Hey, Ross here:

I just took a position in a new stock, and I believe it has a chance to go 10x higher from today's price. This ServiceNow stock analysis breaks down exactly why I think this is one of the cleanest ten-bagger setups in the entire S&P 500 right now. The man running the most important technology company on Earth just pointed directly at this ticker.

Nvidia CEO Jensen Huang recently went on CNBC and told every CEO in America that the service industry is 100 times larger than the software industry. He specifically pointed at one ticker: ServiceNow. The AI rotation is just beginning. The obvious names have already run, and the real money will be made in the names institutions are still piling into quietly.

The Fortune 500's Operating System

Bottom Line: ServiceNow is not an AI speculation play. It is the workflow infrastructure already embedded inside the largest companies on Earth, now positioned as the default operating layer for agentic AI. With 22% growth, institutional accumulation, and a direct endorsement from Jensen Huang, the argument is that the market is still underpricing how central NOW becomes as enterprises automate at scale.

Most people have never heard of ServiceNow. That's partly by design. It is the plumbing that quietly makes a 200,000-person company actually function.

Every Fortune 500 you can think of runs ServiceNow underneath. Walmart, BFA, Lockheed, Coca-Cola. The system routes every IT ticket, every HR onboarding, every customer service case, finance approvals, and security alerts.

Why Did Jensen Huang Single Out ServiceNow?

Jensen Huang stated that we are seeing one of the greatest transformations for the software industry ever. For the first time, service is software, and software is service.

When Jensen speaks, you listen. His past public stock call-outs have absolutely cooked. People who listened to him last year made a fortune.

Jensen's 2025 Track Record

- NBIS: Called at $22 a share

- Intel: Called at $23 a share

- SanDisk: Called at $275 a share

- Coreweave: Called at $40 a share

- Taiwan Semi: Called at $240 a share

Now he is pointing directly at ServiceNow. The entire service economy has just been digitized by agents running on this exact platform.

What Agentic AI Advantage Is Wall Street Overlooking?

Wall Street has been dumping software stocks across the board because they think AI will replace software. That story is vastly oversimplified.

Nobody is ripping out ServiceNow to start over with a language model. ServiceNow already has the workflows, the data, the security model, the integrations, and the compliance. All the boring stuff nobody wants to rebuild. The AI gets bolted onto it. You stack AI agents on top, and those agents inherit everything underneath.

This is the trillion dollar idea. ServiceNow charges you for the agents. Over the last 12 months, they have quietly assembled the most important AI stack in enterprise software.

The AI War Chest

Moveworks: Acquired for $2.85 billion to secure the best front-end AI assistant in the enterprise.

Armis: Acquired for $7.5 billion. The largest acquisition in company history, bought specifically for cybersecurity and AI control, the ability to govern every single AI agent running inside a Fortune 500 company.

Major Partnerships: Layered on deals with Nvidia, OpenAI, Microsoft, AWS, and Anthropic.

They also launched the AI control tower. This command layer watches every AI agent operating inside the enterprise, no matter who built it. Every company in America is terrified an AI agent will leak data or break a regulation. Whoever solves that problem becomes the operating system for AI. That is what Microsoft did in the 80s and 90s. That is what ServiceNow is building now.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubWhy Did Bank of America Issue a Buy Signal on ServiceNow?

Bank of America just reinstated ServiceNow at a buy rating.

The company just priced $4 billion in debt at very tight spreads. The market read that debt pricing as a giant green light. They are funding the next leg of the AI buildout, the Armis integration, and more acquisitions.

McDermott's Trillion-Dollar Bet

When executives have their incentives aligned with investors, that is when the magic happens. ServiceNow CEO Bill McDermott has publicly committed to a $1 trillion market cap by 2030.

He tied his entire compensation package to hitting that exact number. A staggering 97% of his pay is tied directly to the stock's performance.

McDermott is the guy who took SAP to a $4 trillion valuation in his last job. He is not making these kinds of claims unless he has the math to back it up.

A ServiceNow Stock Analysis: The Numbers That Prove It

ServiceNow currently sits at a market cap of right around $100 billion. Reaching a trillion is 10 times that. A proper ServiceNow stock analysis requires looking at the raw financial data from Q1 2026.

The numbers prove this is not hype. It is already working inside the enterprise.

Q1 2026 Financial Breakdown

- Subscription Revenue: $3.7 billion, up 22% year-over-year

- Operating Margin: 32%

- Free Cash Flow Margin: 44%. For every dollar that walks in the door, 44 cents drops straight to free cash flow.

- Now Assist Growth: Customers spending over $1 million a year on their AI agent product grew 130% year-over-year

- Remaining Performance Obligations: $27.7 billion, up 25% year-over-year. Future revenue already signed and booked.

Show me another hundred billion dollar company growing 22% a year with a 42% cash flow margin. There are maybe three of them in the entire stock market, and ServiceNow is one.

The Path to a Trillion

ServiceNow guided to about $15.7 billion in subscription revenue this year. They are growing at 22%. If they hold even close to that growth rate, call it 17% or 18% compounded, they will be north of $30 billion in revenue by 2030.

Apply the same revenue multiple they trade at today, and you get a trillion dollar market cap. That is not some pie-in-the-sky number. That is just 20% compounded growth and the multiple holding where it is today. The multiple could actually expand because as AI monetization kicks in, ServiceNow's margins go up, not down.

Software companies do not usually scale at 40%+ free cash flow margins. ServiceNow does. Add AI agents and it gets better, not worse.

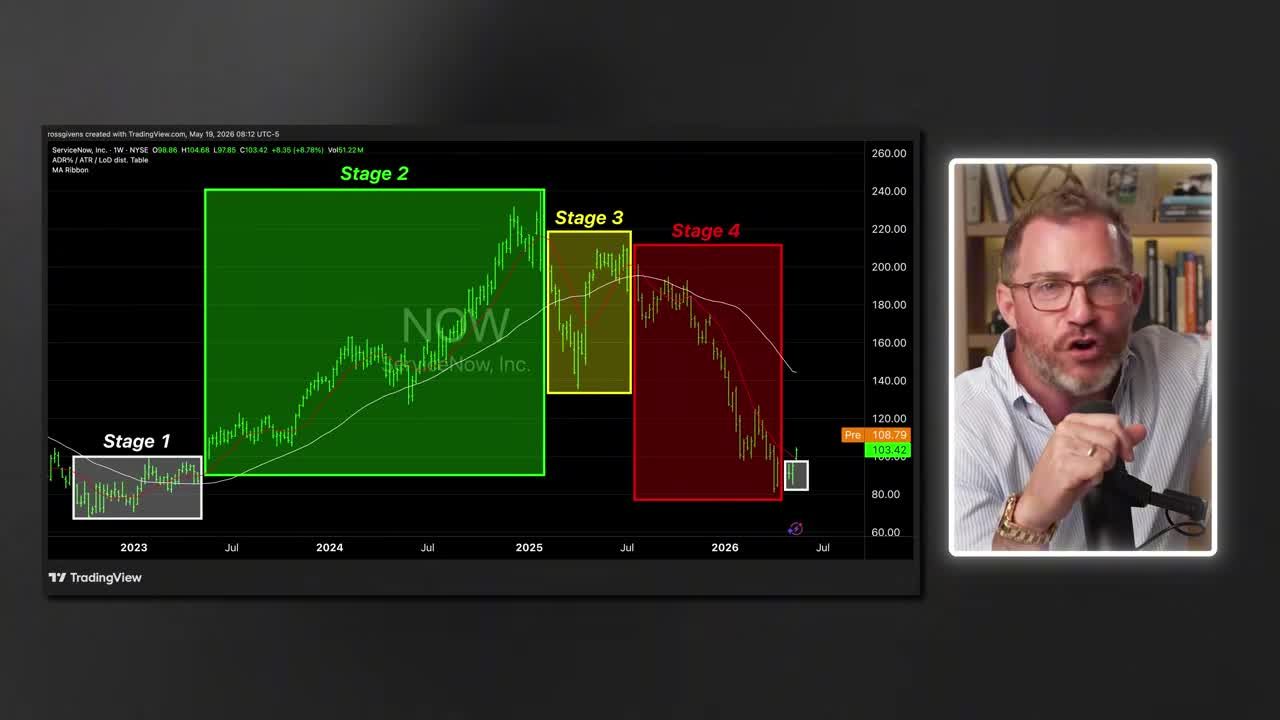

The Technical Setup

My ServiceNow stock analysis points to a massive technical setup. The stock has been building a base in the 90s after a 65% stage 4 decline.

This is my favorite place to buy a stock. Coming out of a stage one consolidation, off the lows, making a strong turnaround on heavy volume. These are the setups where you can make several hundred percent on the way up.

This has been a very short stage one consolidation. Typically, these take months or years to form. ServiceNow simply got caught in a group move. When big institutions get out of a sector, they dump every software stock and every software ETF. ServiceNow was collateral damage, and investors are waking up to that fact quickly.

I bought 200 shares this week at about $100 a piece. I am planning to add on pullbacks or new base formations. This is a position worth building for the next two to three years.

The Operating System of Corporate AI

The winning strategy for the rest of 2026 is not chasing the obvious AI names or the big hyperscalers. The real opportunity lies in the actual operating system of corporate AI.

ServiceNow is growing 22% a year. The CEO of Nvidia is personally telling everyone who will listen that this is where the real money is going to be made. The fundamentals are solid, the chart looks ready, and the AI monetization is already showing up in the numbers.

This is a setup I will buy every day of the week. Do with this information what you will, but I think it is a bet worth making.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- Nvidia CEO Jensen Huang publicly named ServiceNow on CNBC as the prime beneficiary of his thesis that the service industry is 100 times larger than the software industry.

- ServiceNow processes over 80 billion enterprise workflows annually, covering IT, HR, finance, security, and customer service across the Fortune 500, including Walmart, Lockheed, and Coca-Cola.

- NOW is growing revenue at 22% annually, and AI monetization is already appearing in reported financials, not just in forward projections.

- Bank of America has issued a buy signal on the stock, adding institutional conviction to a name that is still being accumulated quietly by large funds.

- The core bull case is that ServiceNow is the existing infrastructure layer where corporate AI agents will run, giving it a structural moat that pure-play AI startups cannot replicate.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources