If you want to find massive opportunities in the market, you have to look where the math simply does not match the stock price. This Nu Holdings stock analysis reveals a $14 financial technology company completely dominating its sector. Profitable. High-growth. Trading at a massive discount.

Warren Buffett saw this coming years ago. Retail investors are quietly loading up. And the window to get in early is closing.

Why Did Warren Buffett Invest in Nu Holdings?

Bottom Line: Nu Holdings presents a rare combination of Buffett-backed credibility, high-margin profitability, and early-stage market penetration in a region where traditional banking has historically underserved consumers. At $14.68, the stock trades below the analyst consensus target with 2025 earnings growth accelerating faster than revenue, the kind of leverage expansion that tends to reprice a stock. The core risk to watch is whether Latin American macro conditions or currency volatility compress those margins before the market re-rates the valuation.

Warren Buffett is famous for avoiding technology bets. He held cash for years while the dotcom bubble inflated and popped. He passed on Google. He passed on Amazon. He passed on Facebook. He has publicly admitted he missed some of the biggest wealth-creating opportunities of the last 30 years because technology simply was not in his circle of competence.

So when Buffett puts Berkshire Hathaway's money into a fintech company, you stop and pay attention.

Berkshire Hathaway first invested in Nu Holdings, ticker symbol NU, back in 2021. They participated in a $500 million pre-IPO funding round. When the company went public in December 2021, Berkshire held a stake that was worth over a billion dollars at one point.

Buffett does not invest in fintech on a whim. His thesis was clear: Nu Bank is doing to Latin American banking what American Express did to consumer financial services decades ago. They were creating a sticky, trusted, high-margin platform with enormous network effects.

Latin America's Broken Banking System

To understand the magnitude of this opportunity, you have to understand the environment. Latin America is one of the most underbanked regions in the world.

Before Nu Bank launched in 2013, the banking system in Brazil was a nightmare for the average consumer. Getting a bank account required visiting a physical branch. You paid enormous fees. You navigated a notoriously bureaucratic process. Traditional Brazilian banks charged obscene fees for basic services. Credit was nearly impossible to access for ordinary people.

Nu Bank came in with a mobile-first, fee-free model. No physical branches. No monthly fees. Full banking services through a simple app on your phone. The result has been explosive adoption.

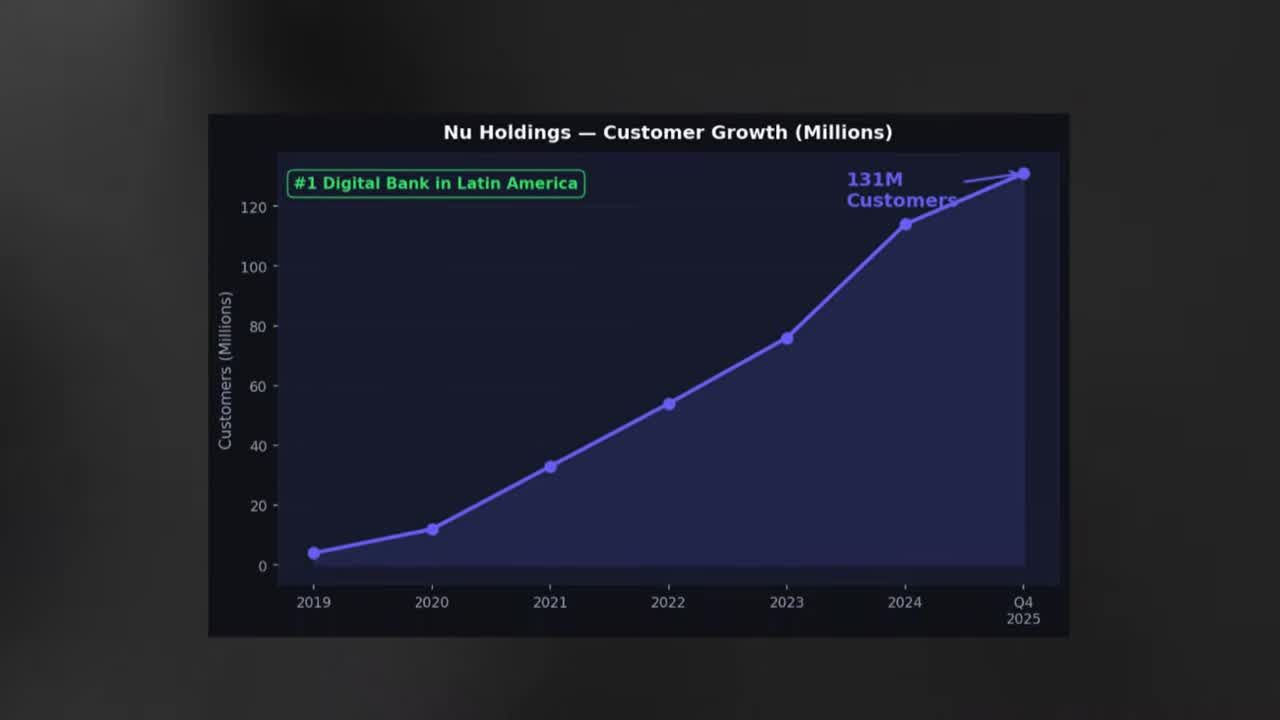

Nu Holdings Stock Analysis: 131 Million Customers and Counting

The sheer size of this user base is almost hard to believe.

As of Q4 2025, Nu Bank has 131 million customers. That is not a typo. 131 million customers across Brazil, Mexico, and Colombia.

For context, Bank of America, one of the largest banks in the United States, has around 68 million customers. Nu Bank has nearly twice that. And they are still growing at 15% per year.

The data advantage they hold on those 131 million users makes their credit underwriting better than any traditional bank could ever hope to achieve.

What Do Nu Holdings' Earnings Actually Show?

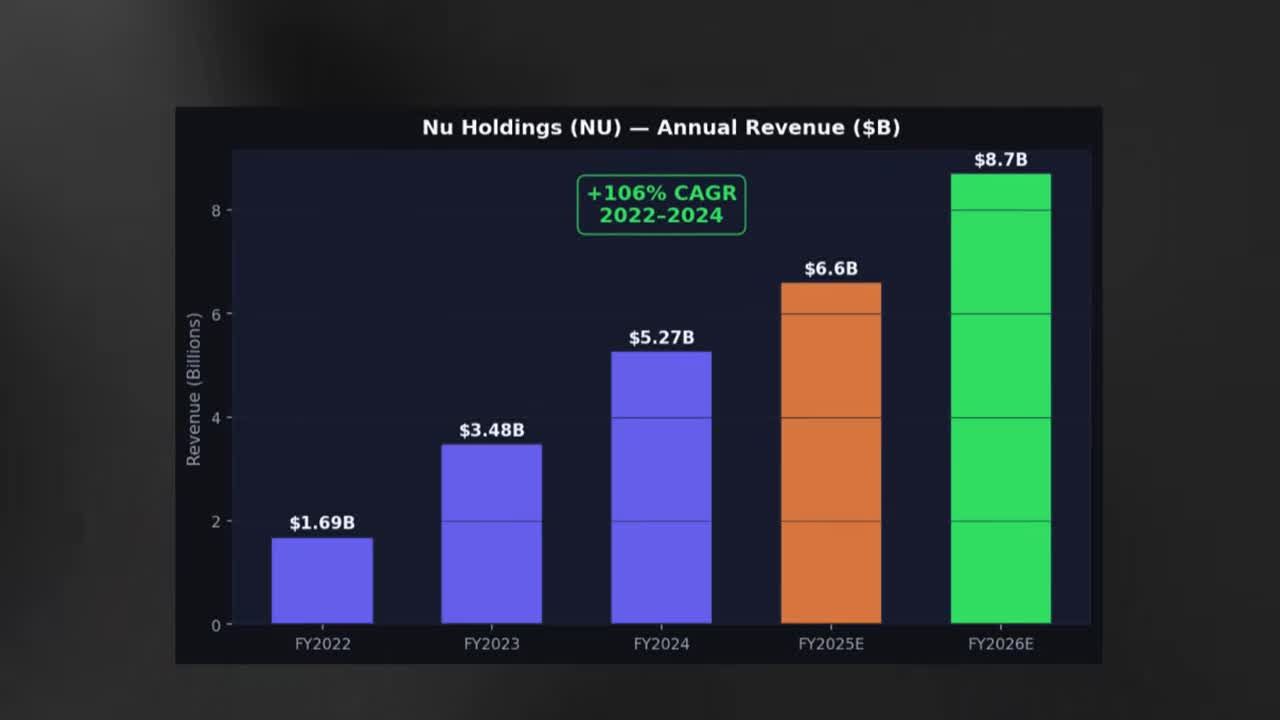

A massive user base only matters if a company can monetize it. The recent earnings data proves they are doing exactly that. This is not a startup burning through cash hoping to find a business model. This is a profitable, high-growth bank at scale.

- Revenue Growth: Revenue grew 26% last year to $6.6 billion.

- Net Income: Profit was $2.87 billion, up 46%.

- Profit Margins: The company operates with 47% profit margins.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubIs Nu Holdings Expanding Beyond Brazil?

Most investors look at the 131 million existing customers and think the growth story is over. It is not even close to over.

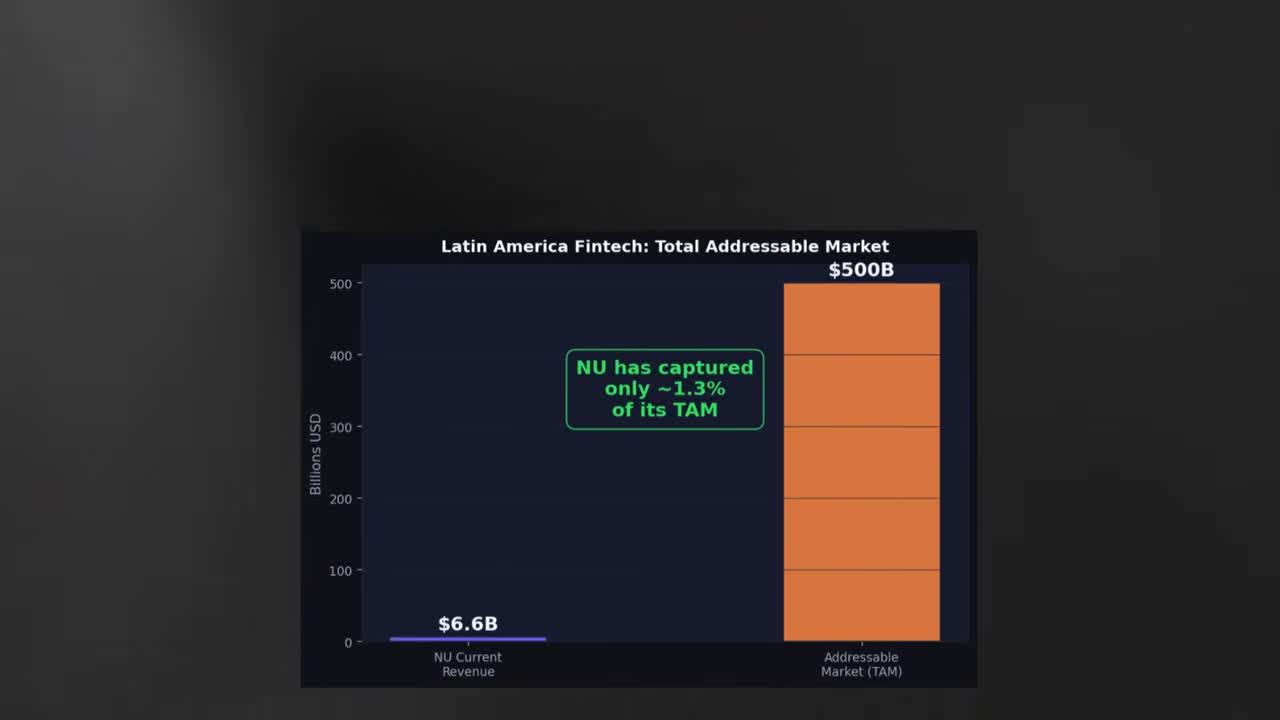

Latin America has a combined population of roughly 650 million people. Brazil alone is 215 million. Mexico, 130 million. Colombia, 52 million.

The total addressable market for digital banking in Latin America is estimated at over $500 billion in annual revenue once fully penetrated. Nu Bank has $6.6 billion in revenue. That means they are capturing roughly 1.3% of the total opportunity.

The US Play: Nu Stadium

Nu Bank is not just resting on its Latin American dominance. They recently announced plans to enter the United States market, and they are taking an aggressive approach to brand building.

They just secured the naming rights to Miami's new stadium, calling it Nu Stadium, one of MLS's largest sponsorship deals ever. That brand building is part of their US expansion strategy.

Growing Revenue Per User

The company also expanded its credit product lineup: personal loans, FGTS credit in Brazil, business accounts. Average revenue per user is growing. They are not just relying on adding new customers. They are extracting more revenue from every existing user on the platform.

Is NU Undervalued at $14?

NU stock closed at $14 and change, up around 5% on the day. The 52-week range has been wide. The stock has been volatile as investors debate growth versus profitability.

When you look at the underlying math, the current price makes no sense.

NU trades at about 16 times forward earnings. That is 16 times what analysts think they will earn in 2026. For a company growing revenue at 26% per year, with 47% profit margins, and 130 million and counting customers, 16 times forward earnings is cheap.

Compare that to PayPal, which has been shrinking yet trades at similar multiples. Or look at Block, ticker symbol SQ, with far less impressive fundamentals. NU's growth rate is superior to virtually every fintech in the world right now. Trading at just 16 times forward earnings is a massive discount to fair value.

Wall Street Is Waking Up

Nine analysts cover NU stock with a consensus rating of buy.

UBS just upgraded the stock to strong buy on March 19. JP Morgan maintains a buy at $18. Susquehanna has a buy with a $22 target.

The Susquehanna note is particularly interesting. They project Nu's revenues could reach $20 billion by 2026 as their credit business scales up. From $6.6 billion to $20 billion in one year. That is an ambitious estimate, but it reflects how rapidly that credit book is compounding.

Retail Investors Are Loading Up

A lot of people do not realize that retail investors are starting to pay attention to NU stock in a big way. The stock shows up repeatedly in investing and stock threads on Reddit. Retail traders are actively hunting for undervalued fintech opportunities, and NU keeps hitting their radar.

The pitch is powerful. A Buffett-backed company. 26% revenue growth. A stock priced around $14. Retail investors looking for the next big thing are quietly building positions.

As Nu Bank continues to report strong earnings quarters, the narrative will shift. As the US expansion builds brand recognition in North America, more eyes will find the stock. As analysts continue to raise their targets, institutional money will rotate in. That creates a feedback loop, and that feedback loop is what drives a stock higher.

The retail investors loading up right now are early, not late. They are seeing what Warren Buffett saw three years ago.

The Bottom Line on This Nu Holdings Stock Analysis

Nu Bank has 131 million customers, still growing at 15% per year. Revenue hits $6.5 billion in 2025, representing 26% growth. Net income at $2.87 billion, up 46%, driven by those 47% profit margins.

Warren Buffett's Berkshire Hathaway backed this company before it went public and has held through the volatility.

The stock sits at $14.68. The analyst average target is $17.84. The high target is $22. And this is just for 2026.

Latin America's banking revolution has barely started. Nu Bank has captured 1.3% of the total addressable market. In 20 years in financial markets, I have seen what happens when a Buffett-backed company with monopoly-like growth metrics trades at a discount to fair value. Patient investors get rewarded. The stock may have significant room to run from here.

NU is one of those positions.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Key Takeaways

- Nu Holdings trades at $14.68 against an analyst average price target of $17.84 and a high target of $22, implying 20–50% upside before accounting for further growth.

- 2025 projections show $6.5 billion in revenue (26% growth) and $2.87 billion in net income (46% growth), with profit margins near 47%, unusually high for a growth-stage fintech.

- Berkshire Hathaway entered at the pre-IPO stage in 2021 via a $500 million funding round, a rare move for Buffett given his long-stated aversion to technology and fintech bets.

- Nu Holdings has 131 million customers but has captured only 1.3% of its total addressable market in Latin America, leaving a long runway if customer acquisition continues at current pace.

- Revenue growth of 26% combined with net income growth of 46% signals operating leverage, costs are scaling slower than revenue, which is the pattern traders watch for in platform businesses.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources