January 1st, 2027. That is the exact date the Pentagon makes it illegal to put a Chinese-made magnet inside any US weapons system. Not a suggestion. A hard deadline written into federal law. China rare earth export restrictions have already started squeezing the supply chain, and the United States currently has no scaled-out replacement. Every major weapons system relies on materials that are about to be legally banned from the supply chain.

What Does the Pentagon Rare Earth Ban Actually Require?

Bottom Line: The January 1, 2027 Pentagon deadline is a legally binding supply chain crisis with no obvious off-ramp. The loopholes are closed, the weapons systems are dependent, and the domestic production base is nearly nonexistent. The thesis rests on Realoys being the single investable company positioned to fill that gap, which makes the stock call entirely contingent on whether that operational claim holds up under independent due diligence.

After January 1st, 2027, every stage of magnet production must happen outside of China, Russia, Iran, and North Korea. If a defense contractor uses a magnet where even one single stage of production touched those countries, the magnet is banned from US weapons.

This rule was originally written into the 2023 NDAA. Then Congress came back the next year and made it even harder.

Contractors used to rely on a massive loophole. They would melt Chinese oxides in Vietnam, press them into a magnet, and stamp the magnet as non-Chinese. That loophole is completely dead.

Every single stage must be clean: mining, refining, separating, melting, fabrication. If just one of those steps happens in China, the magnet does not go into the weapon. Period.

F-35s, Tomahawks, and the Problem

The ban directly impacts production of F-35s, Tomahawks, guided missiles, Navy ships, and advanced satellites. Every single one of these weapons systems runs on rare earth magnets that today get made in China. Without an alternative supply chain, these weapons programs simply will not ship.

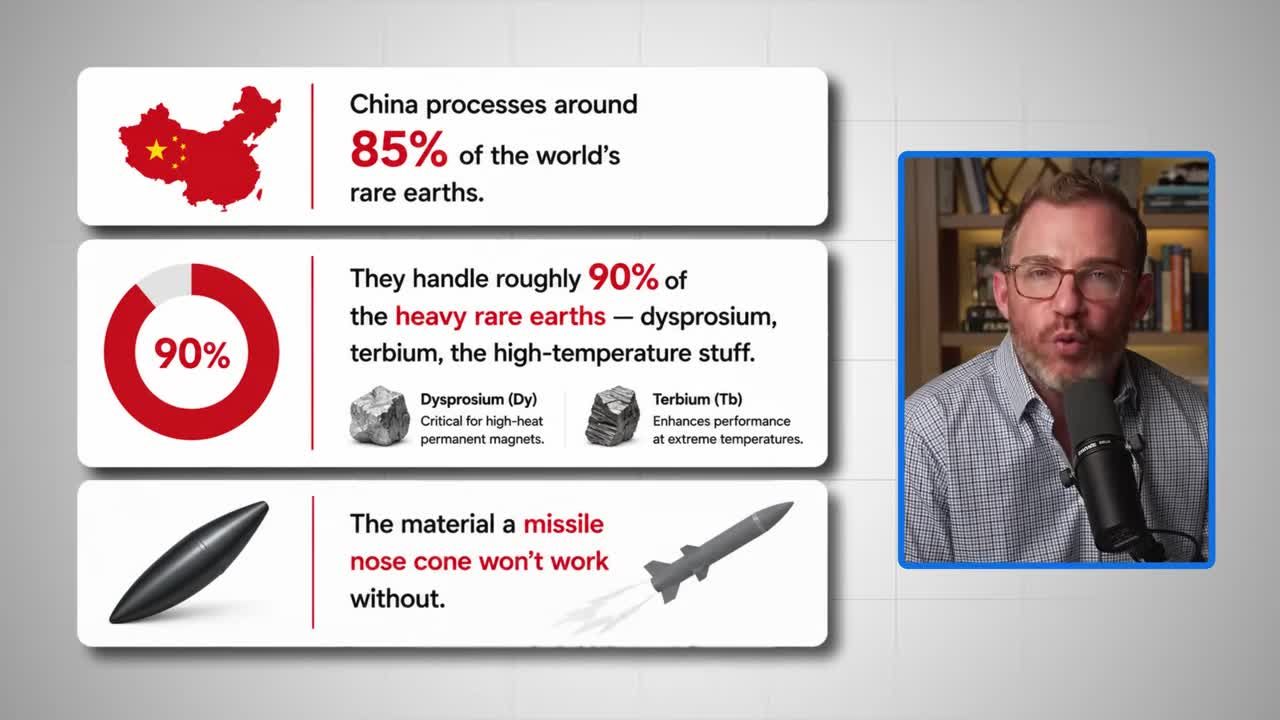

I am talking about materials like dysprosium and terbium. The high-temperature stuff. The material a missile cone will not work without.

Without heavy rare earths, the magnet demagnetizes. The weapon fails.

How Are China Rare Earth Export Restrictions Affecting US Defense Supply Chains?

Most government deadlines get pushed back. This one already got moved up.

Last year in 2025, China stopped pretending it was a passive supplier. Beijing imposed export licensing restrictions on rare earth magnets and the materials that go into them.

The impact was immediate. US drone makers were waiting weeks for shipments that used to clear in days. Defense subcontractors had to halt production lines while their applications sat on a desk in Beijing.

That was China telling Washington: we control the spigot. We can turn it down whenever we want, and we are not going to give you a heads up.

When China throttled the supply, weapons programs slipped. The Pentagon had to deal with the delay. Those China rare earth export restrictions proved exactly why the January 1st, 2027 deadline matters.

Washington is legally requiring an alternative chain. This deadline is not going to move.

The Coming Structural Shortage

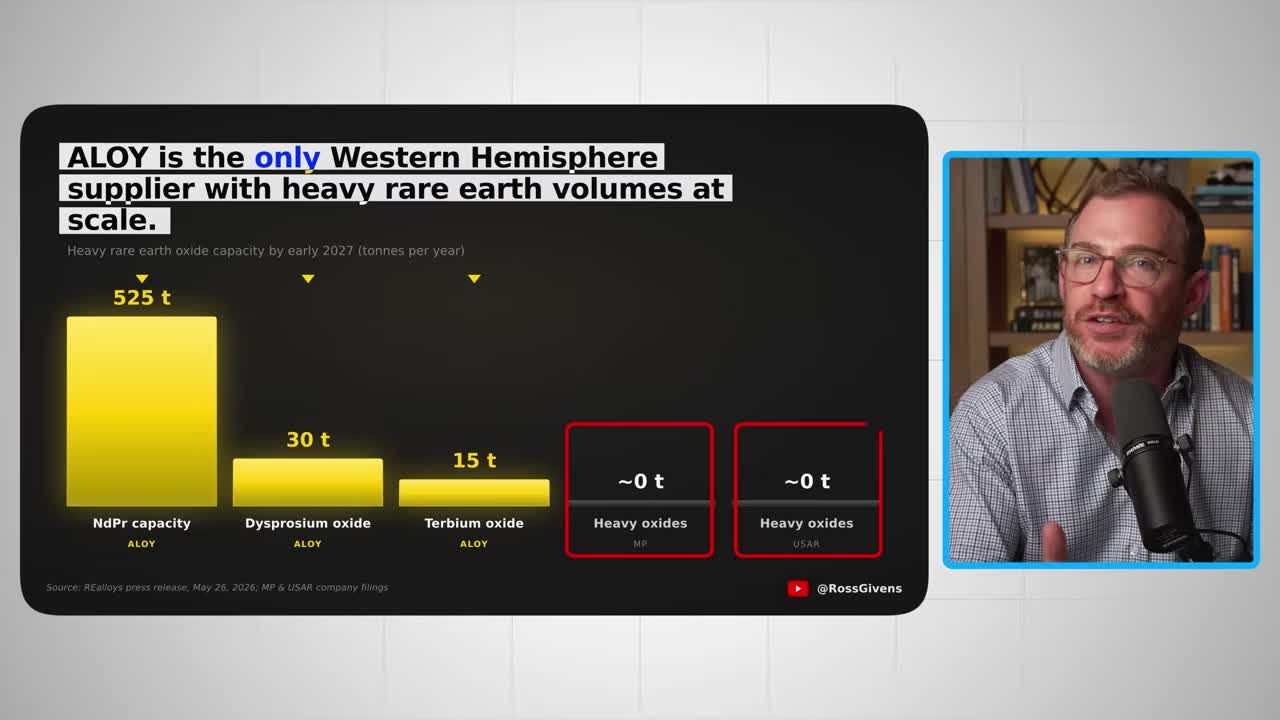

The United States has exactly one commercial heavy rare earth metallization facility in the continental US. Just one.

The largest American mine-to-magnet project on the drawing board today is targeting roughly 10,000 tons a year by the end of the decade. The problem? US demand at the end of the decade is roughly double that.

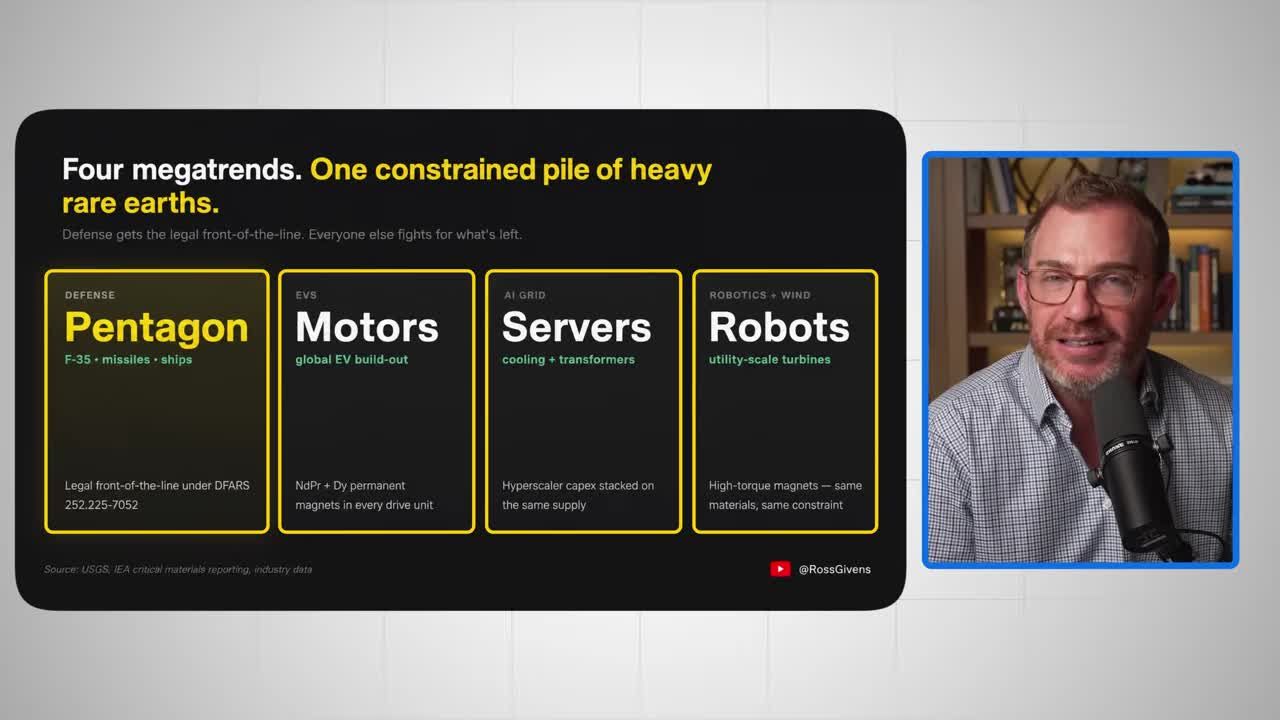

Defense contracts get the headlines, but the heavy rare earths going into a missile guidance system are the exact same materials needed for other massive industries.

You have four mega-trends bidding for the same pile of dysprosium and terbium:

- Defense systems

- EV motors

- Utility-scale wind turbines and cooling systems inside AI data centers

- Advanced robotics arms

The Pentagon just legally put itself at the front of the line. Every other buyer competes for what is left.

This is not a regulatory issue. There is about to be a real structural shortage, and it starts in seven months. Can you imagine what happens to the company that actually delivers heavy rare earth oxides, the dysprosium, the terbium, and the samarium-grade material between now and into 2027?

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubIs There a Full Rare Earth Supply Chain Outside of China?

The company positioned for this shift is Realoys, ticker ALY. It trades on the NASDAQ. Small cap, valued around $600 million. That is tiny in the context of the trade it is positioned for.

What makes Realoys different from competitors like MP Materials or USA Rare Earth is one word: heavy.

The headline names mostly handle light rare earths like neodymium and praseodymium. Important stuff, but only half the puzzle. The heavy rare earths, your dysprosium, your terbium, are what let a magnet hold its strength inside a missile cone at 400 degrees. Without those, the magnet demagnetizes. The weapon fails. Realoys has the only meaningful heavy rare earth supply line ramping up in the Western Hemisphere right now.

The Structural Moat

Companies like MP and USOR handle one stage of the supply chain. MP mines and does separation. USA Rare Earth processes feedstock. They are a piece of the puzzle, not the whole picture.

Realoys spans the entire chain under one roof: mining feedstock, separating the oxides, refining the metals, building the magnet components. A true mine-to-magnet operation. Think farm-to-table, but for defense materials.

Why the Pentagon Demands This

Go back to the rules of the 2027 ban. Every single stage has to be non-Chinese.

A defense contractor cannot piece together a clean supply chain out of five different vendors and pray that none of them touch China at any step. The Pentagon wants one certified supplier they can audit end-to-end.

That is exactly what vertical integration buys you. It is the simplest way for federal agencies to comply with their own rule. Vertical integration is no longer just a nice feature. Under this 2027 rule change, it is a qualifying feature.

This is not a story stock waiting for sales. The customers are already sitting at the table.

The Partnerships and Capital

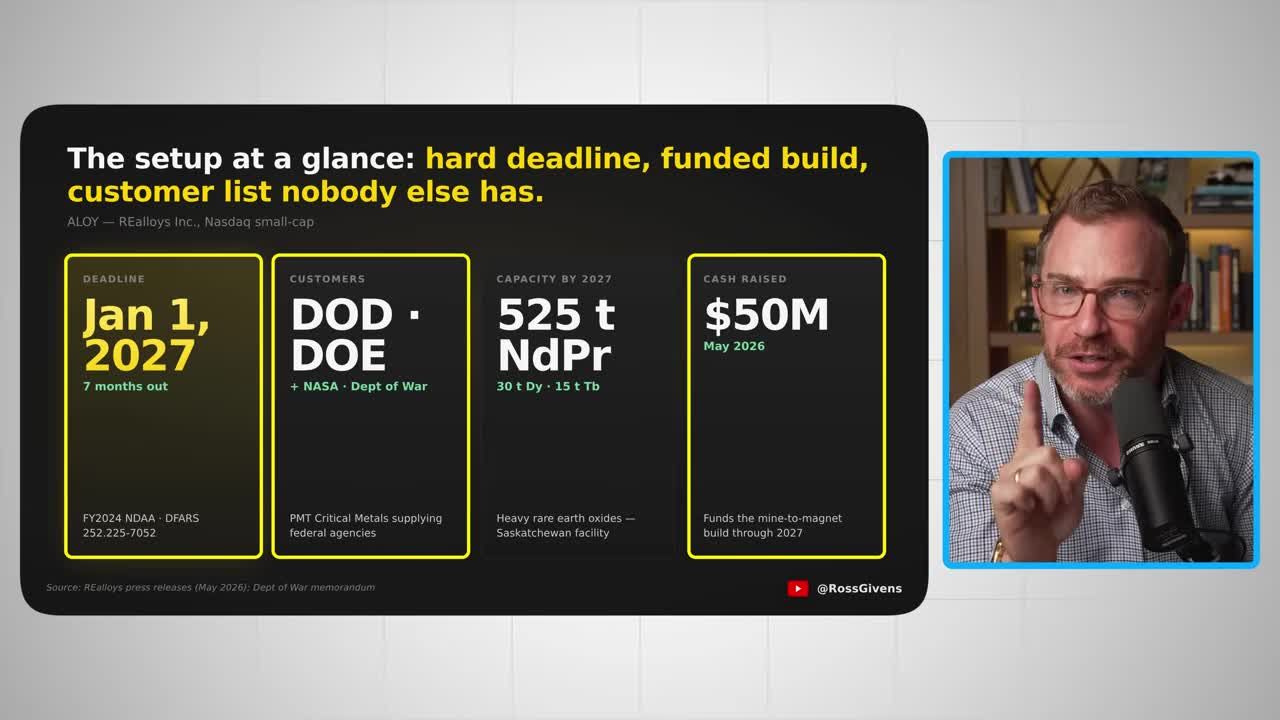

In May, Realoys received a formal memorandum from the US Department of War recognizing the company as the domestic heavy rare earth solution. That is a government-stamped invitation to take a meaningful role in a federal supply chain.

They have locked in feedstock partnerships across the map.

Saskatchewan, Canada: A $20.6 million investment in a Saskatchewan Research Council facility, giving them preferred rights to up to 80% of the expanded output.

Southern Greenland: An offtake agreement with Critical Metals Corp. for 15% of the Tanbreeze project.

Montana: A memorandum with US Critical Materials covering up to 10% of the Sheep Creek project.

To fund this massive mine-to-magnet build, they raised another $50 million in fresh capital. That is what a credible build looks like.

The Technical Setup for ALY

This stock moves fast. It made a five-fold run last year, hitting $27 a share in March.

Today it trades for around $9. That is roughly two-thirds off its high, hugging the 200-day moving average at the bottom of the chart.

There is real accumulation building over the last couple of months. Once that January 1st deadline hits, I would not be surprised to see this stock push into the $20s or potentially $30s per share.

There is a lot of upside on this stock, and that move could happen very quickly.

The Asymmetric Setup

Do not bet the farm on any single small cap stock. But the setup here is undeniable.

A firm January 1st, 2027 deadline. China rare earth export restrictions already squeezing the market. The DoD, DOE, NASA, and the Department of War already in the customer file. A fresh $50 million raise and the only heavy rare earth supply line in the Western Hemisphere.

This is exactly the kind of asymmetric setup I look for in the markets.

The US government cannot let this supply chain fail. They wrote the deadline into law. There is exactly one publicly traded small cap in the Western Hemisphere with the heavy oxide volumes to plug the hole, and it is Realoys.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- The 2023 NDAA mandates that all Chinese-origin rare earth magnets be eliminated from US defense systems by January 1, 2027, with no exceptions for partial foreign processing.

- The old loophole of melting Chinese oxides in Vietnam and relabeling magnets as non-Chinese is explicitly closed. Every stage of production, from mining through fabrication, must occur outside China, Russia, Iran, and North Korea.

- Every major US weapons platform including the F-35 and Tomahawk missile relies on rare earth magnets that currently touch the Chinese supply chain, making the 2027 deadline a hard structural problem, not a policy preference.

- Realoys is identified as the only publicly traded small-cap company in the Western Hemisphere with heavy rare earth oxide volumes sufficient to serve as a domestic alternative, with a $50 million raise completed and existing defense customers on file.

- China rare earth export restrictions already in effect are compressing the available supply window before the 2027 ban takes hold, meaning the shortage pressure is active now, not theoretical.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources