SpaceX stock is massively overvalued, and I still want to buy it. Many are asking whether SpaceX is overvalued at this price, and the answer is clearly yes.

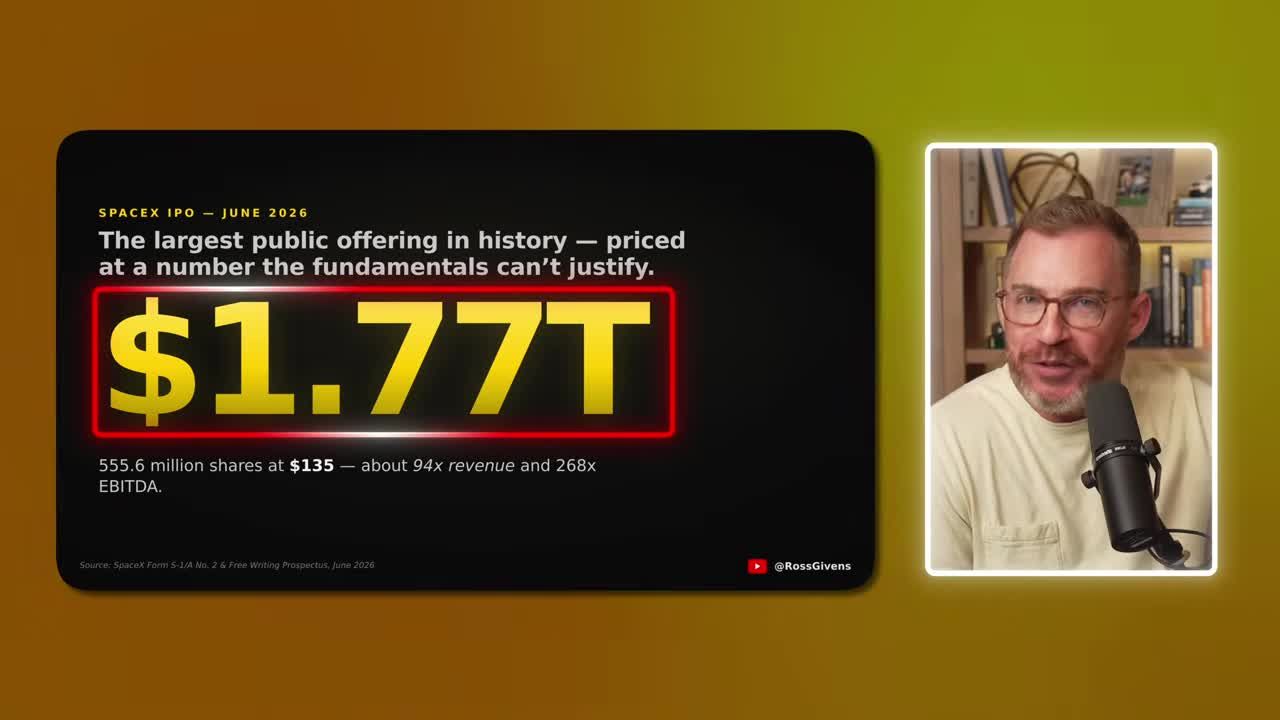

The company is going public at $135 a share, making it the biggest IPO of all time. On day one, the market is slapping a $1.775 trillion valuation on this business. That number is completely disconnected from the actual fundamentals. On the numbers, SpaceX is worth about half of that.

But in the short term, this is a momentum trade driven entirely by supply and demand.

Is SpaceX Overvalued? What the Numbers Actually Say

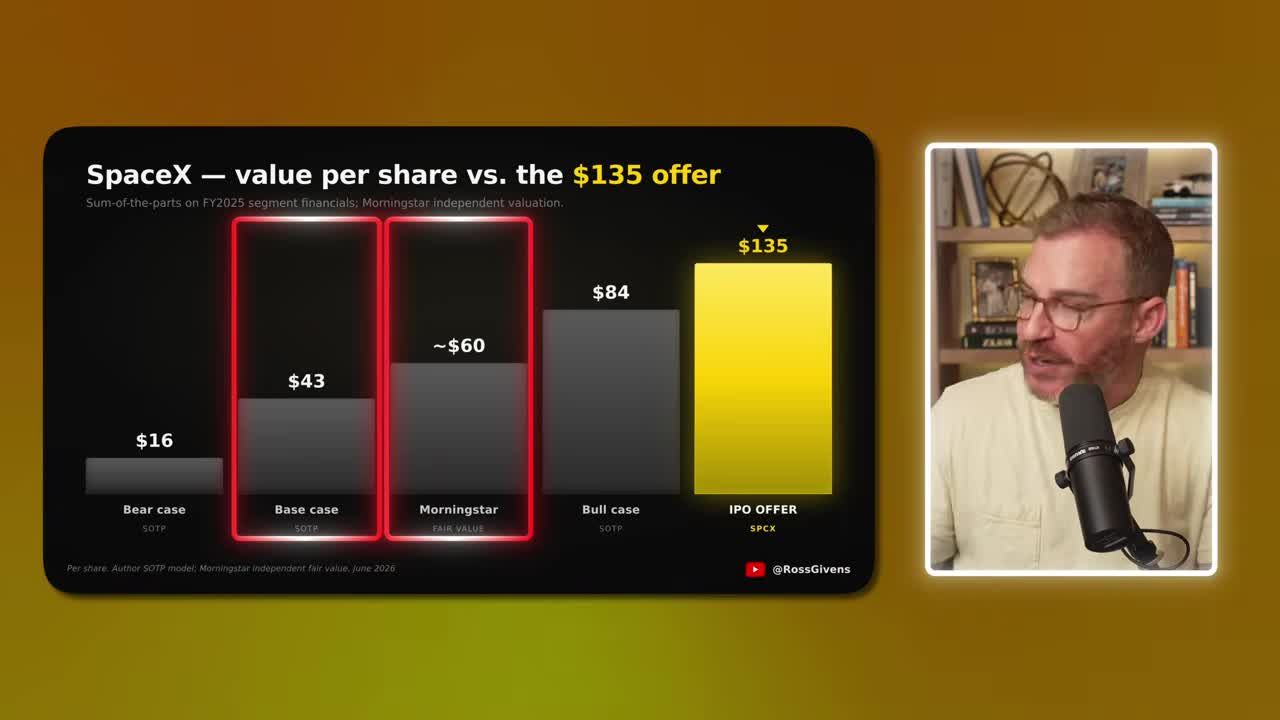

Morningstar puts the fair value at around $60 a share. They flat out say the stock is overvalued by half. My own breakdown is even more conservative, landing at a base case of around $42 a share.

I built a valuation model using the S-1 filing and the SpaceX prospectus. The math is clear.

- Bear case (things go poorly): $16 a share

- Base case: $42 a share

- Bull case (optimistically): $84 a share

None of these scenarios justify the $135 asking price. Everyone agrees the valuation is incredibly rich.

But the price tag simply does not matter right now. I have never in 20 years of doing this seen this kind of appetite for a single stock. The biggest IPO in history is heavily oversubscribed. Most people who want it will not get pre-IPO shares at $135. They are going to pay much more when it opens for trading on June 12th.

The $135 Premium

Why the market is willing to pay this much

The $135 asking price is based on the assumption of perfect execution for the next five years. Investors are pricing in perfect execution of rocket launches, putting thousands of satellites into orbit, and building data centers in outer space.

If anyone can do it, it is Elon Musk. But that is a big leap to just assume every goal is going to get hit on target. We are riding demand right now, not value. That is fine, but let's not confuse the two.

Three Businesses, One Ticker

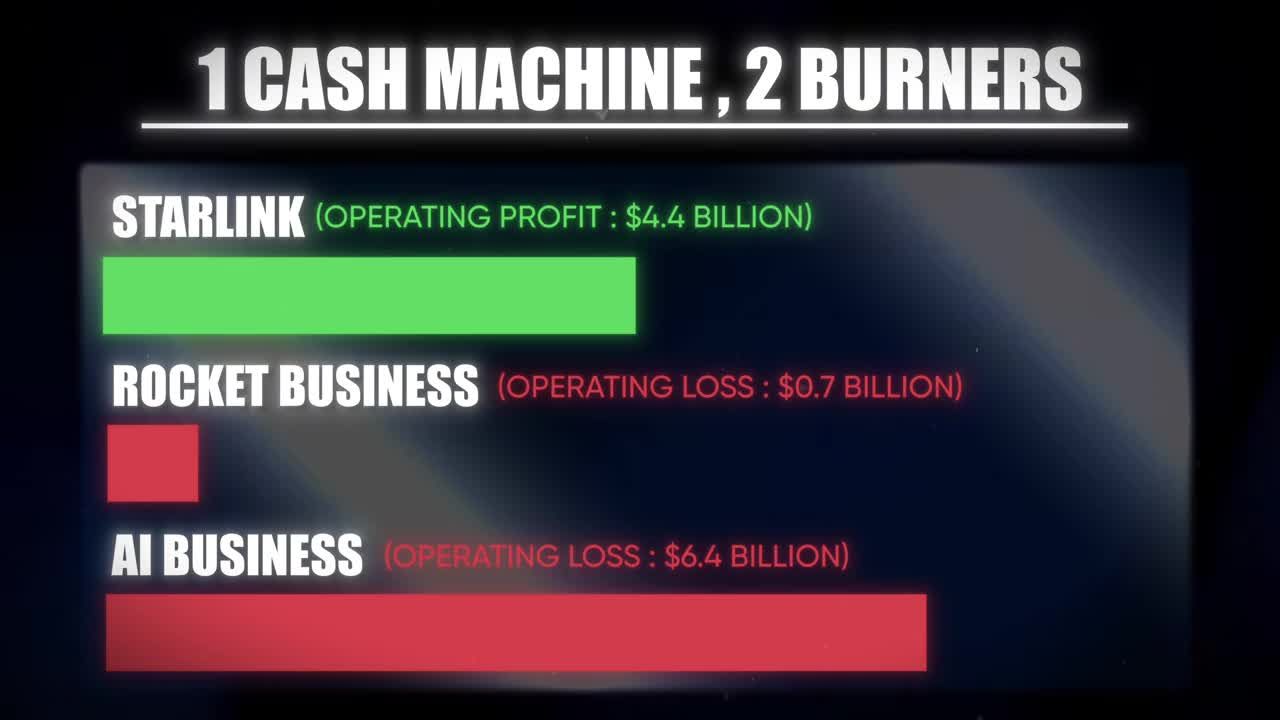

SpaceX is not a simple company. It is actually three separate businesses rolled into one. You have one cash machine carrying two cash burners.

1. Starlink (the monster). $11.5 billion in revenue last year, growing about 50% year-over-year. This segment tosses out real profit: $4 billion in operating income. They have 10 million subscribers and climbing. If SpaceX were just Starlink, the massive valuation would make a lot more sense.

2. The Rocket Business (the monopoly). It flies more than 80% of everything that all of humanity puts into orbit. Total monopoly. And it still lost money last year. They are pouring everything into Starship.

3. The AI Business (the cash furnace). xAI, Grok, the whole thing, folded in earlier this year. That segment did about $3 billion in revenue last year but lost about $6 billion doing it. Right now, it is a cash furnace. Most of these big hyperscale AIs are right now. Big expenses up front, potentially massive payout down the line.

What Is SpaceX Actually Worth at $135 a Share?

When you project out the next two years, the revenue growth expectations are staggering. Anything beyond 2027 is just throwing darts at a wall.

My base case assumes a 32% compounded annual growth rate through the end of 2027. That is more than healthy. The bear case assumes 20% growth, a pace most of the S&P 500 would kill for. The bull case projects 45%.

I ran comparable metrics against fast-growing tech companies like Nvidia and Tesla, looking at price-to-sales multiples and enterprise value to revenue. Even with generous multiples, the numbers do not add up to $1.775 trillion. So yes, SpaceX overvalued is not just an opinion; the math backs it up.

But again, price in the short term has nothing to do with value.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWhy Is the SpaceX IPO So Heavily Oversubscribed?

How high can SpaceX go in its first week?

There is a real chance this stock could rise another 50% in the first week just from the buying frenzy. The demand here is unlike anything we have ever seen.

Musk skipped the whole Wall Street dance entirely. No price range. No testing the waters. He set the price at $135. Take it or leave it. He knows he is way out on the edge of realistic value. He is not trying to squeeze every last penny out of it.

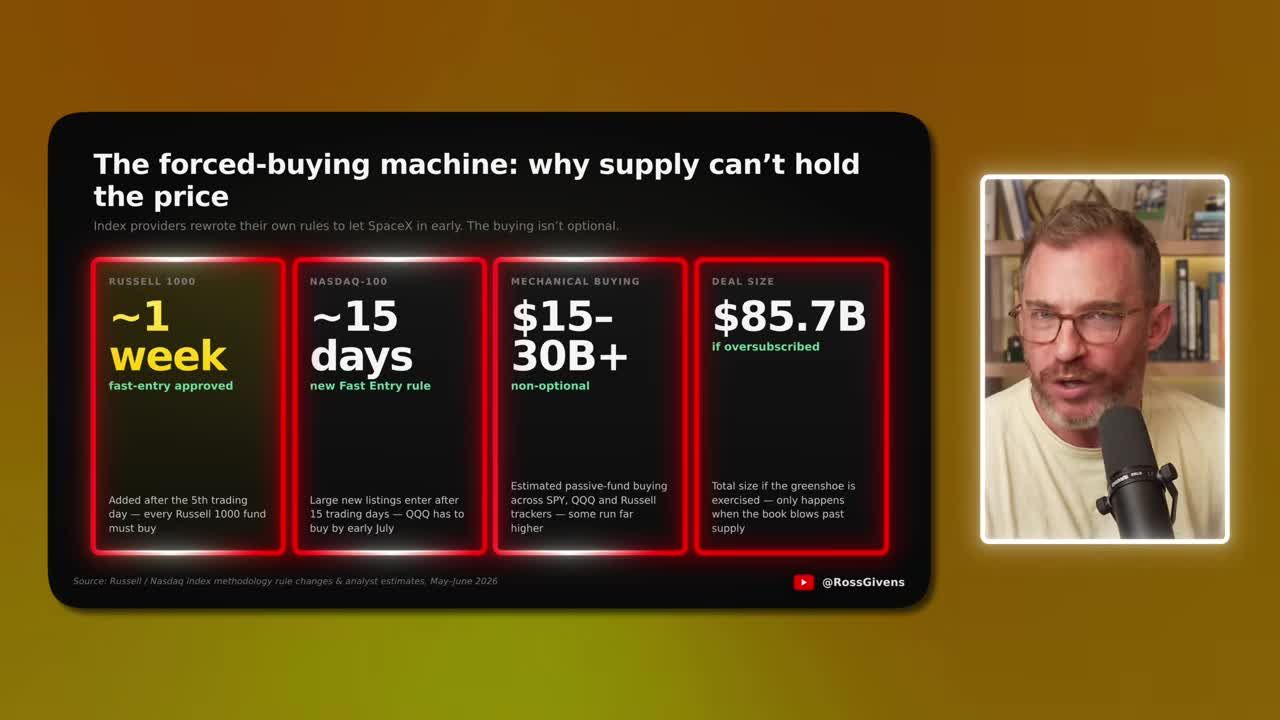

Despite the high price, the deal is heavily oversubscribed. The underwriters, Morgan Stanley and Goldman, have an option to sell another $11 billion of stock on top of the base deal, another 15%. But even that is not going to be near enough to satisfy demand.

The Rule Changes That Force Buying

Why index funds are being forced to buy

The big index providers rewrote the rulebooks to let SpaceX in early. This forces index funds to buy the stock regardless of price.

The Russell 1000 approved a fast-entry rule. SpaceX gets added about a week after the IPO, right after the fifth day of trading.

The NASDAQ 100 changed its methodology so that any new listing big enough now comes in after just 15 days. That means QQQ, one of the most widely held exchange-traded funds on the planet, has to go out and buy this stock by early July.

The S&P 500 is still consulting on a rule change, so that wave of buying probably does not hit until later this year.

Index inclusion is not optional buying. Every fund tracking those indexes, every 401(k), every target-date fund, trillions of dollars on autopilot, has to buy the stock to match the index. That is forced buying on top of a deal that is already oversubscribed, on top of record demand.

Can Retail Investors Get SpaceX IPO Shares?

Usually retail investors are lucky to get allocated 5% or 10% of an IPO. Most goes to the big institutions. Elon demanded that retail investors get 30%. Those shares are being divided between five firms: Robinhood, SoFi, Fidelity, Charles Schwab, and E-Trade.

Musk has a rabid following among retail investors. Millions of people want to own a piece of the company taking us to Mars. They do not care what Morningstar thinks the fair value is. They just want to own shares of SpaceX. Period.

You have a fixed price that is massively sold out. You have most of the demand locked out of the $135 pre-IPO shares. When a wall of money meets a sliver of supply, the price goes up fast.

How I'm Playing It

If you do not get an allocation at the $135 pre-IPO price, do not buy the stock on day one. Trading opens at 8:30 a.m. Central on Friday, June 12th, and the stock will likely open at a massive premium.

I fully expect the stock to trade well north of where it opens. I will not be surprised if it hits $200.

I filled out an indication of interest at Fidelity to get IPO shares. I have no idea if I will get them or not. If I get an allocation at $135 and the stock hits $200 in a week, I am selling. Period.

Brokers do not want you to flip the stock immediately. A lot of them will fine you or cut you off from future IPOs if you do. I do not care. I will take the gift and walk away.

If I do not get IPO shares, I am not paying $150 or $160 or whatever this thing opens at that Friday. Most people I have talked to plan to hold this one forever. For me, it is just another trade. If it sets up as a good buy later, I will take it. If not, there are 6,000 other stocks to trade.

The Death of Price Discovery

When a company goes public, it typically goes through a price discovery period. Buyers and sellers try to decide what the business is actually worth. The stock may double or it may fall 90%, but it needs that natural auction process.

That is not happening here. Between the fixed price, the massive retail lockout, and the forced index buying, natural price discovery is dead.

It would be natural for this stock to fall 50% from peak to trough. That is how it has been since the Bank of North America first went public in 1783. But they changed the rules so that will not happen. Plus, everything Elon touches turns to gold. This stock is going to have a cult-like following.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- SpaceX IPO priced at $135 per share, implying a $1.775 trillion valuation, making it the largest public offering in history.

- A custom valuation model using the S-1 filing puts fair value at $42 per share in the base case, $16 in the bear case, and $84 in the bull case. None support the $135 price.

- Morningstar independently pegs fair value at roughly $60 per share, calling the stock overvalued by approximately half.

- Despite the valuation gap, the IPO is heavily oversubscribed, meaning most retail investors who want shares will not receive an allocation at the offering price.

- The near-term thesis is a momentum and supply-demand trade, not a fundamentals trade. The longer-term bull case rests partly on a potential SpaceX-Tesla merger.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources