You've probably seen it happen before. A company announces earnings, the stock gaps up or down 15%, and you wish you had a way to trade that explosion in volatility without guessing the direction. That's exactly what we're walking you through today. We'll compare the straddle vs strangle, two options strategies designed to capture major price movements regardless of which way the stock moves. By the end of this guide, you'll know how to set up both trades, manage the risks, and decide which one fits your market outlook.

What Is a Straddle and How Does It Work?

Bottom Line: The straddle and strangle serve the same core purpose: profiting from a large price move without picking a direction. The real decision comes down to cost versus required movement. If you expect a violent, nearby move, the straddle gets you there faster. If you want cheaper exposure and are comfortable waiting for a bigger swing, the strangle is the better fit.

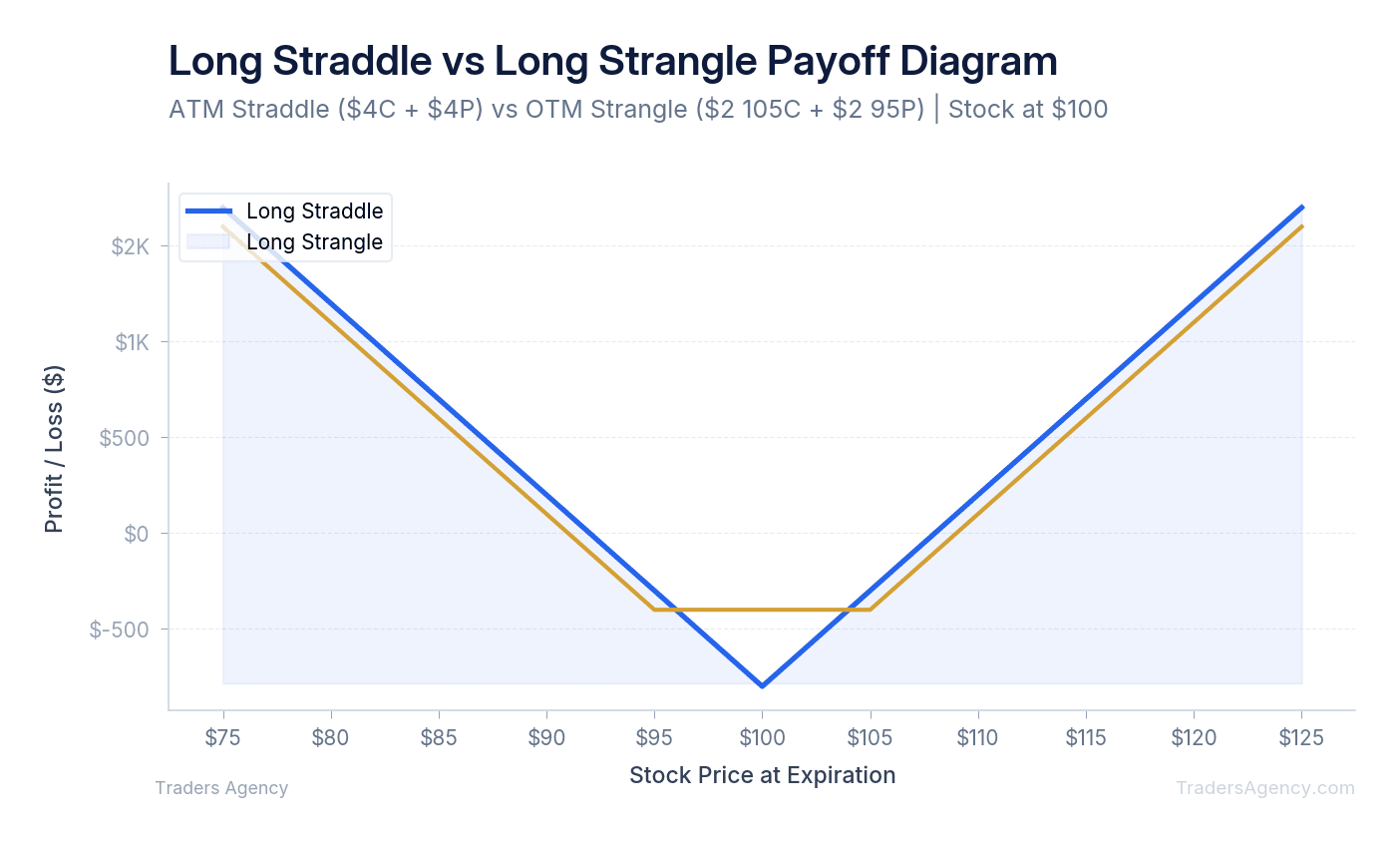

A long straddle is an options strategy where you buy both a call option and a put option with the exact same strike price and expiration date. This creates a position that profits from extreme volatility. You make money if the underlying asset moves sharply in either direction beyond your total premium paid.

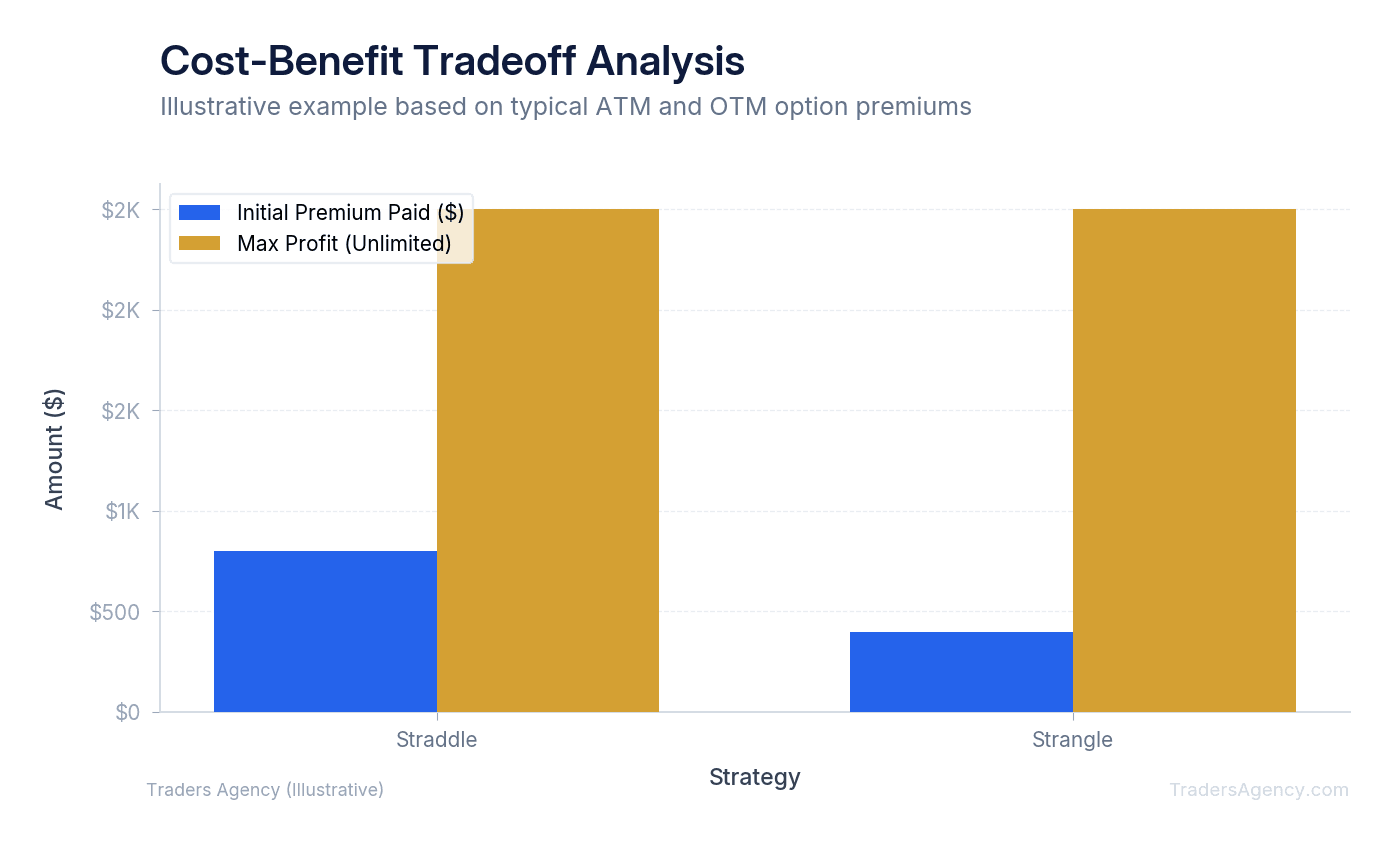

We teach our members to use at-the-money (ATM) options for this setup. Because you're buying two ATM contracts, the upfront cost is relatively high. ATM options carry the most extrinsic value, which means you need the stock to move significantly just to cover the premium you paid. If the stock barely moves, both options lose value rapidly.

Key Concept: A long straddle uses two at-the-money options (same strike, same expiration). Your maximum risk is strictly limited to the total premium you pay upfront. You profit when the stock makes a large move in either direction.

What Is a Strangle and How Does It Work?

A long strangle involves the purchase of an out-of-the-money (OTM) call and an out-of-the-money put with the same expiration date. Because the strikes are further away from the current stock price, the initial cost is lower than a straddle, but the stock must move further to reach profitability.

We prefer to use a strangle when we want to limit our upfront capital risk. The tradeoff is that OTM options require a much more aggressive price swing to reach your breakeven points. If the stock stays flat or only moves slightly, both options will expire worthless. Like the straddle, your maximum possible loss is capped at the initial premium paid to enter the trade.

What Are the Key Differences Between a Straddle and a Strangle?

When comparing a straddle vs strangle, the primary difference comes down to your strike placement and capital outlay. A straddle centers precisely on the current stock price. A strangle creates a wider gap between your call and put strikes. Here's how we break down the differences for our traders:

| Factor | Long Straddle | Long Strangle |

|---|---|---|

| Strike Selection | Both options at the money (ATM) | Both options out of the money (OTM) |

| Initial Cost | Higher (ATM options hold more value) | Lower (OTM options consist entirely of extrinsic value) |

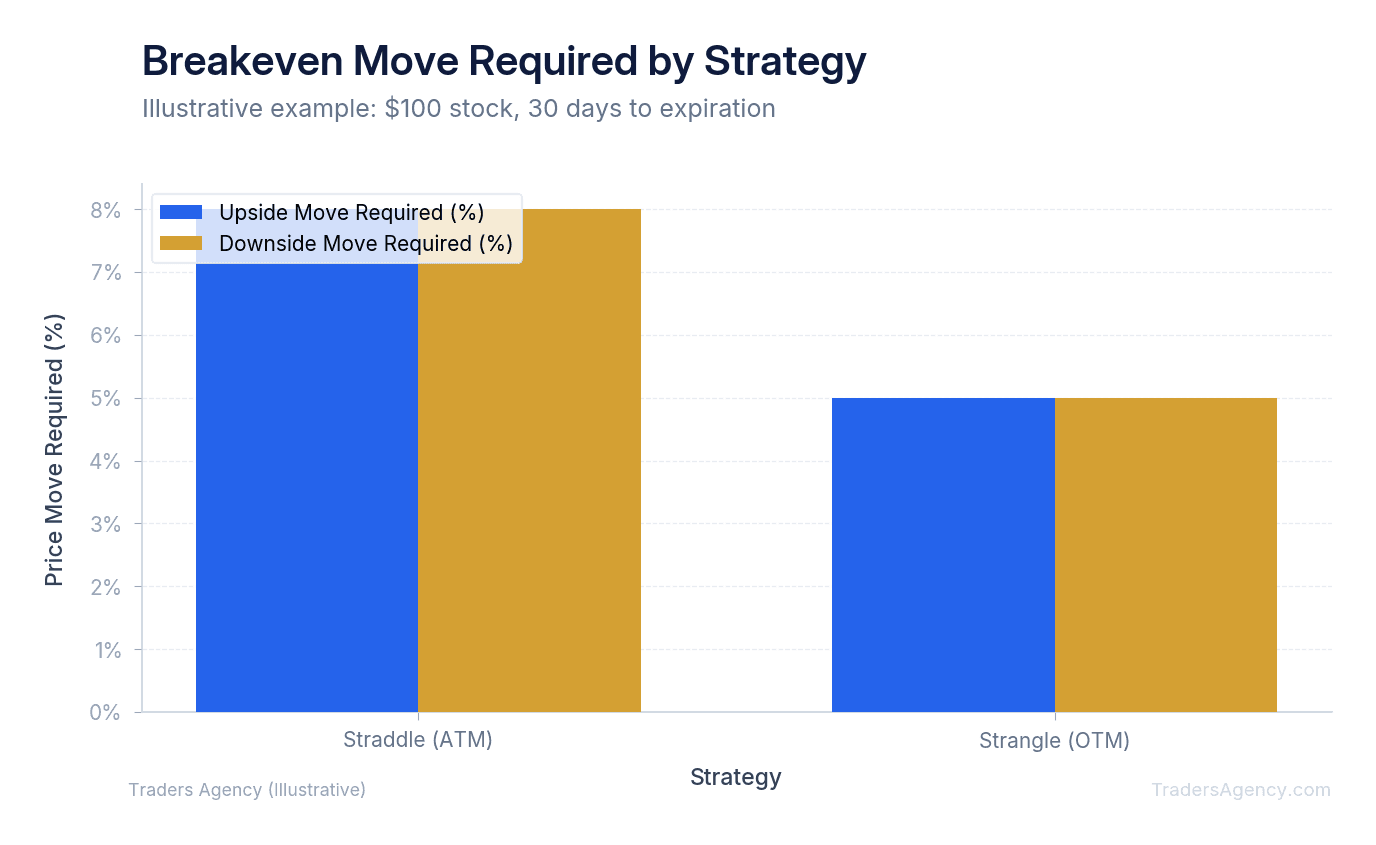

| Breakeven Distance | Smaller percentage move required | Larger percentage move required |

| Probability of Profit | Slightly higher (tighter breakeven points) | Lower (wider breakeven points) |

| Capital at Risk | More dollars on the line | Fewer dollars on the line |

| Maximum Loss | Total premium paid | Total premium paid |

When Should You Use a Straddle vs a Strangle?

Your choice between a straddle vs strangle should be based on your budget and your conviction in the size of the upcoming move. Use a straddle when you expect a moderate to large move and can afford the higher premium. Use a strangle when you expect an absolutely massive, historic price swing and want to risk less capital.

Our education team looks for specific market events before deploying either strategy. We want to see an upcoming earnings report, a pending regulatory decision, or a major macroeconomic announcement. These events force the market to reprice the stock instantly, and that repricing is where these strategies thrive.

When to Use a Straddle

Use a straddle when you expect a significant price movement but implied volatility is relatively low. Because you're buying at-the-money strikes, the options are expensive. Low implied volatility keeps your initial costs down and improves your chances of reaching profitability quickly. You're paying a premium for proximity to the current price, and that's ideal when you know a stock will move but aren't sure it will be a record-breaking swing.

When to Use a Strangle

Use a strangle when you anticipate a massive, historic price swing but want to risk less upfront capital. By selecting out-of-the-money strikes, your initial premium cost is much lower. However, the underlying stock must move significantly further to reach your breakeven points. We prefer a strangle when implied volatility is already somewhat elevated, making ATM options too expensive. You must be highly confident that the impending price shock will be violent enough to blow past your wide strikes. This is a lower-probability trade that pays off handsomely when extreme outliers occur.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyProfit and Loss Examples with Real Numbers

Let's look at a concrete example using a hypothetical stock, XYZ Corp, currently trading at $100 per share. You expect a massive move after their earnings call next week.

The Straddle Setup

For the straddle, you buy the $100 strike call for $4.00 and the $100 strike put for $4.00. Both expire in 30 days.

| Parameter | Value |

|---|---|

| Strategy | Long Straddle |

| Call Strike / Premium | $100 / $4.00 |

| Put Strike / Premium | $100 / $4.00 |

| Total Premium Paid | $8.00 per share ($800 per contract) |

| Upside Breakeven | $108.00 ($100 strike + $8.00 premium) |

| Downside Breakeven | $92.00 ($100 strike - $8.00 premium) |

| Max Loss | $800 if XYZ closes exactly at $100 at expiration |

The Strangle Setup

For the strangle, you buy the $105 strike call for $1.50 and the $95 strike put for $1.50.

| Parameter | Value |

|---|---|

| Strategy | Long Strangle |

| Call Strike / Premium | $105 / $1.50 |

| Put Strike / Premium | $95 / $1.50 |

| Total Premium Paid | $3.00 per share ($300 per contract) |

| Upside Breakeven | $108.00 ($105 strike + $3.00 premium) |

| Downside Breakeven | $92.00 ($95 strike - $3.00 premium) |

| Max Loss | $300 if XYZ closes anywhere between $95 and $105 |

Comparing the Outcomes

Notice something interesting here: in this specific scenario, both strategies share the exact same breakeven points of $92 and $108. The straddle costs $500 more to enter, but it begins gaining intrinsic value immediately if the stock moves away from $100.

| Scenario | XYZ Price at Expiration | Straddle P/L | Strangle P/L |

|---|---|---|---|

| Big Rally | $115 | +$700 | +$700 |

| Moderate Rally | $105 | -$300 | -$300 |

| No Movement | $100 | -$800 | -$300 |

| Breakeven (Up) | $108 | $0 | $0 |

| Breakeven (Down) | $92 | $0 | $0 |

If the stock rallies to $115, both trades make exactly $700 in profit. The straddle call has $15 of intrinsic value minus the $8 total position cost, netting $700. The strangle call has $10 of intrinsic value minus the $3 total position cost, also netting $700. But if the stock only moves to $105, both strategies lose $300. The straddle's call has $5 of intrinsic value but not enough to offset the $8 total cost, while the strangle's call expires with zero intrinsic value and the entire $300 premium is lost. The strangle risks less capital overall, but the stock must move beyond $105 or below $95 before your options gain any intrinsic value at all.

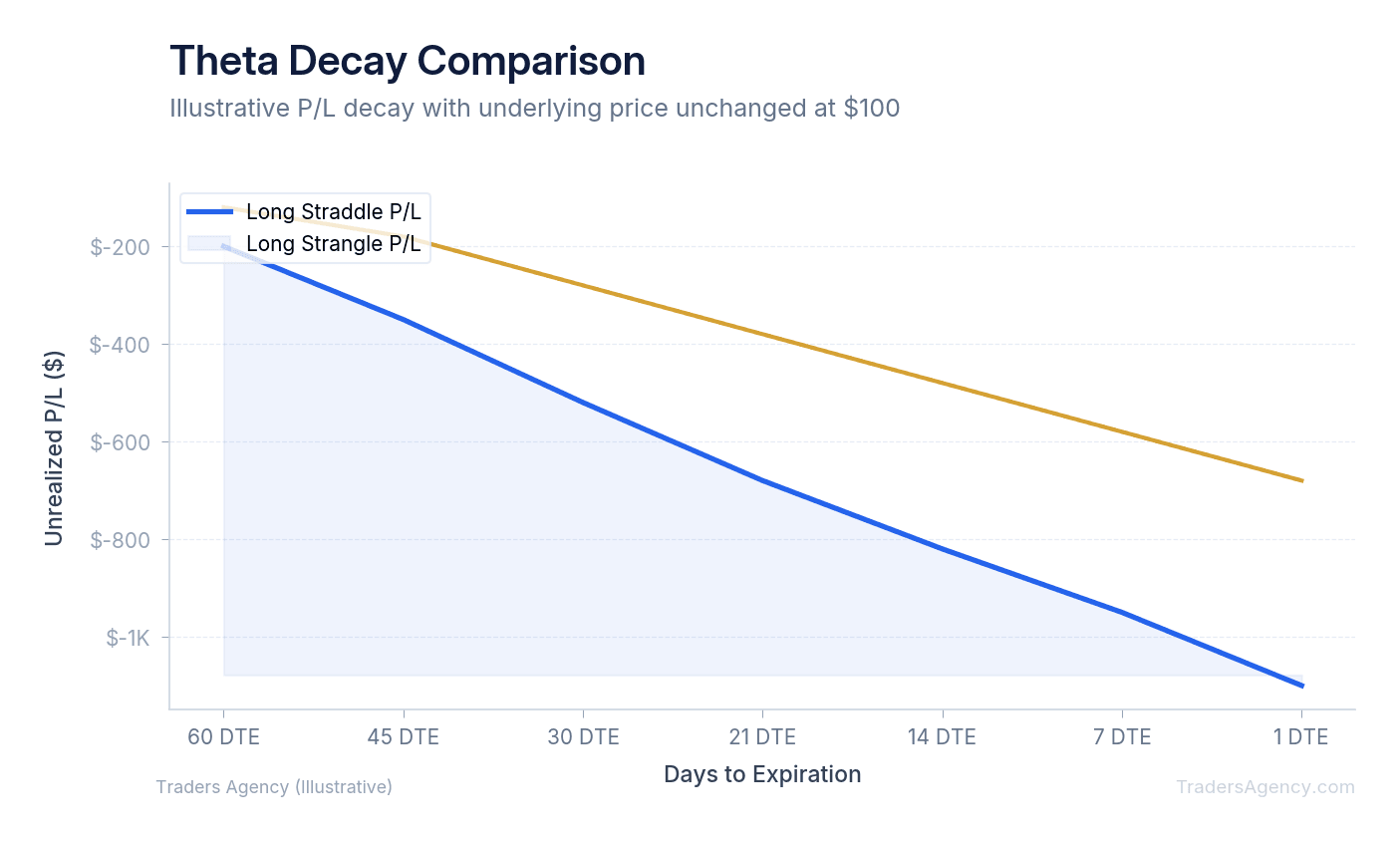

How Do Vega and Theta Affect Straddles and Strangles?

Both strategies are highly sensitive to implied volatility (vega) and time decay (theta). Because you're buying two options, you suffer double the time decay. You also benefit doubly if implied volatility expands, which is why we often enter these positions before a major known event occurs. Understanding the Greeks is essential for anyone trading volatility strategies.

Theta (Time Decay)

Time is your biggest enemy when holding long options. Every day that passes without a price movement chips away at the value of your contracts. ATM options in a straddle experience the highest absolute time decay. OTM options in a strangle decay slightly slower at first, but their value collapses rapidly in the final days before expiration if the stock remains stagnant.

Vega (Implied Volatility)

Both strategies need vega to increase or stay elevated. If you buy a straddle or strangle when implied volatility is already at its peak, you'll suffer a massive drop in premium value after the event passes. Even if the stock moves in your favor, a sudden drop in vega can wipe out your profits. We teach our members to enter these trades before the market fully prices in the upcoming volatility.

Watch Out: Buying options the day before earnings usually means paying the absolute highest premium possible. When the news breaks, implied volatility drops instantly. This is called a volatility crush, and it can destroy the value of your options even if the stock moves in your favor.

Managing Risk When Trading Volatility

Trading a straddle vs strangle requires strict risk management. Because you're buying premium, the mathematical probability of losing money is higher than when you sell premium. Here's our approach to keeping risk under control:

- Size Your Position Correctly: We prefer to allocate no more than 1% to 2% of total account equity to a single volatility play. If the trade goes to zero, your account survives easily.

- Set Profit Targets Early: If you get a quick 30% or 50% gain on the total position due to a sudden price spike, take the money. Waiting for maximum profit at expiration is a dangerous game.

- Enter Before the Crowd: The best time to enter is when implied volatility is still relatively low, typically 5 to 10 days before the expected event. This gives you a better entry price and room for vega expansion.

- Use Adequate Time to Expiration: We recommend buying at least 30 to 45 days of time. This gives the stock more opportunity to trend and reduces the daily impact of theta decay.

What Are the Most Common Mistakes Traders Make with Straddles and Strangles?

The most common mistake traders make is holding these positions too close to expiration. If the anticipated price move happens early, take your profits. Waiting for expiration exposes you to accelerating time decay and the risk that the stock might reverse back to its original price.

Here's what we teach our members to avoid when trading a straddle vs strangle:

- Ignoring the Volatility Crush: As we mentioned above, buying right before the event means paying peak premium. The post-event IV collapse can erase your gains entirely.

- Choosing the Wrong Expiration: Buying options that expire in three days leaves you no room for error. Give yourself 30 to 45 days minimum.

- Forgetting to Manage the Losing Leg: Sometimes traders ignore the losing option until expiration. If the stock reverses, that seemingly worthless option could regain value you'd miss by not monitoring it. Always manage both legs of the trade and close them deliberately.

- Overallocating Capital: These are speculative trades. Risking too much on a single straddle or strangle can devastate your account if the expected move doesn't materialize.

Remember This: Both the straddle and the strangle are powerful tools for capturing massive market moves. Your choice depends entirely on your risk tolerance, your available capital, and how far you believe the stock will run. The straddle costs more but profits sooner. The strangle costs less but needs a bigger move.

Our education team publishes new strategy guides and market analysis every week. If you found this straddle vs strangle breakdown helpful, there's a lot more where this came from.

Want expert trading insights delivered daily?

Join thousands of traders who rely on Traders Agency for market analysis and trade ideas.

Join Traders AgencyKey Takeaways

- A long straddle buys both a call and put at the same strike price and expiration, making it profitable when the stock moves sharply in either direction beyond the total premium paid.

- A strangle uses out-of-the-money options on both sides, which lowers the upfront cost but requires a larger underlying move to reach profitability compared to a straddle.

- ATM options carry the most extrinsic value, so straddle buyers face faster time decay and need a significant price move just to break even on premium paid.

- The straddle costs more and profits sooner on a moderate move; the strangle costs less but needs a bigger move to pay off.

- Both strategies are speculative and capital-intensive. Sizing too large on a single trade can cause serious account damage if the expected volatility never materializes.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources