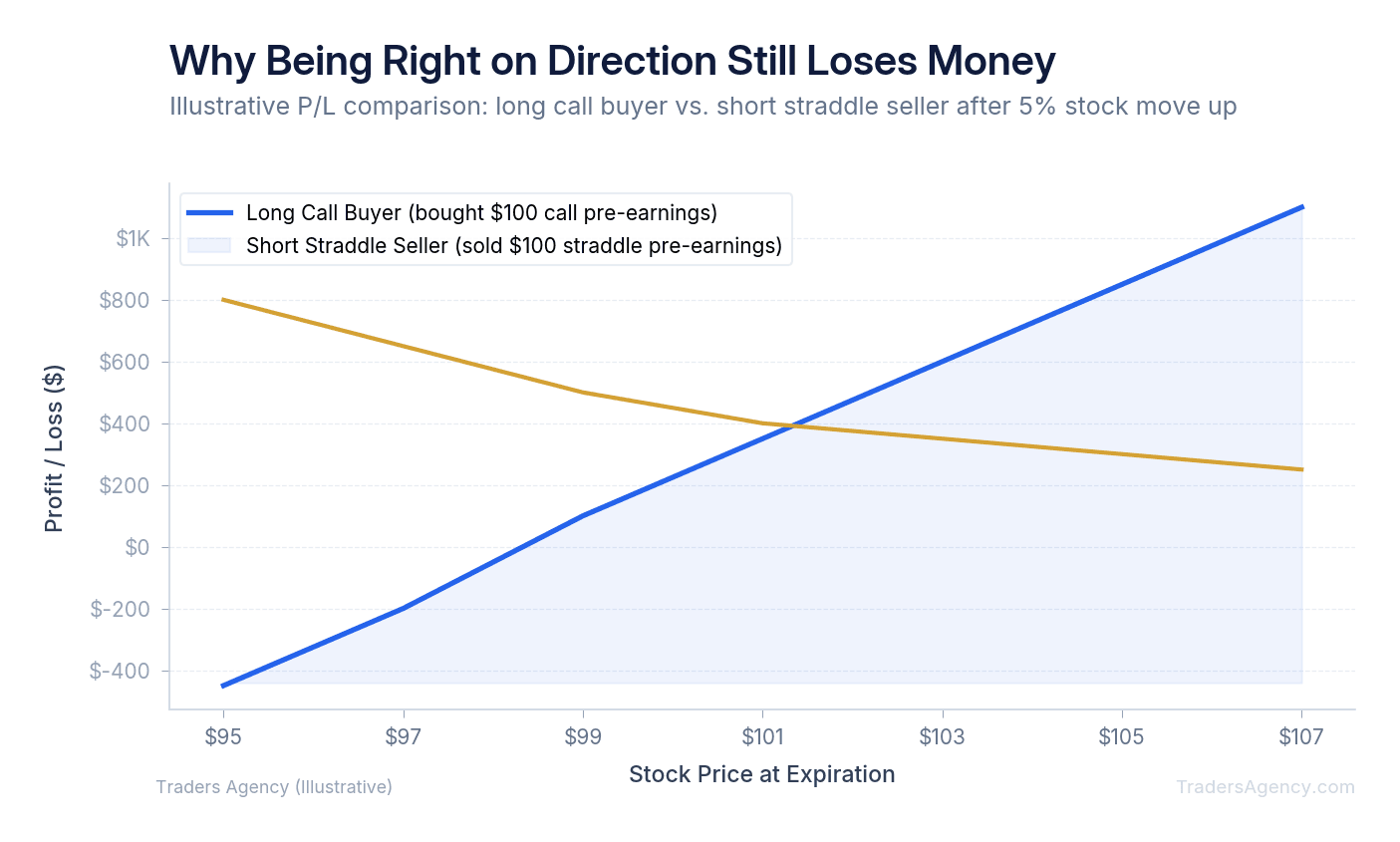

Why Does Being Right on Direction Still Lose You Money?

Many retail traders treat earnings announcements like a coin flip. They buy a long call if they expect good news, or they buy a long put if they expect bad news. The primary problem with this approach is that you're paying peak prices for those options. You're buying the hurricane insurance right as the storm makes landfall. When the earnings report drops, the implied volatility crush wipes out the inflated premium you just paid.

Options have a specific Greek metric called Vega, which measures an option's price sensitivity to changes in volatility. When volatility drops, Vega dictates that the option's price will drop alongside it. If the stock doesn't move aggressively past your breakeven price, the loss in volatility value will completely outweigh the gain in intrinsic value. You can accurately predict the stock's direction, watch the stock move in your favor, and still lose money on the trade.

Volatility contraction is the main reason long option buyers struggle during earnings season. This is a well-documented pattern in options markets, and it's one we teach our members to respect rather than fight against.

Strategies That Profit From IV Crush After Earnings: Short Straddles and Iron Condors

If buying options before earnings is a losing battle against volatility, the logical alternative is selling options. Our team prefers to act as the insurance company.

A short straddle is a classic strategy used to trade iv crush after earnings. This involves selling an at-the-money call and an at-the-money put at the same strike price and the same expiration date. You collect a large premium upfront from the inflated options prices. If the stock stays relatively flat after the announcement, the volatility crush destroys the value of both options. This allows you to buy them back the next morning for a fraction of the cost, keeping the difference as profit.

However, short straddles carry undefined risk. If the stock gaps up or down massively on a huge earnings surprise, your losses can be severe.

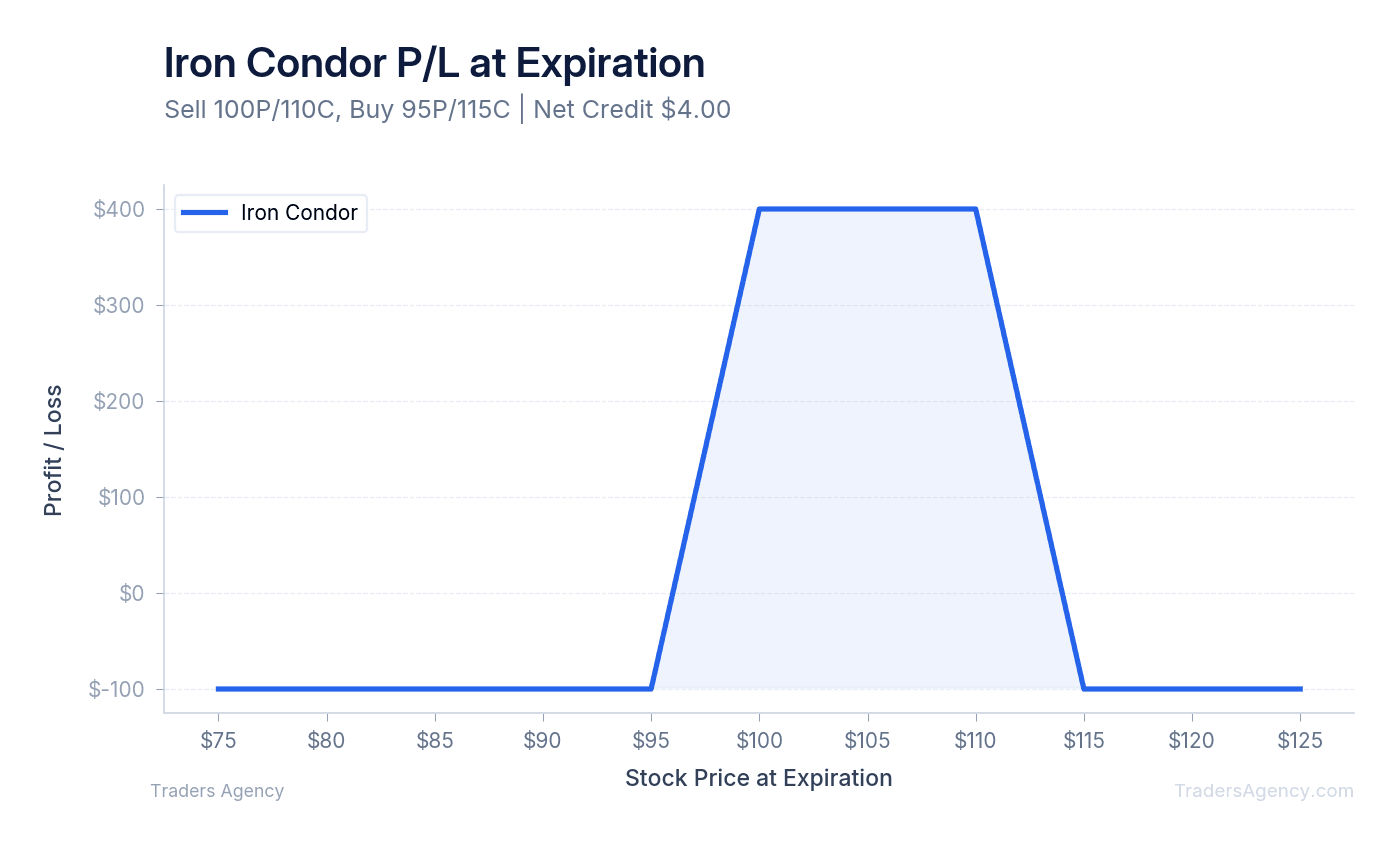

That's why we teach our members to use the iron condor strategy instead. An iron condor involves selling an out-of-the-money call spread and an out-of-the-money put spread simultaneously. This creates a wide profit tent around the current stock price. You still benefit heavily from the volatility collapse, but your maximum loss is strictly capped by the long options you purchased for protection.

Watch Out: Selling naked calls before earnings exposes you to theoretically unlimited risk, and selling naked puts exposes you to potentially catastrophic losses. A single bad earnings gap can wipe out months of progress. Always define your risk with spreads like the iron condor.

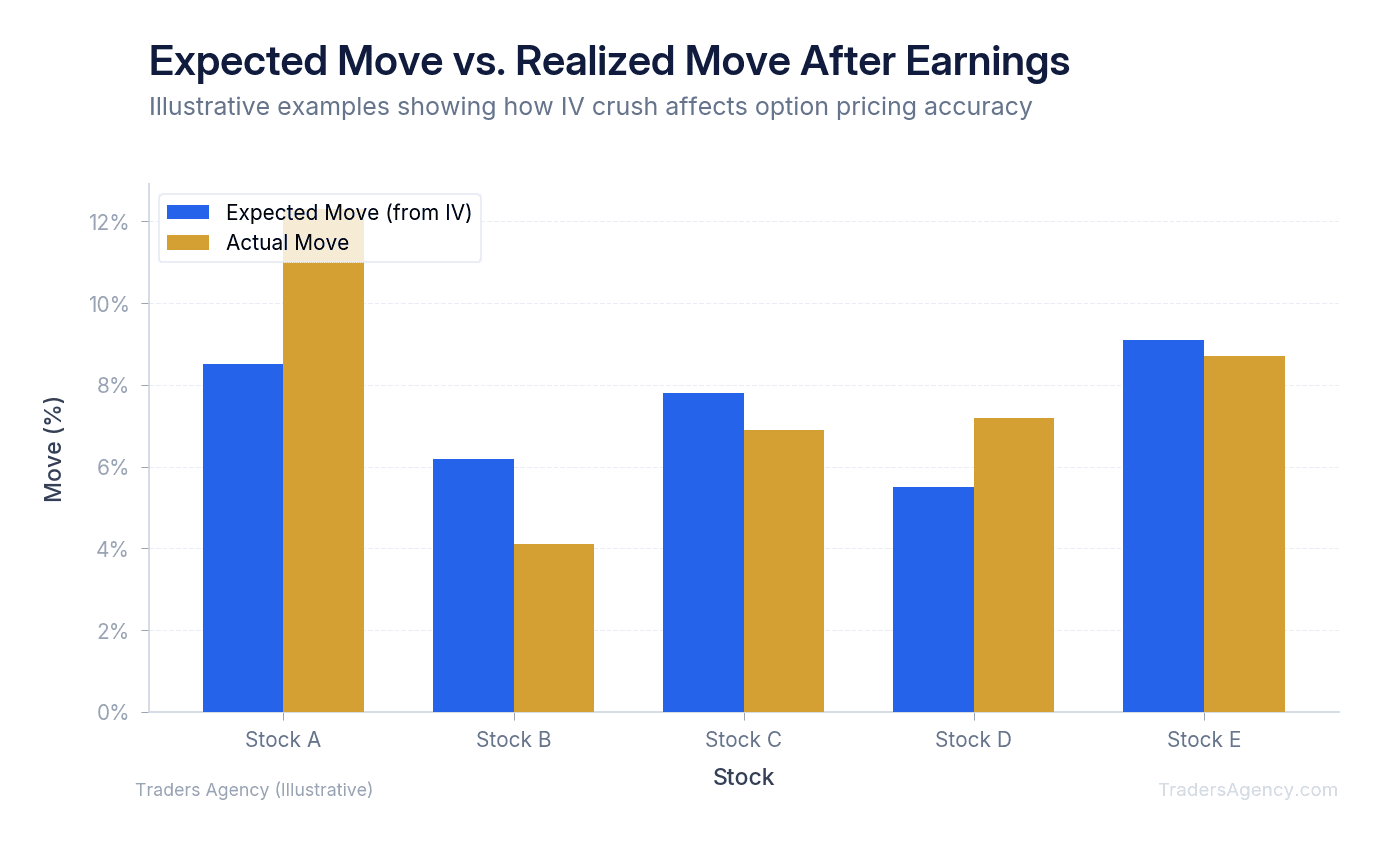

How Do You Calculate the Expected Move Before Earnings?

A common approximation for the expected move is to add the price of the at-the-money call and the at-the-money put for the nearest expiration cycle. This combined premium represents the approximate dollar amount the options market expects the stock to move up or down. (A more precise formula multiplies the straddle price by roughly 0.85, but the full straddle price is a widely used quick estimate.)

Here's a practical example. Imagine a stock is trading at exactly $100 the day before its earnings report. You check the options chain for the expiration date happening that same week. The $100 strike call costs $4.00, and the $100 strike put costs $4.00. The total premium is $8.00. Using the simplified method, the options market is pricing in roughly an $8.00 (8%) expected move in either direction. The market expects the stock to stay between approximately $92 and $108.

| Parameter | Value |

|---|---|

| Stock Price | $100.00 |

| ATM Call Premium | $4.00 |

| ATM Put Premium | $4.00 |

| Total Expected Move (approx.) | $8.00 (8%) |

| Expected Range | $92 to $108 |

If the stock only moves $3.00 after the announcement, the market severely overestimated the actual volatility. The options will experience a massive volatility contraction, rewarding the premium sellers.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyStep-by-Step Execution: The Earnings Iron Condor

Let's walk through a specific trade setup using a hypothetical stock, XYZ Corp, trading at $150 right before the closing bell on the day of its earnings report.

- Identify the Setup and Expected Move: We check the expected move on the nearest expiration chain. The $150 call and $150 put cost $5.00 each, meaning the market expects roughly a $10.00 move. We want to place our short strikes outside of this $140 to $160 expected range to give ourselves a high probability of success.

- Execute the Trade: We build the call side by selling the $165 call and buying the $170 call for protection. Simultaneously, we build the put side by selling the $135 put and buying the $130 put for protection. This creates an iron condor with $5-wide wings on both sides. We collect $1.50 in total premium, which equals $150 per contract in our account.

- Manage the Outcome: Earnings are released after the bell. The next morning, we evaluate the result and act quickly. The volatility collapse happens fast, so we aim to close the position within the first 30 minutes of the market open.

| Scenario | Stock Opens At | Action | Profit/Loss per Contract |

|---|---|---|---|

| Best Case | $152 | Buy back iron condor for $0.30 | +$120 |

| Most Likely Case | $158 | Close for partial profit as IV drops | +$70 |

| Worst Case | $175 | Call spread fully in the money | -$350 |

In the best case, XYZ reports decent earnings and opens at $152. The expected $10 move didn't happen. The volatility crush wipes out the extrinsic value of all the options, and we buy the entire iron condor back for $0.30. In the worst case, XYZ gaps to $175 and our call spread is fully in the money. Our maximum loss is the width of the spread ($5.00) minus the premium collected ($1.50), resulting in a strict $350 max loss per contract. Most of the time, the stock moves moderately, stays inside our profit tent, and the volatility drop offsets the directional move.

When Should You Trade an Earnings Volatility Contraction?

You should only trade this setup when a stock has an exceptionally high Implied Volatility Rank (IV Rank) compared to its historical average. A high IV Rank confirms that options premiums are mathematically inflated and ripe for a post-earnings collapse.

We prefer to look for an IV Rank above 50. This specific metric tells us that current volatility is in the upper half of its 52-week range. If a stock has an IV Rank of 15 right before earnings, the options are actually cheap. Selling premium in a low-volatility environment is a terrible idea because there's no inflated premium to crush. You can find the IV Rank metric on almost all modern brokerage platforms.

Key Concept: IV Rank measures where current implied volatility sits relative to its 52-week high and low. An IV Rank of 50 or higher means premiums are in the upper half of their annual range, making them ideal candidates for selling strategies. An IV Rank below 30 means premiums are relatively cheap, and selling them offers a poor risk-to-reward ratio.

We also look for companies with a proven history of staying within their expected move. Boring, established companies in sectors like consumer staples or utilities often see huge volatility spikes before earnings but rarely deliver massive price shocks. These are ideal candidates for premium selling.

Understanding historical volatility and risk is a required step for any options seller. You must know if the premium you're collecting is historically high or historically low before placing the trade.

What Mistakes Do Retail Traders Make With Earnings Options?

Trading around earnings is inherently risky. Even experienced traders can get burned if they ignore basic risk management rules. Our team reviews thousands of trades, and we see the same errors repeated every earnings season. Here are the primary mistakes we see traders make when trying to trade an iv crush after earnings:

- Ignoring position sizing: Earnings trades are binary events with instant outcomes. You should never allocate more than 1% to 2% of your total account equity to a single earnings trade.

- Holding the trade too long: The volatility collapse happens in the first 30 minutes of the market open. We teach our members to take profits immediately the next morning. Don't wait around for the stock to drift and threaten your short strikes.

- Trading low-liquidity options: If the bid-ask spread is too wide, you'll lose your entire profit edge to slippage when you try to close the trade. Stick to highly liquid stocks with penny-wide spreads.

- Selling naked options: Selling unhedged calls or puts before earnings exposes you to potentially catastrophic risk. A single bad earnings gap can wipe out months of progress. Always define your risk with spreads like the iron condor.

- Forgetting about forward guidance: A company can beat revenue and earnings estimates, but if the CEO gives poor forward guidance on the conference call, the stock will tank. You're trading the market's reaction, not just the raw numbers.

Risk Warning: Earnings trades are binary events. The outcome is determined overnight while you have no ability to adjust. Never risk more than you can afford to lose on a single earnings play, and always use defined-risk structures like iron condors or vertical spreads.

By understanding the mechanics of iv crush after earnings, you can stop gambling on directional coin flips. You can step into the role of the insurance provider, collect inflated premiums, and let the inevitable volatility contraction work in your favor. This is the approach our team uses every earnings season, and it's one that puts probability on your side.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyKey Takeaways

- A call option can lose 40% of its value even when the underlying stock moves in your favor, because the collapse in implied volatility after earnings wipes out more extrinsic value than the directional move adds.

- Options premiums are deliberately inflated before earnings to price in unknown risk. Once the announcement is made, that uncertainty premium is removed almost instantly, regardless of whether the news is good or bad.

- Professional traders approach IV crush by selling options before earnings rather than buying them, positioning themselves as the 'insurance provider' collecting inflated premiums before volatility contracts.

- Defined-risk structures like iron condors and vertical spreads are the preferred vehicles for earnings trades because the outcome is determined overnight with no ability to adjust the position.

- The market's reaction to forward guidance on the earnings call often matters more than the raw numbers. A stock can beat estimates and still sell off if the CEO's outlook disappoints.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources